I wanted to get this posted now but am not going to proof it for typos or confusing language (past dinner time). I’ll proof it in the morning, so if you’d like you can check it out again tomorrow. Edits added at the end.

In 2008 and 2011 inflation trades ended. The former rolled over and crashed and the latter shot up like a bottle rocket (led by silver) and blew out into a bear market in inflation (with a little nudge from Operation Twist).

I was going to simply do this update through the lens of the Gold/Silver ratio (GSR) and its similarity to 2008, but in conversing with Jordan of the Daily Gold he made a good point that the Gold/SPX ratio is similar to its 2011 state but not to its 2008 state (GSR is similar to 2008 but not very similar to 2011). But again, the common theme is the ending of inflation trades, led by the tanking precious metals (the asset class that led the 2001-2008 and 2009-2011 inflation episodes).

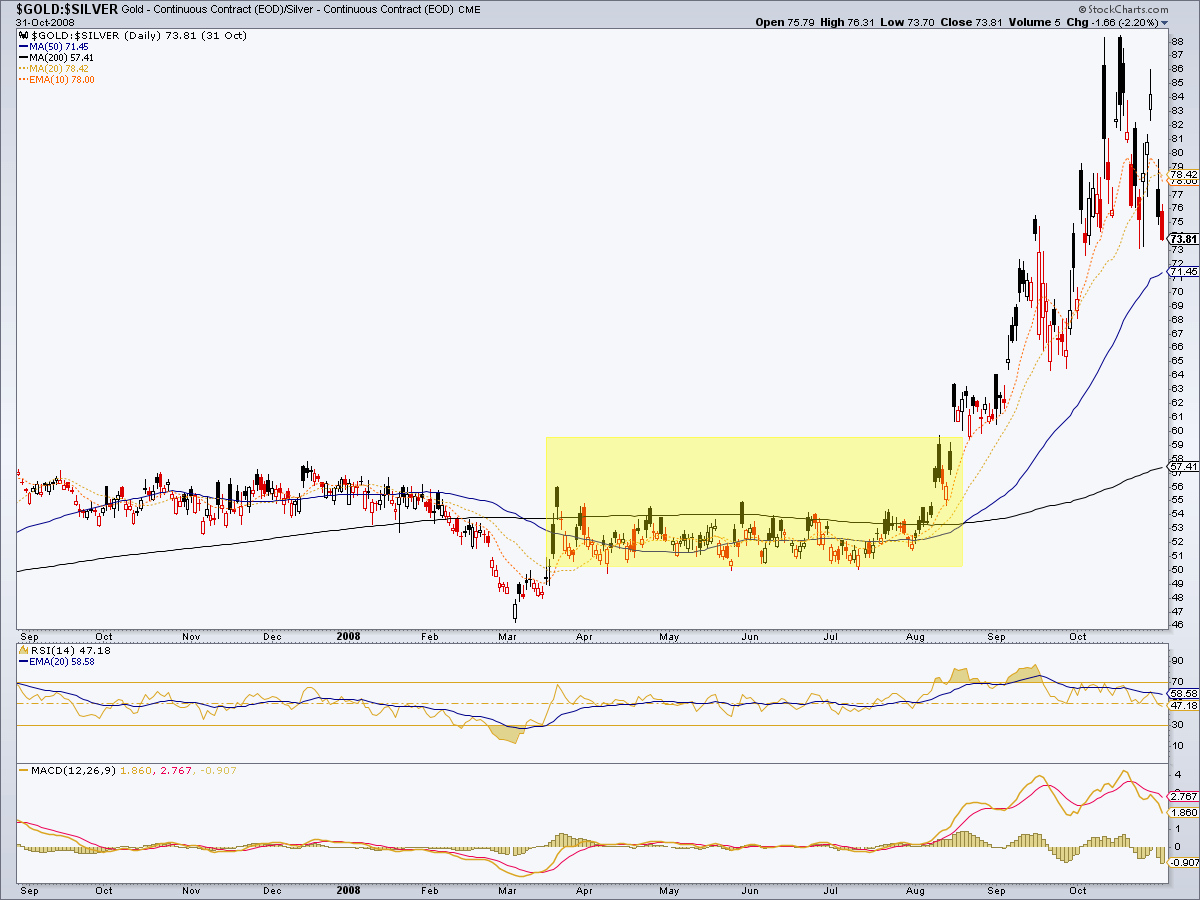

First let’s look at the GSR and its similarity to 2008. In that year the GSR based and turned up in August. This was a precursor – as noted at the time (although I did not begin publishing NFTRH until September 2008) – to what I called Armageddon ’08, a deflationary resolution to the 2003-2008 inflation trades that came compliments of Alan Greenspan’s Fed and its credit bubble.

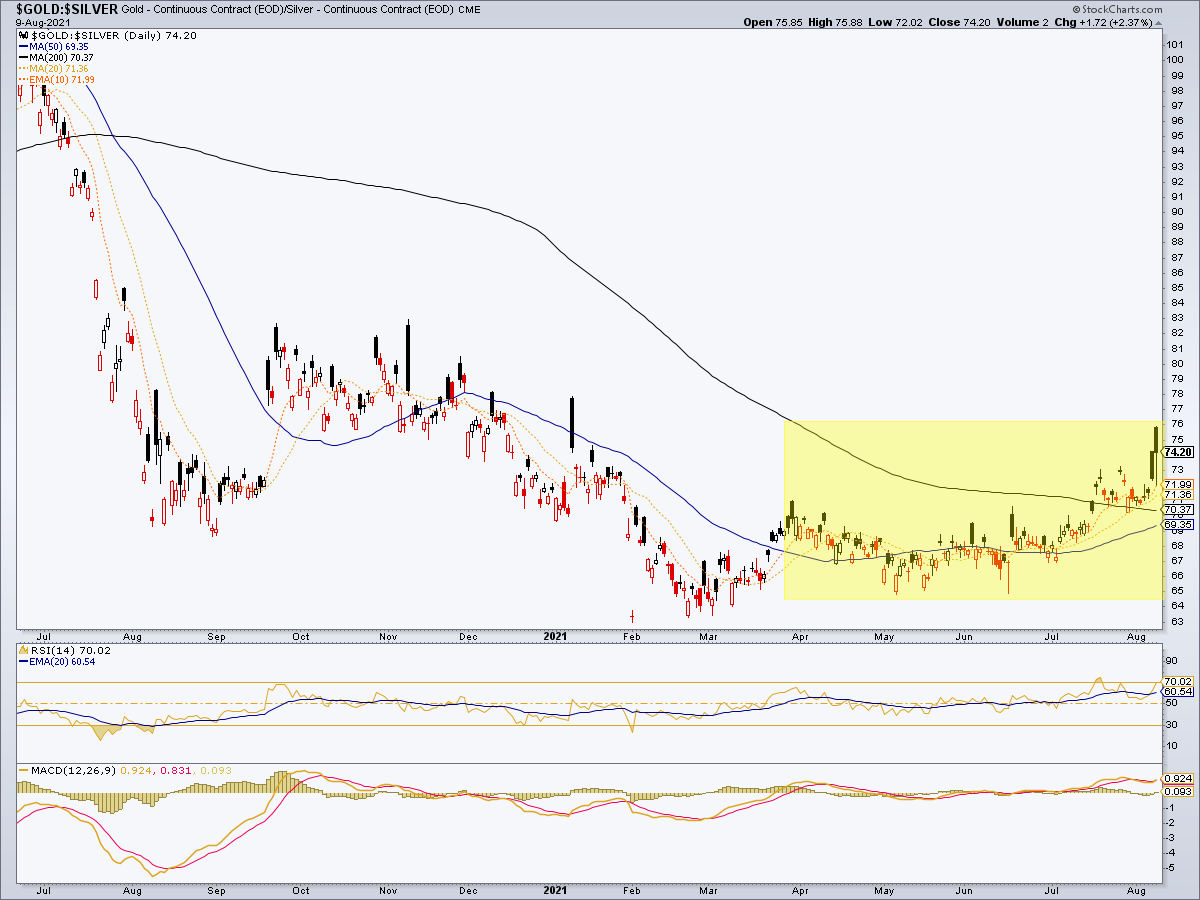

Today the GSR is as we’ve been noting for the last several weeks. It has based in similar fashion and taken out the daily moving averages. So here is a visual from today and yesteryear about why I am increasing the caution, especially as pertains to precious metals, commodities and the reflation stuff.

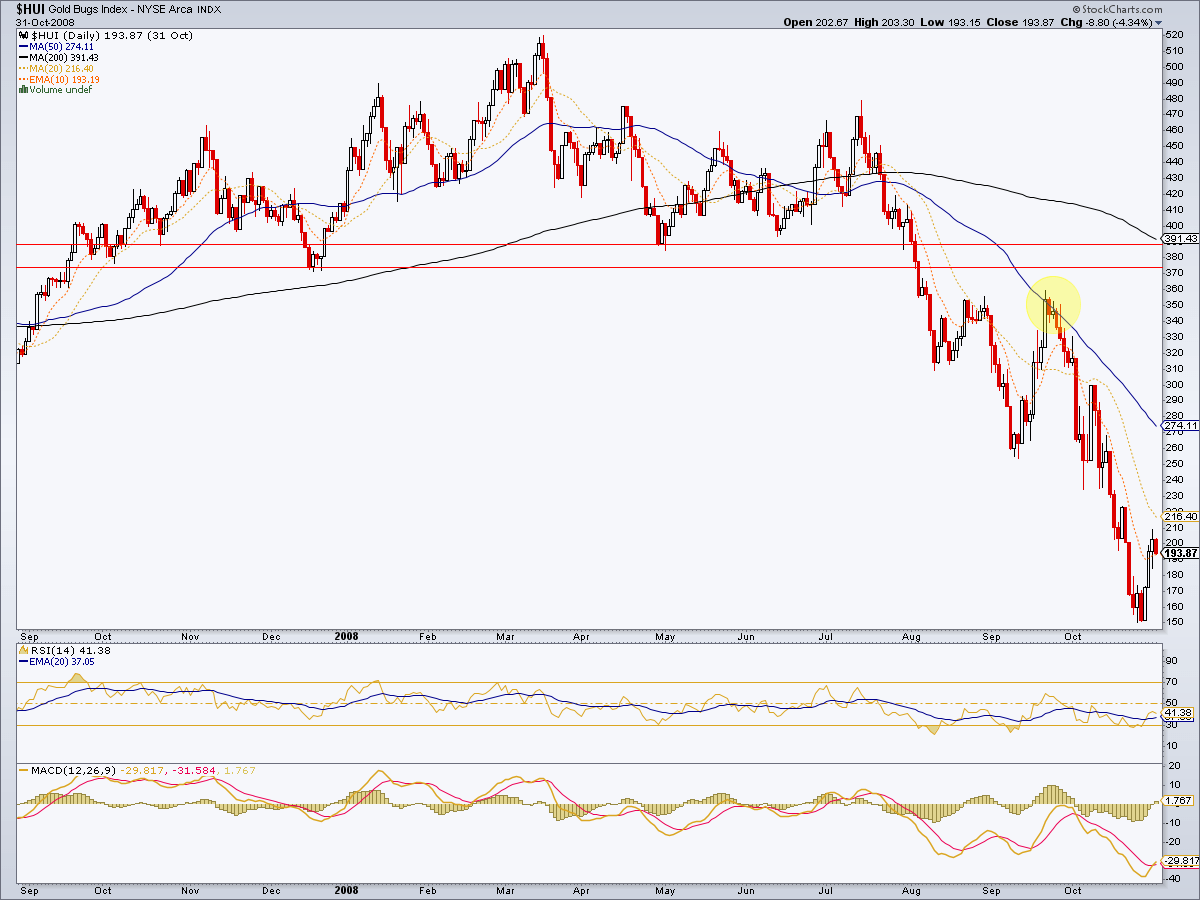

HUI 2008 broke down and did not quite make a test of resistance but did make a test of the SMA 50, which it failed in spectacular fashion.

HUI today just made its failed test of the SMA 50 last week. I might add that I did not distinguish myself on that test because I felt there could be a little more bounce left before failure. In hindsight I would like to have pounded a bearish table. The main theme is/was the same, however. HUI is and has been bearish and down trending since it failed the down-turning moving averages.

HUI 2008 above bottomed at 150 and HUI 2021 has downside targets of 230, 212 and per the measurement in this morning’s update, a theoretical 185 as well. But you probably know the drill when the soldier bugs start to panic and disobey the leader bugs. So a test of the 2020 low is also open if we get a genuine running of the gold bugs event.

In 2008 HUI had already flipped bearish well before it became readily apparent that the rest of the market was in trouble as well.

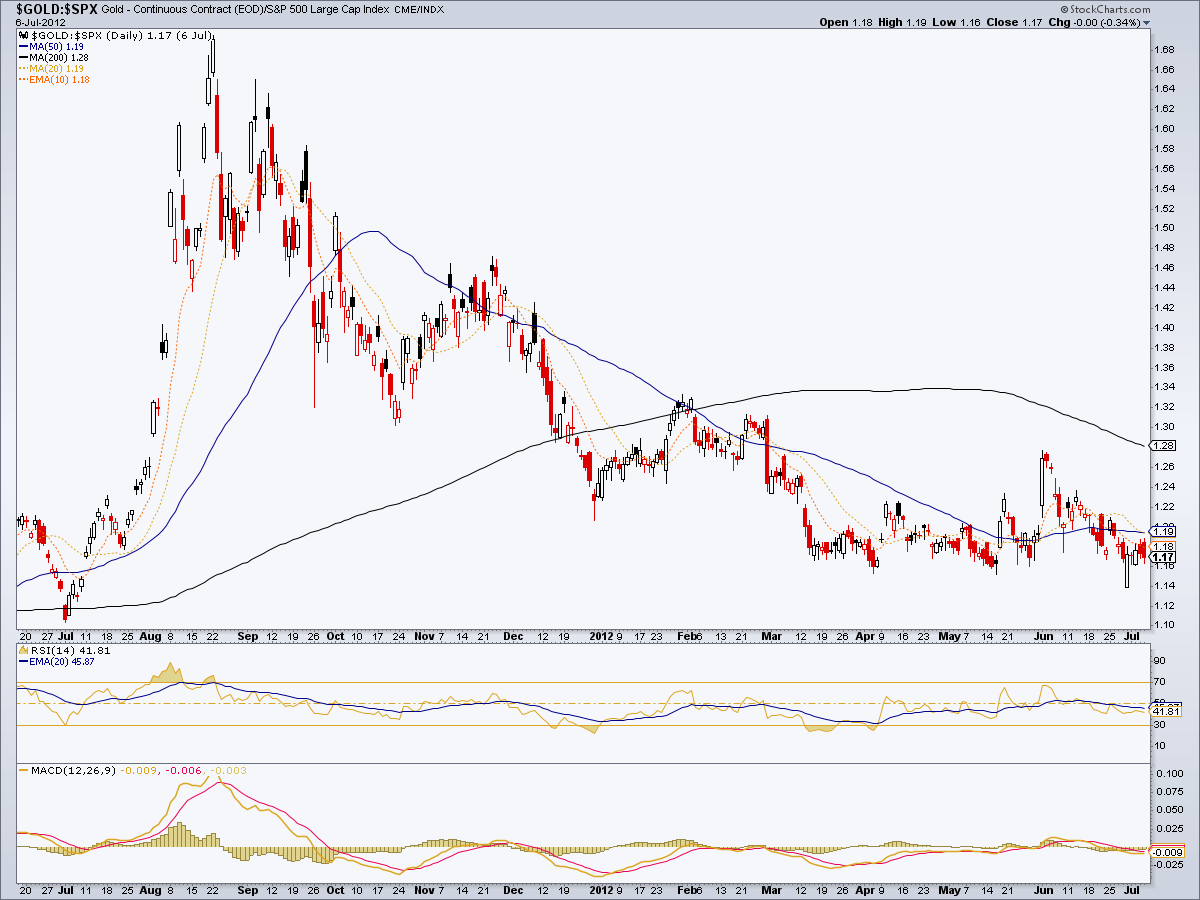

Shifting to the 2011 scenario, here is the Gold/SPX ratio in 2011. The inflation trades had already blown out with silver in the spring, but then came the Euro crisis knee-jerk into gold. That was 2011’s COVID disaster. Gold/SPX blew out in August that year and what you see below was the start of a significant bear market in the precious metals.

It’s important to note that what came next for stocks was not a bear market, but a rotation to a Goldilocks market in the US amid global disinflation but not deflationary disaster. That is why I continually bring up Goldilocks as an option today as well.

Here is Gold/SPX 2021 showing the COVID spike acting as the Euro crisis did back in 2011. While I called the need for gold to correct last summer I also called it a handle to a bullish cup. That is still in play, but it is time for open minds with respect to the potential for another bear market in gold.

The common themes between the two phases (2008 & 2011) were bearish precious metals and commodities as inflation blew out and market liquidity became the issue. But during the ’08 example everything eventually crashed and gold led the rebound into 2009. In the ’11 example precious metals and commodities went straight to hell and the strong USD sucked global capital into the Good Ship Lollipop, err, that is the US markets.

Darned if I know which of these scenarios – if either of them – will serve as our blueprint today. So I am not going to over step my risk management until I get a handle on that. My preference would be for a full out crash in the precious metals that leads a crash in commodities, resource countries and finally developed countries (including the US). But stocks are still playing their rotation game and if the Gold/Silver ratio and USD win out it is possible – per the post-2011 period – that the Semiconductor>Tech leadership thing will persist.

Either way, the short-term has risks and we are not in 2020’s inflationary Kansas anymore. Inflationists think the Fed must inflate again and indeed our ‘summer cool down’ scenario is doing what it was supposed to do, which is to cool that inflationary hysteria, that got out of hand several months ago. Now we are there but at some point a cool down morphs to the real thing and I do not like what the combo of the GSR and USD are doing at all if I am an inflationist or especially, an inflationist gold bug.

If we do get a deflationary tank job across asset markets then the buy in gold stocks could be as amazing as Q4 2008. If not, they will probably be dead money at best or toxic at worst.

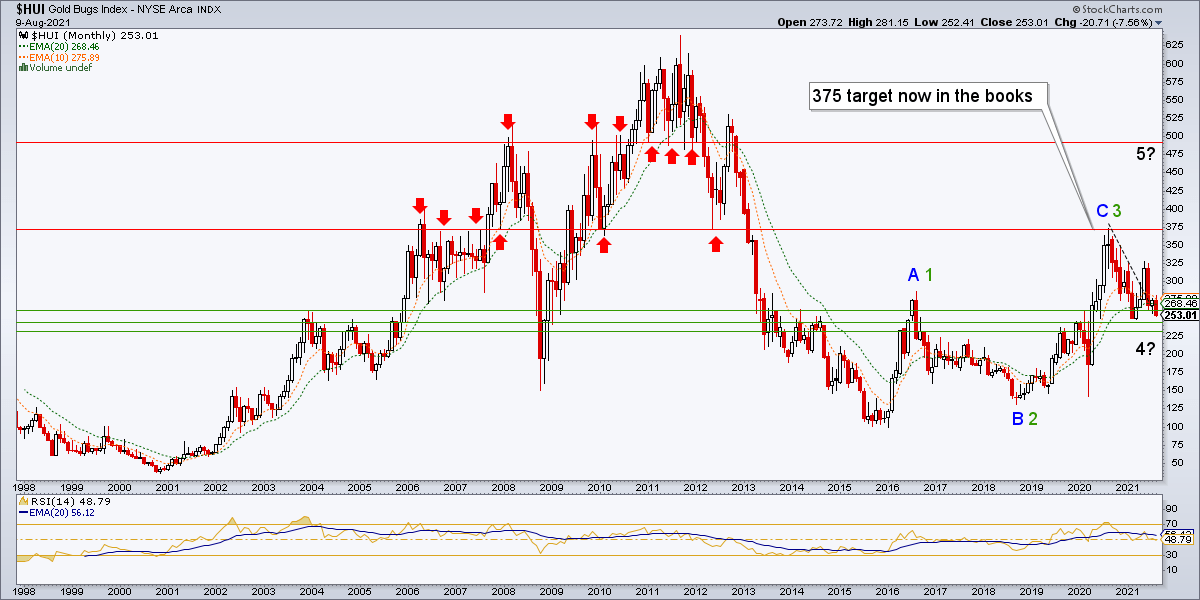

[edit] Per the monthly chart of HUI the situation has not changed a bit. So the GSR/USD stuff above can be filtered with this picture. As we’ve been noting all along, if HUI makes a higher low to 2020 (at where ever point 4 comes in) a 5th leg higher could be something to behold. The optimal situation then is for this picture to remain unbroken even as the index scares all the hangers on out and makes them think bear market.

Of course, the other scenario is that it will have been an A-B-C bear market rally to 375, as originally planned back in 2019. But the look of this chart is of something still starting, not ending. A drop to a higher low would feel like an ending to over committed bugs, but the chart continues to ask us to be aware of a potential bigger picture bullish opportunity within the situation.

[edit 2] Taking it a step further and as pertains to the inflation trades, before getting so freaked out with the Gold/Silver ratio I was 60-70% inflation leaning. So let’s realize that it would be ironic if the guy who called for a summer cool down actually got too wigged out by said cool down and then that’s all it ends up being. So please filter all of this with incoming information from the macro.