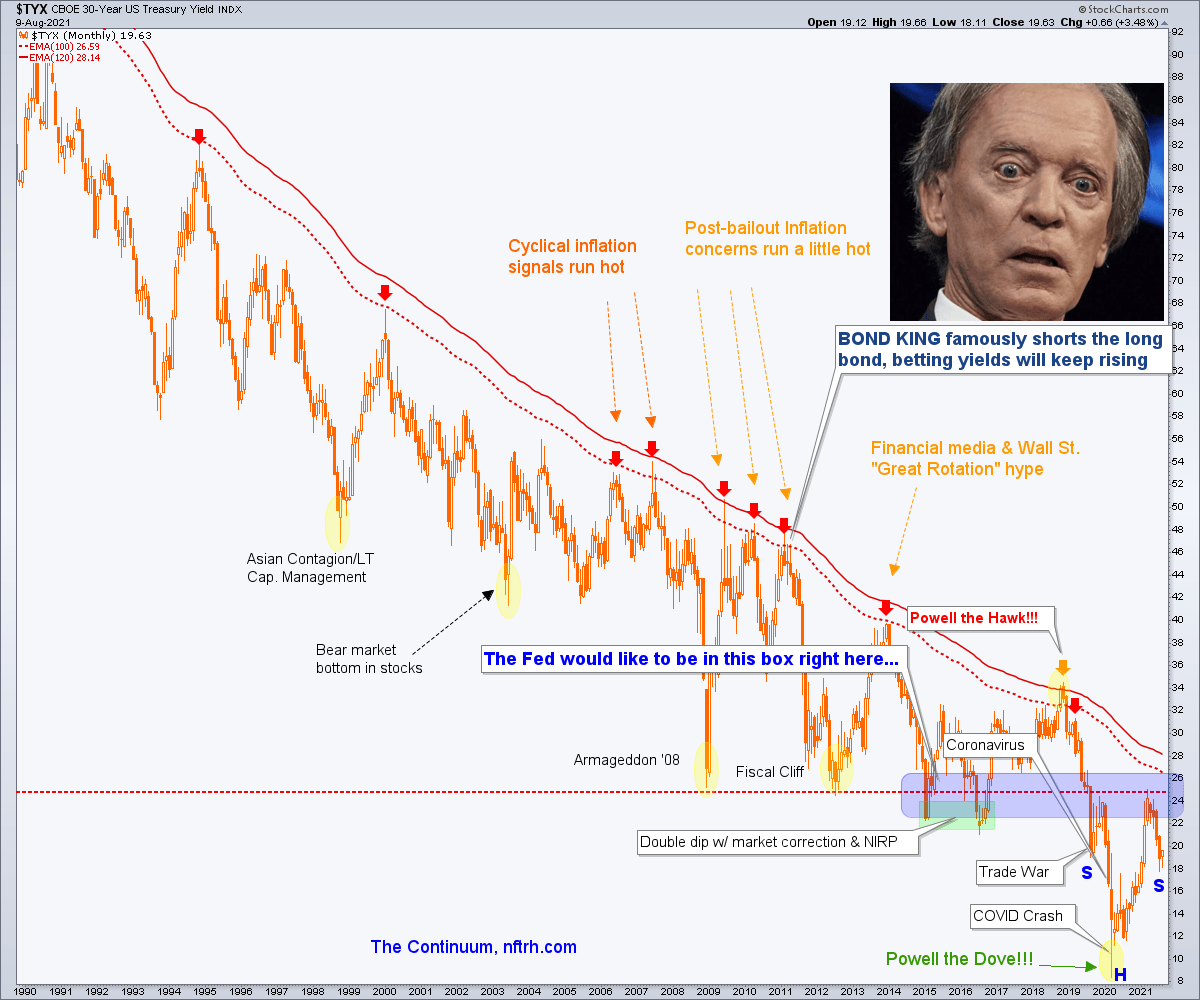

The 30yr Treasury yield has made its right side shoulder

Of course there is inflation.

We see it everywhere; the Fed’s printed (funny) munny and the government’s cost-pushing into the economy. Everybody knows that inflation is here and everybody has known since March when the last guy, still sitting on his couch playing lockdown era video games, figured it out.

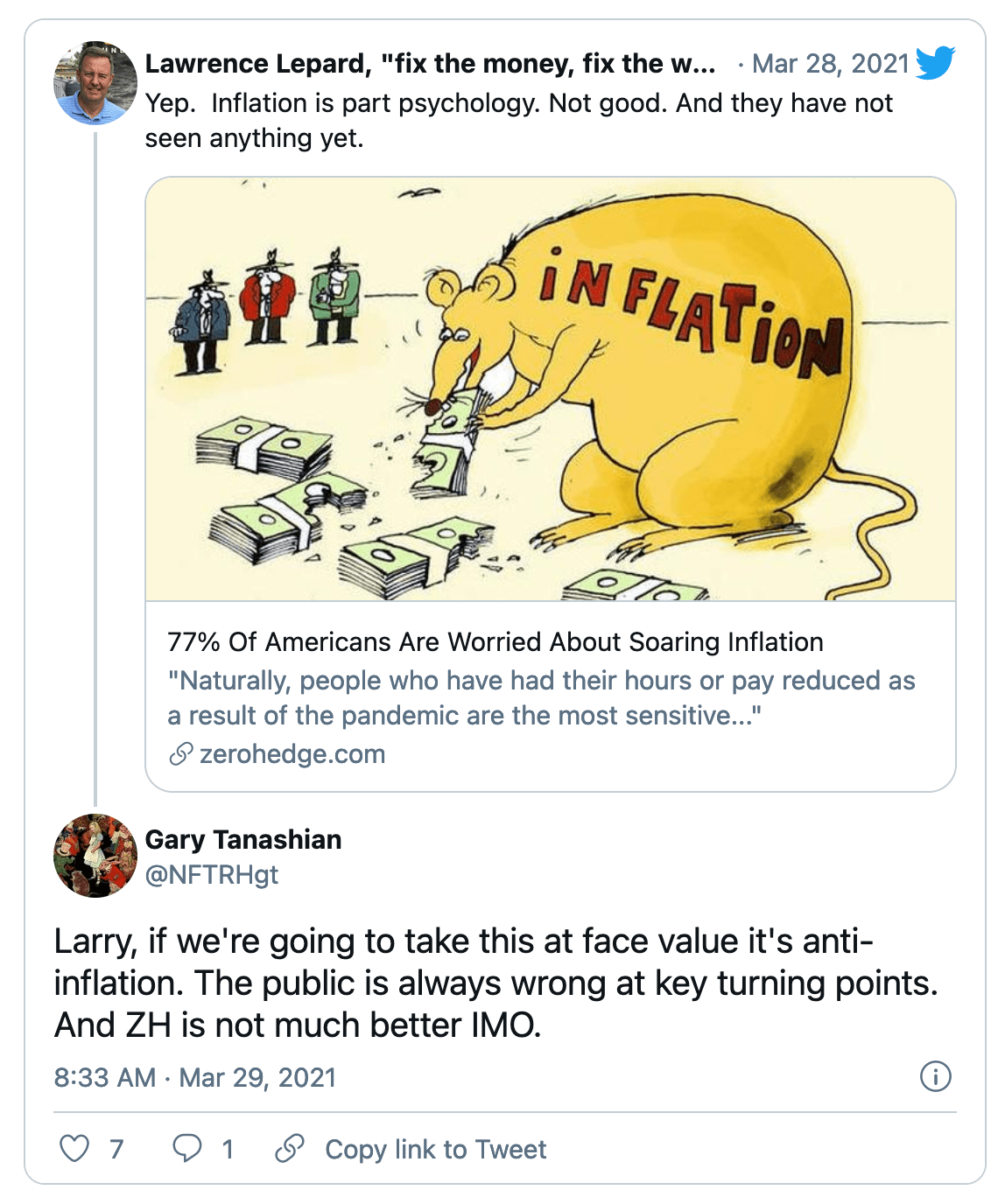

And then Zero Hedge called the top with an assist from Larry…

Then came our summer cool down thesis. And with the Gold/Silver ratio doing this, there is now some meat on the cool down’s bones.

Some people think market ratios are useless. I happen to think they are more important than nominal charts for sussing out the hints that are hidden below the surface. Do they always work to logical ends? Come on now, these are the markets. There’s a good deal of mayhem (and manipulation) woven in with any logical view. But it is beyond dispute that gold is less inflation sensitive, less cyclical than silver, and gold bottomed vs. silver in yup, March.

So with the still flaming inflation numbers within the economy it is up to the Continuum (monthly 30yr yield) now to put in that right side inverted shoulder and rise anew, as one (but probably not the main indicator) of forward inflation. Our plan was for a cool down as represented by the decline from the March high to put in another shoulder. Now the yield is postured to put in that shoulder.

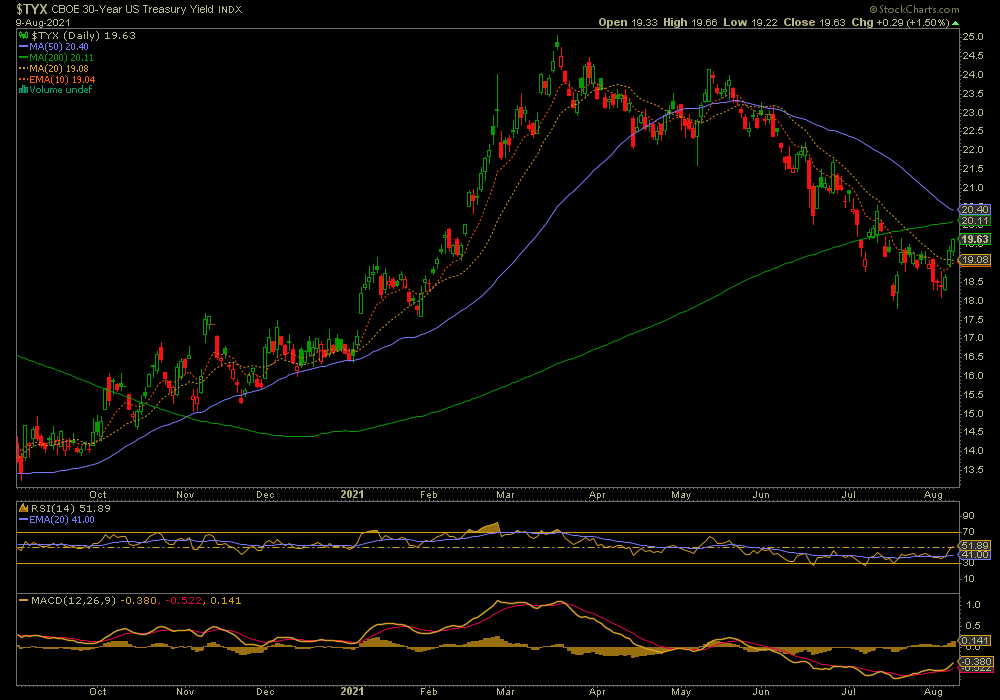

But a monthly chart is slower and more lumbering than a daily chart or our own brain functions, so let’s dial in a daily view. We find a short-term ‘W’ pattern and a bounce toward the converged SMA 50 and SMA 200. Take those out and the yield has a good shot at putting in the right side shoulder.

What comes after that? Well, you tell me what the Gold/Silver ratio and the US dollar are going to do and then I’ll tell you what’s in play. With the memory of daddy Deflationist Robert Prechter once projecting rising long-term yields under a deflationary backdrop I’ll stay open minded, although traditionally rising yields indicate a heating economy and in this case, a heating economy hopped up on inflation.

So the original view back in March was for a cool down prior to a whopping new inflationary phase, likely leading to economically impairing cost pressures as it morphs to Stagflation. So a valid question is what is the Fed more concerned about, an out of control inflation as created by its own hand or a deflationary liquidation the likes of which visits the macro periodically every several years?

My guess? Thing 2 is the Fed’s preference because it keeps them in business, at the ready to pretend to be saviors once again. Thing 1 would expose and could ultimately incinerate the Fed and its inflationary brinkmanship. Now, just because the Fed does not want rampant and runaway inflation it does not mean they can stop it. I see it as a battle going on behind the scenes while we casino patrons trade this mess as if it were all normal.

What do we lowly participants do? Well, this lowly participant is going to continue watching indicators, weighing probabilities because the answers will eventually come in. It’s not advisable to play hero or adhere to orthodoxy at a time like this. It’s advisable to listen to the market. It will burp up directional signals at some point likely sooner, not later.

For “best of breed” top down analysis of all major markets, subscribe to NFTRH Premium, which includes an in-depth weekly market report, detailed market updates and NFTRH+ dynamic updates and chart/trade setup ideas. Subscribe by PayPal or credit card using a button on the right sidebar (if using a mobile device you may need to scroll down). Keep up to date with actionable public content at NFTRH.com by using the email form on the right sidebar. Follow via Twitter @NFTRHgt.