As I’ve been noting again, again, again, again, and again the macro backdrop is marching toward changes. I’d originally thought those changes would come about within the Q4 window and while that may still be the case, it can easily extend into the first half of 2018 based on new information and data points that have come in.

One thing that has not changed is that stock sectors, commodities and the inflation-dependent risk ‘on’ trades and the gold sector, Treasury bonds and the risk ‘off’ trades are all keyed on the interest rate backdrop; and I am not talking about the Fed, with its measured Fed Funds increases. I am talking about long-term Treasury bond yields and yield relationships (i.e. the yield curve).

People seem to prefer linear subjects like chart patterns, momentum indicators, Elliott Waves, fundamental stock picks or the various aspects of ‘the economy’ or the political backdrop. They want distinct, easy answers and if they can’t ascertain them themselves, they seek them out from ‘experts’. But all of that crap (and more) exists within an ecosystem called the macro market. When you get the macro right you then bore down and get investment right. That’s the ‘top down’ approach and I adhere to it like a market nerd on steroids. And with the recent decline in long-term bond yields and the end of week bounce, the preferred plan is still playing out.

So let’s briefly update the bond market picture with respect to its implications for the stock market, commodities and gold.

US Treasury yields are poised to reach the limiters, which are noted on this multi yield chart. We’ve been watching 3.3% on the 30 year and 2.9% on the 10 year (those are the levels of the ‘limiters’ AKA the monthly EMA 100 & EMA 140, respectively).

- This is positive for the stock market at face value because rising Treasury bond yields are a normal part of an economic recovery, which has been in place most notably since we identified the Semiconductor Equipment sector’s ‘canary in a coal mine’ indication back in January of 2013.

- It is also generally positive for commodities, which are correlated to global growth.

- At face value, rising interest rates are bad for gold and the gold sector, because the implication is that money is trending away from having been cheapened, and is paying some return for its holders.

So assuming we are right and the 30s and 10s go to 3.3% and 2.9% respectively, the track should be clear for casino patrons to see their stock and commodity speculations continue paying out. This week’s market disturbance? Well, we accounted for that ahead of time in an NFTRH update on Wednesday morning. But it is not expected to be terminal. If yields remain firm, it will likely either be a healthy and moderate correction or one of those little blips that have sustained the bull market so well lately in the face of bad risk/reward and sentiment profiles.

But when the yields above meet the limiters, that is where the rubber will meet the road. It’s going to be one thing or the other; a full blown inflationary breakout (von Mises Crack Up Boom style) or another failure into a potentially hard drop in yields, possibly right on cue again as the financial media honk yet another hysterical inflation phase. Here again ladies and gentlemen, “the Continuum” ™…

If and when you see 3.3% on the 30 year yield (2.9% on the 10yr) it is advisable to at least run a calculation about what the chances may be that it will be different this time. A lot will depend on how lathered the media and by extension, the public are about inflation at such time and how vigorous the asset party is. But the inflation trade has been stopped dead in its tracks every damned time the yield has hit the limiter for decades now.

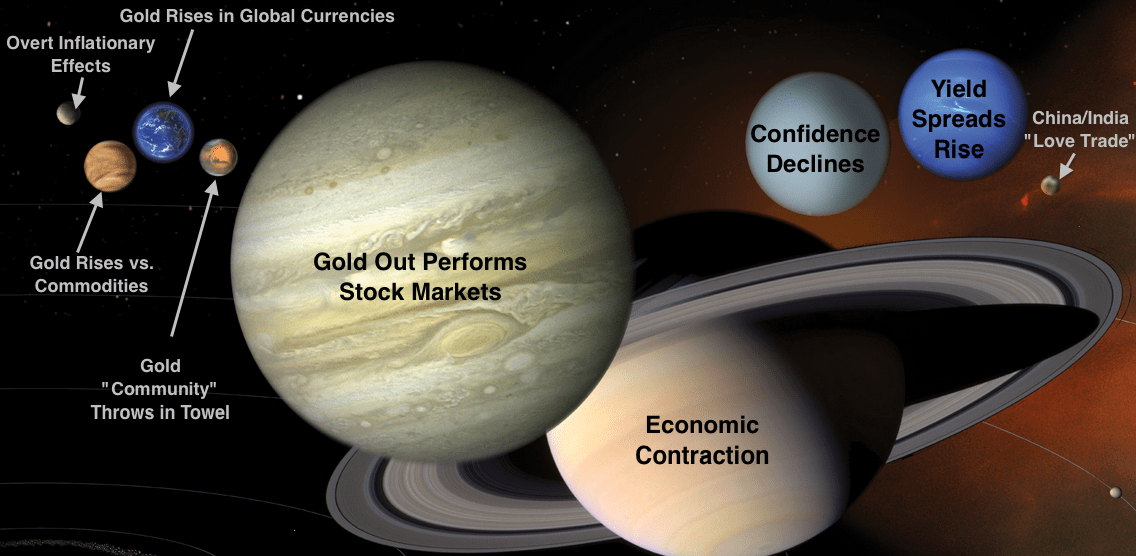

Last week I couldn’t keep my lunch down as a gold “enthusiast” lathered the faithful about how the gold miners are going to lead gold “for a very long period of inflationary time” and that is simply not the way it is going to play out.

The gold sector will step forward when the four largest planets of the Macrocosm ™ align properly.

One of those planets is the Yield Curve. The boom will end, and I find it really interesting that the curve is declining toward a bottoming point while yields on nominal 30s and 10s are rising toward limit points.

On the here and now, even the TIP/IEF ‘inflation gauge’ is in line with our thesis of rising inflationary expectations amid the asset party. You need Thing 1 (rising inflation expectations) to bring about Thing 2 (a hard stop of said expectations) as nominal yields and the curve reach their limit points.

It’s not a good market to be flying blind or following the herd (which will probably get lathered on inflation in the short-term). It’s a good market to have a macro plan. Personally, I am following the short-term inflationary plan but the biggest trades are going to come when it all changes. So its run with the casino patrons for now, but when the right signals are registered let the herd keep running but plan to go in another direction. Gold and risk ‘off’ will take center stage when the inflation flames out but meanwhile, the trend is toward inflation’s limiters up there at 3.3% and 2.9%.

Subscribe to NFTRH Premium for an in-depth weekly market report, interim updates and NFTRH+ chart and trade ideas; or the free eLetter for an introduction to our work. You can also keep up to date with plenty of actionable public content at NFTRH.com by using the email form on the right sidebar. Or follow via Twitter @BiiwiiNFTRH, StockTwits or RSS. Also check out the quality market writers at Biiwii.com.