Part 2 appears to be taking off now after the summer cool down. But part 2 is not going to play out like part 1. It will be more difficult for more people one way (increasing inflation problem) or another (inflation failure and bust, which is what has happened historically in the post-2000 era of Inflation onDemand).

It is time to know the macro and to know yourself. It is time not to go on auto pilot, or at least as we enter 2022 I would recommend you not swallow dogma and practice automatic thinking (the herd of course will do exactly that).

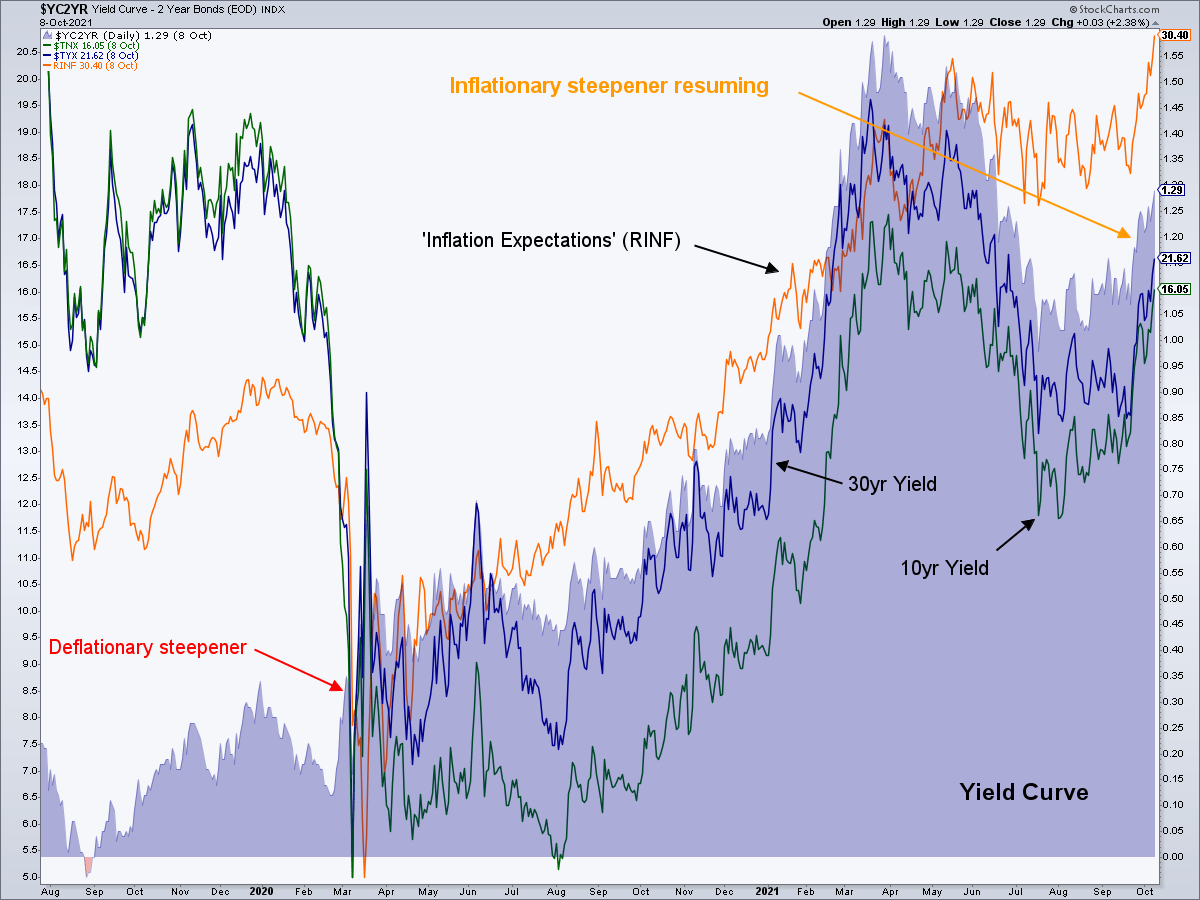

Anyway, after the “summer cool down” (my own theme that I have to admit mentally whipsawed me a little) it appears that the next step – as originally projected – is engaging. That step is for a resumption of the the inflation. At this moment it feels pretty good for asset speculators, at least. That will not last. I am not going to blab the details publicly because this is where NFTRH makes its bones by staying apart from herd-think using indicators rather than bias. So I’ll just note two things…

Thing 1: current macro signaling is inflationary, with the yield curve steepening and inflation expectations rising along with Treasury yields.

Thing 2: the inflationary situation will either morph to a more intense and painful version (Stag) or change to something very painful in the other direction when the indicators say the risk of change is likely.

For now, party on Garth.

For “best of breed” top down analysis of all major markets, subscribe to NFTRH Premium, which includes an in-depth weekly market report, detailed market updates and NFTRH+ dynamic updates and chart/trade setup ideas. Subscribe by PayPal or credit card using a button on the right sidebar (if using a mobile device you may need to scroll down). Keep up to date with actionable public content at NFTRH.com by using the email form on the right sidebar. Follow via Twitter @NFTRHgt.