Macro markets quake as expected, bonds get a little crazy

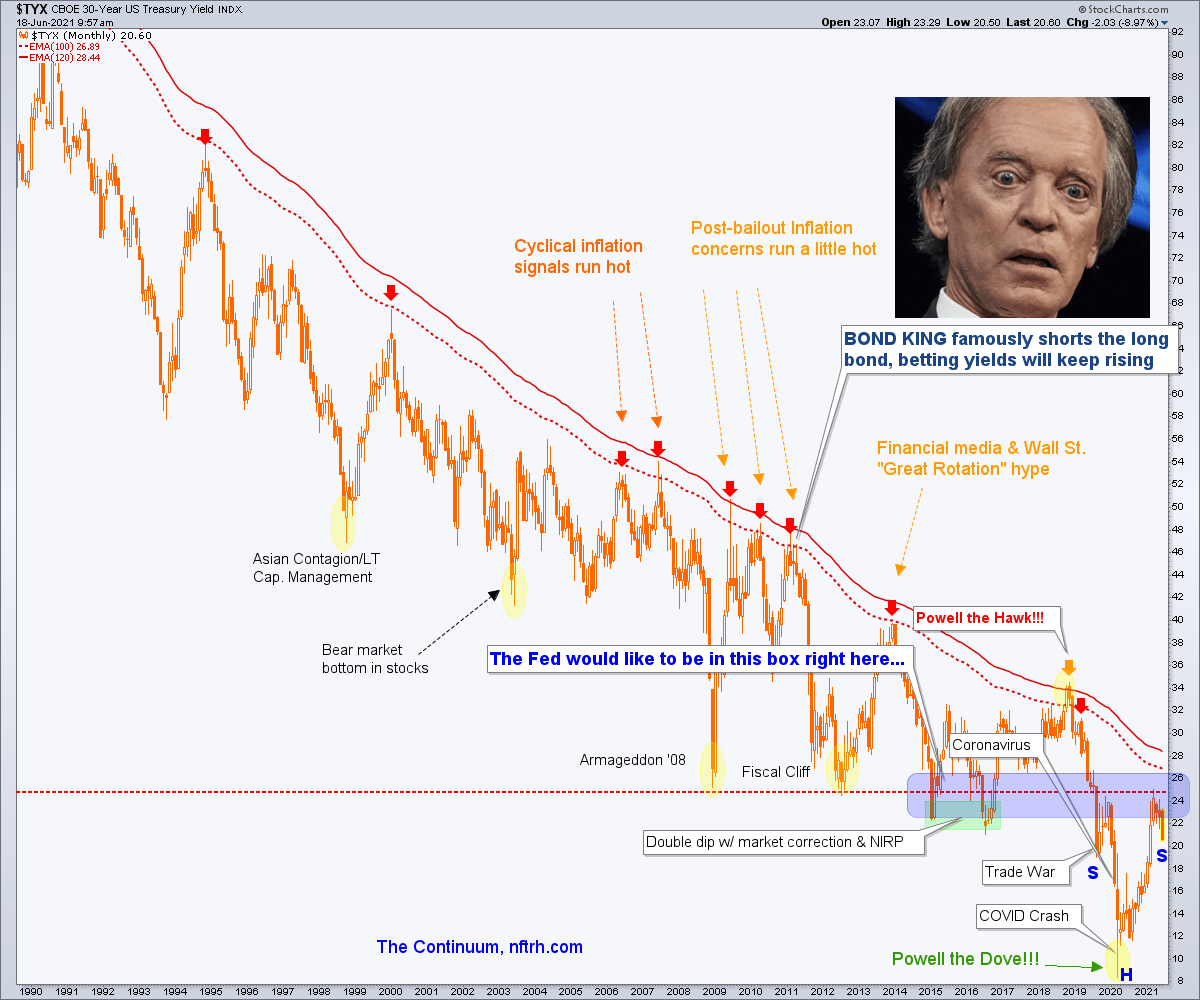

For months now we have been expecting the Continuum to make a roughly symmetrical right side shoulder. That is the cartoon picture of it. The reality of it would be a resetting of the unsustainable (for a Fed wishing to attempt to continue the inflation) rise in inflation expectations. Well, so far so good. How nicely is this right side shoulder coming along?

But there is more. The yield curve was part of the inflation signaling and it has been rolling over along with other inflation signalers since March.

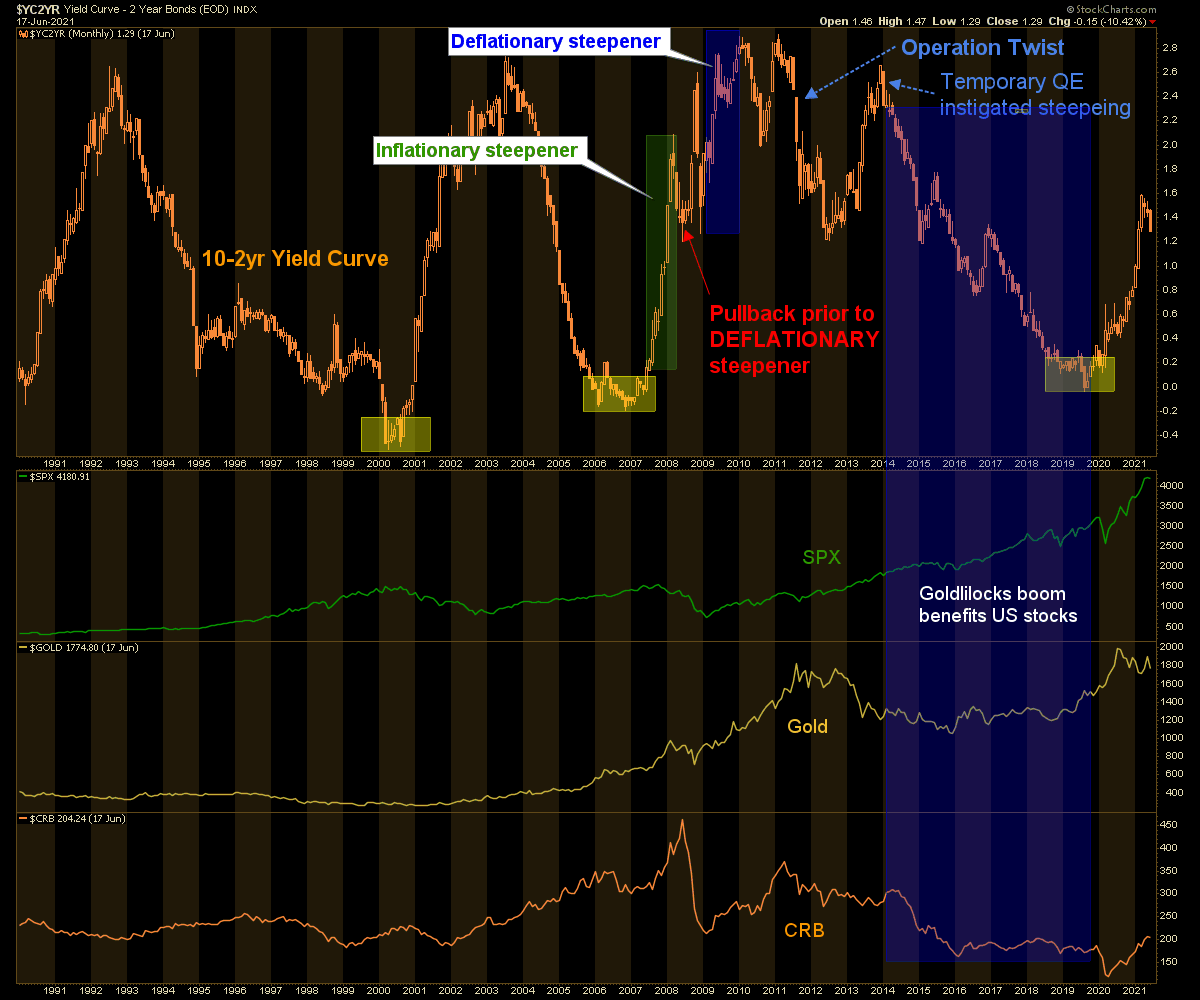

While the Continuum implies eventual further upside in long-term yield (and inflation) levels, there is another alternative to this pre-summer cooling off period. That alternative is as this chart notes, a deflationary steepener. Remember, the yield curve works both ways. It can steepen under pains of inflation (long-term yields rising faster than short-term yields) or deflation (long-term yields falling less than short-term yields).

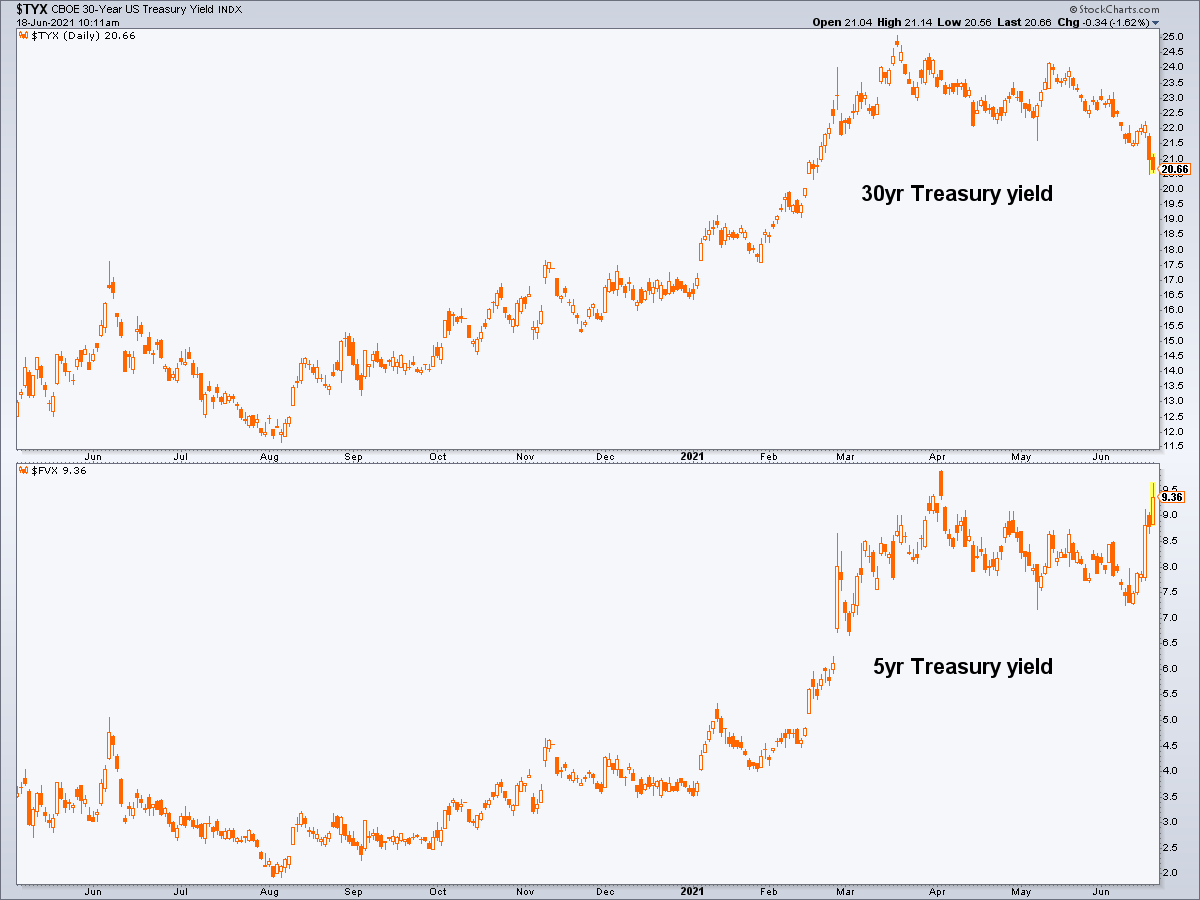

Right now there is strange signaling on the macro with the 30yr yield dropping and the 5yr ramping. That is not inflationary signaling and it is not deflationary signaling. It is, if anything, Goldilocks and/or risk ‘on’ signaling. It’s probably the result of whatever the machines think about the Fed’s ongoing bond manipulation buying regimen. But the net result is that the yield curve continues to ease as it did after the inflationary surge in 2008.

Just a few observations about the bond market at the end of an eventful week.

For “best of breed” top down analysis of all major markets, subscribe to NFTRH Premium, which includes an in-depth weekly market report, detailed interim market updates and NFTRH+ dynamic updates and chart/trade setup ideas. You can also keep up to date with actionable public content at NFTRH.com by using the email form on the right sidebar. Follow via Twitter @NFTRHgt.