October came and went. It’s now November 5th with holiday (and Wall Street bonus) season directly ahead along with the 1 year anniversary of the Christmas Eve massacre in which the machines puked and reversed the market.

This morning long-term yields are up, yield curve is up, inflation expectations are bouncing and stocks are up. Bonds are down and the risk ‘on’ backdrop is dragging gold. All logical to the expected inflation/reflation trade about which my main question has been ‘Q4 2019 or H1 2020?’. Well Beuller, yesterday we noted that SPX jumped the bull turnstile. We also noted that SPX (SPY) has been under performing to global markets for better than a year now.

The NFTRH theme has been “global macro inflation/reflation trade” and unless this is one big bull trap (sentiment is getting ridiculously over-bullish, after all) then it’s starting in Q4. Perhaps Christmas Eve this year will see an opposite event to last year’s crash and reversal.

Personally, I am in a selective mode regarding global stock markets, resources/commodities and materials. A key feature of this bullish reflation backdrop is rising long-term yields; yeah, the same rising long-term yields that had everyone freaked out a year ago. With the subsequent diving bombing of the yield (blow off in the bond) and everyone on the deflationary/risk ‘off’ side of the boat last summer unless the system was about to end in a deflationary whirlpool, the next ping of the macro Continuum would be inflationary. Q4 2019 or H1 2020?

We have asked the long bond’s yield to hold 2.2% in order to remain constructive to an inflationary situation and this morning it is at 2.3% (from investing.com).

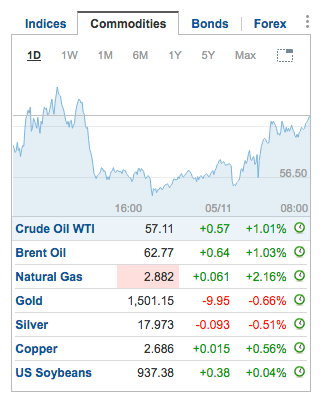

Stock markets are again green.

And very notably and logically, commodities are green while precious metals – which we’d noted had been vulnerably tied to the long bond during the summer’s risk ‘off’ situation – are red and in continued consolidation in ratio to the assets of risk ‘on’ and reflation.

See…

The Bond Yield Continuum and Gold

From that August 8th post…

Gold’s vulnerability, in theory at least, is the fact that it has gone hand in hand with something that is stretched to an extreme.

But the yield curve is steepening again. It’s no great shakes yet, but if it continues this time gold will be just fine as it does have some inflationary mojo to it under certain macro situations.

But for now the raft of cyclical inflatables is out performing and that is consistent with the inflation trade I’d expected at least by H1 2020 but that we may be getting here and now. We’ll have to continue to watch chart trends to see if more of them change to up. I noticed yesterday that items like Materials and Financials were threatening to break out. All part of the plan if it is to be reflationary.

Subscribe to NFTRH Premium (monthly at USD $35.00 or a discounted yearly at USD $365.00) for an in-depth weekly market report, interim market updates and NFTRH+ chart and trade setup ideas. You can also keep up to date with actionable public content at NFTRH.com by using the email form on the right sidebar and get even more by joining our free eLetter. Follow via Twitter @NFTRHgt or StockTwits.