No Laffing Matter

Last week in NFTRH 872, we covered the Art Laffer mega bull view that is likely cast through a political lens. According to this view the Big Beautiful Bill (BBG) is going to bring on a golden age of economic prosperity. Assuming that the whole enchilada does not unwrap into a deflationary death spiral (unlikely), it’s one elderly gentleman vs. another even more elderly (and deceased) gentleman, “old Ludwig van” (von Mises).

The BBG increases national debt by more Trillions (from a starting point of around $36 Trillion). Laffer apparently thinks this can go on indefinitely to the tune of economic prosperity, while von Mises might have instructed that it is the doorway to hyperinflation.

There is a lot of cross-talk in the picture due to Trump’s wax on/wax off routine on tariffs and trade. Trump may be cooking up a plan to rebate consumers to relieve the costs of the tariffs they bear. Fancy that, it’s apparently as simple as going back to the debt pile so government can fund the people, who are bearing the brunt of government funding that flows through tariffs.

It sounds like rearranging deck chairs on the Titanic to me.

[edit] While watching Trump live in Scotland negotiating a trade deal with the EU, I am moved to add context to the harsh comment below. In mentioning mental health issues – of which most of us have some level, whether minor or major, ourselves, or with those close to us – it’s his ego. It is as a big as house. I think he is actually quite sane, if tunnel-vision focused. That sure can be dangerous.

He’s also the guy, as I’ve mentioned in the past, that I’d have a beer with. I don’t care for him and that ego, but he’s funny and just that type. Listening to him talk for 10 minutes about windmills reminded me of that. When listening to him talk, I often find myself laughing, not at him but with him. Can’t help it.

As for the 70/30 split on Trump-o-nomics, I may have been harsh there too. Let’s adjust it to 60/40, pending a likely interim recession, and with the context that the bottom line is still debt and inflation. The guy gets things done. Good things? Some. Bad or unhelpful things? Some. Very bad (IMO) things? Some. But this guy is tireless. He’s all over the place (hence, my “blunt force object” description). The country sure has needed someone who gets things done. More good things than bad things would be preferred, economically speaking.

All that said, I think the damage being done to the USA, culturally and socially, is going to be the worst of it. Now I fade back from the Trump focus so he doesn’t distract me from my job.

Personally, while I don’t like Trump the human (and deplore most reality TV stars) and frankly think he has got some significant mental health issues, I am about 70/30 on him, economically. 70% that he is an unfocused train wreck (or iceberg) waiting to happen, and 30% that he and his advisers know what they are doing to a tune approaching genius. Or at least, Sub-Genius… bonus points if you know who this is (the meme of all memes, decades before memes became a thing)…

Back on track, economic cycles are what they are. While government, regardless of party in power, has always been in the game (fiscally), rigging things as best it can (e.g. Biden/Yellen in 2024), neither government nor the Fed working in combination (monetarily) have been able to forestall previous economic bust cycles.

Let me rephrase that. They have forestalled them, but they have not eliminated them. 2001 and 2008 in particular for the modern era. I don’t count 2020 because that was an exogenous event, prompting a response by the Powell Fed and the U.S. Government (under one Donald J. Trump) to go balls out in inflationary response.

Last week in #872 we looked at some leading indications on the economy that are rolling over (Commercial Real Estate, Construction Spending & Housing Starts). The benefit government is receiving and now considering partially doling back out to we the dupes (the marks) is not going to stop a bust, if one is in the offing. If our macro view is a good one, the question is whether it’s going to be a doorway to a hyperinflationary inflationary “crack-up boom” or a more traditional interim deflationary cycle, followed by a crack-up.

Tariffs, tax cuts, rebates, this, that… it’s deck chairs on the Titanic. But that ship took a long while to sink. In market terms it can take years. The economy has been trying to unwind the excess since before the Biden admin began its 2024 (pre-election) bailout efforts. But it was not allowed to unwind. The can got kicked down the road. My educated guess is that there is still Biden era liquidity sloshing around the system.

While M2 money supply has continued its upward trajectory from the Biden reelection operation…

…”real” M2 (deflated by CPI) appears to have troughed. Has the damage already been done by the hawkish Fed (except for that strategic pre-election double rate cut last year)?

The Fed’s balance sheet implies ongoing tightness, which would normally precede a recession.

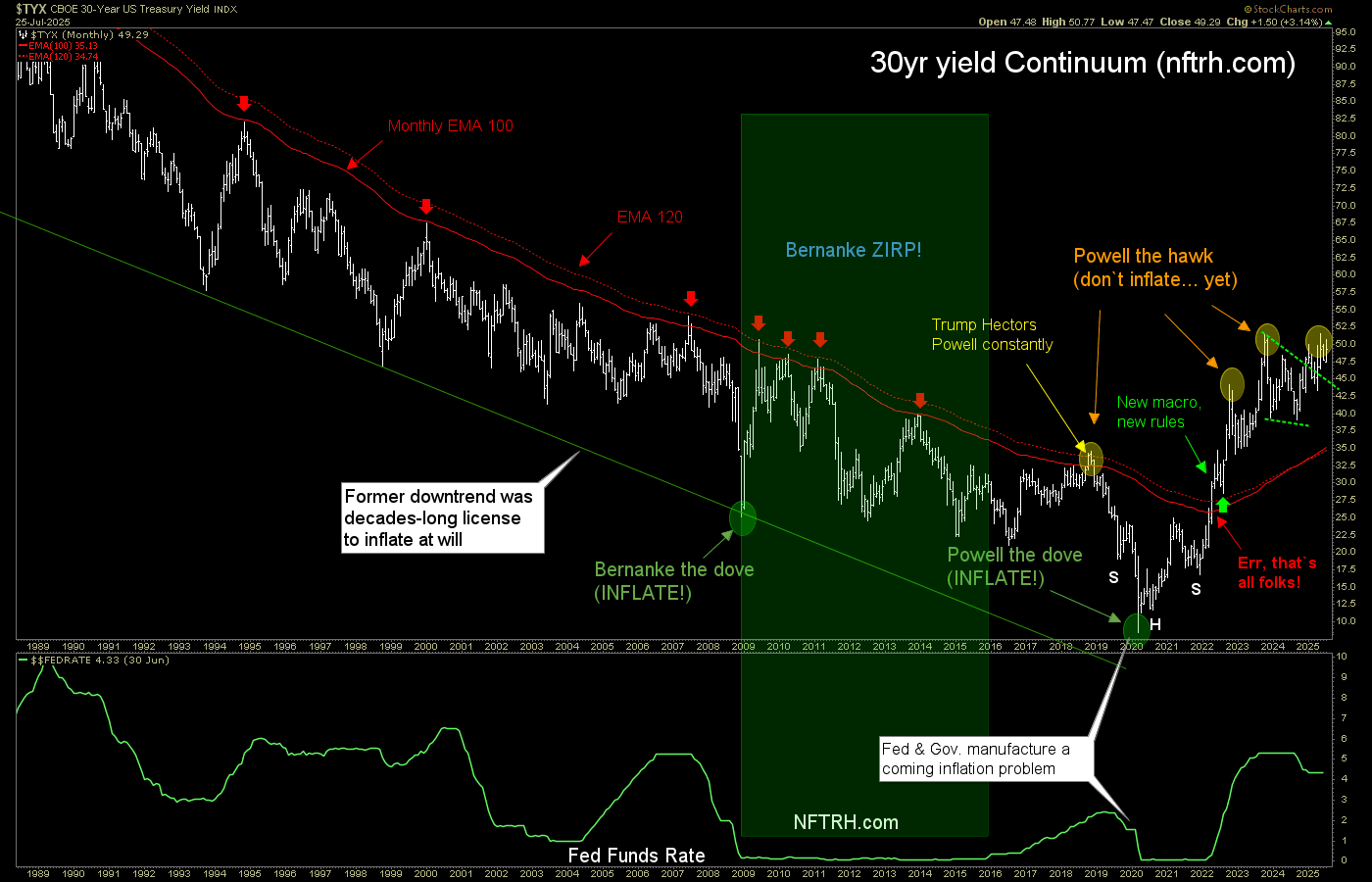

But our theory is that the Fed is less relevant now, as government’s fiscal policy assumes control. Not for nothin’, but behold the visual symbolism of the powerful force known as Trump standing beside and hulking over the frail looking Fed chief. Aye aye aye… the blunt force object and the egghead.

This graph shows the velocity of M2. While stock market bears and deflationists have used this measure for at least the last 2 decades to talk their book, declining money velocity has only served to prompt new inflationary bailouts.

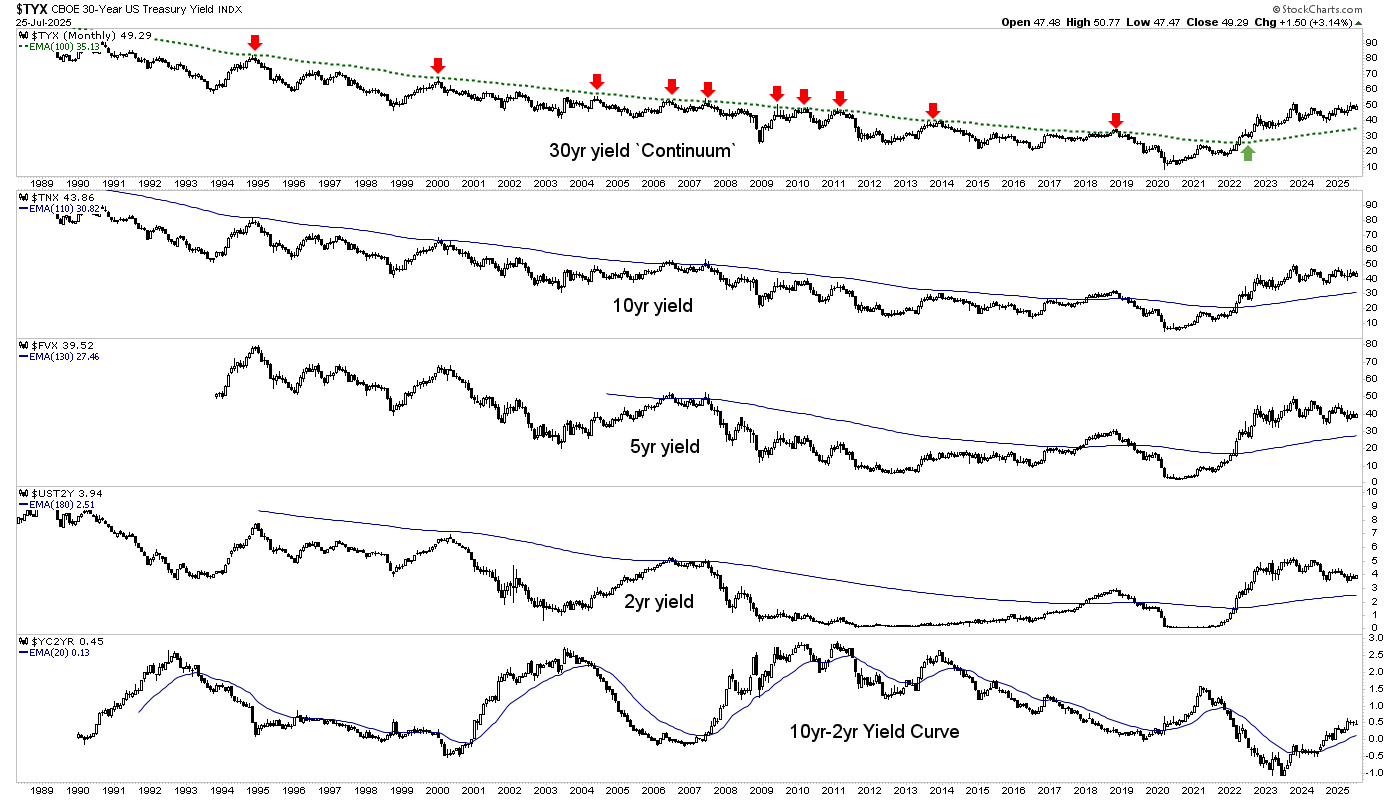

Much like the Continuum did. In 2022 the situation changed for the long bond’s yield and in the same time frame the chart above lurched upward. The trend is still down, but it bears watching because we need to determine whether the next negative economic issue is going to be deflationary or inflationary (I continue to lean interim disinflationary/deflationary prior to the next major phase of inflation, but we need to be flexible on this as events unfold).

Interestingly, and positively, Household Debt to GDP is in a downtrend. The consumer is deleveraging and that is a good thing.

But our households exist under the economic tyranny of the government. And with a government supposedly by the people and of the people, that means we Americans are all leveraged to debt near historic highs. What’s more, the Trump administration shows no signs of wishing to reduce this debt. At least through sound practice.

Unsound practice? Well, they can attempt to inflate the debt away. And now we are back to arranging deck chairs on the Titanic. We are back to von Mises and a potential inflationary “Crack-Up Boom”.

Even Treasury yields don’t yet seem to know if we are going inflationary or deflationary as the 10-2yr Yield Curve steepens (an economic bust signaler), but nominal yields across durations go sideways to varying degrees. With the long bond’s yield grinding slightly upward, that seems to indicate that the bias is still inflationary.

The YC can steepen inflationary or deflationary. Right now it’s a mishmash. But why should this market be easily interpreted? It’s a noisy and wild macro out there.

I could get us lost in the weeds with the economic stuff, but that is enough for this week. Let’s move on to markets.

U.S. Stock Market

Per the in-week notes on Friday:

“I am going to mitigate some Fed week mayhem risk (not that the Fed matters as much anymore, but the machines always seem to get riled up on FOMC week) by doing some more profit taking.”

Take profits I did. I found myself being a little content with my “bull stock” holdings and their performance, and then got rid of several. GOOGL, XYZ, OKTA (both positions), GM, AMZN (one of two positions) and in the metals patch, PALL. Also as noted, a couple silver stocks were released for reasons…

“I reserve the right to be wrong, but I have reduced exposure to silver stocks and also took my profit on Palladium (not really related, but sort of related if you know what I mean).

Remember who was positive on silver vs. gold back when the silver bugs were crickets? It was us. Again, I could be wrong here, but those damn bugs are so loud now. The target for silver has been 40 for months now. It ticked 39.52 this week. It usually over-shoots (in both directions). But I’m going to be comfortable and evaluate going forward.”

But mainly, the objective was to cut down “bull stocks”, which were added during angst and sold during euphoria. They told us in Market Wiseguy 101 that is how to do it if you’re trading rather than investing. And folks, I am not investing in this sentiment relief rally. I bought it when they were afraid and I sell it when they are euphoric.

I retained ALAB, which I am in love with (warning), APPL and a few other items. But for one day’s profit-taking, I feel I accomplished what I wanted to. This with FOMC week upon us, a time when there is often more energy in the markets, for whatever reason.

This market is the same one people could not wait to puke out of in April. There is no technical sign of the rally’s end. Indeed, it accelerated last week. But it is the summer dog days, FOMC week is here and SPX is as far from its 50 day moving average as it usually gets. Profits, please. Now the pig can do whatever it wants.

Market Sentiment

Dumb money loves itself some stonk market. Smart money indicators are fading hard. Market risk is quite high.

Fear/Greed index is in fairly dangerous territory. It would be worse, but I think CNN’s calculations are in error. The only “neutral” of indexes components is Volatility, and frankly that looks like the most extremely over-bullish reading of the components. Markets are solidly in Extreme Greed territory.

NAAIM (investment managers) were over-bullish but muted. However, that was before the market popped on Wednesday. They are surely more over-bullish now.

Finally, AAII have not yet given a big, bull ending signal as they continue to mush around at 36.8% bullish, 29.2% neutral and 34% bearish.

Sentiment Bottom Line

Dangerous. Those who were scared in April are quite brave now. It’s how markets work.

Precious Metals

Ref. last week’s NFTRH+ updates on gold and gold stocks (GDX). They still apply. As for silver, the next upside target of 40 was nearly registered (39.52) before a pullback.

I became cautious about the bugs touting silver. To be fair, there is always silver bullishness out there, perma-style. But it has grown more intense lately. Much more so than it was in April-May when gold was leading everything (as it often does) and silver was tanking.

Back in mid-2016 we had to become quite cautious on the precious metals as gold’s bigger picture fundamentals eroded amid a cyclical upturn, led by the Semis. Back then I clearly remember a widely followed supposed Tech expert who was always bullish on the precious metals and rarely on Tech/Semi taking the exact opposite stance to mine. It was leading the gold bug sheeple to a slaughter. Wash, rinse, repeat.

I mention it because it and similar instances annoy the living crap out of me, because by following the market’s signals I do not get to do the kind of touting that brings in herds of readers and hence, subscribers. Well, guess who turned out to be right and who led many a bug down a sink hole.

This time is different. New macro and all. Back in 2016 I began tuning out raving silver bugs that were leading the precious metals complex higher amid a cyclical inflationary environment. Gold stocks, especially, were not going to benefit from that macro. At best, they’d be nothing special. At worst? Well, HUI did the worst. It took a 54% haircut in the first downturn (to point 2’s higher low) of the new bull market that began with that 2016 up-thrust. I don’t know about you, but I am not riding 54% haircuts, bull market or not.

I’ll make clear that this is not like 2016. Completely different macro, assuming the 70% surety I have that Trump-o-nomics is either going to fail or be rudely interrupted. So my apprehension about the silver cheering is simply a mid-summer, Fed week thing. I don’t think it’s like point 1 on the chart above, which was put in amid gathering positive cyclical economic signals.

On the intermediate-term picture, I think we are still on a drive to point 5 by HUI and that would imply silver taking out the target of 40. I have held onto everything I want to hold onto and may find myself adding more precious metals positions before long.

The Silver/Gold ratio trades (“SGR trades”) are still intact as well with the TSX-V/TSX ratio firmly trending up but correcting its impulsivity a bit and the SGR trending up in an orderly manner. In my opinion, the very orderliness of the SGR probably means that the trade is not at all done. Silver usually ends trends in dynamic fashion, whether nominally or in relation to gold. So again, right now I am managing the possibility of perhaps some summer turbulence, not the end of the move.

This long-term monthly chart has a similar message with gold having led, silver still in bull mode, CRB index still forming a bowl/base for a would-be attempt to break resistance, TSX-V trending up and the Silver/Gold ratio not having gone much of anywhere. Again, if the extreme low the ratio came from this time goes the way previous extremes lows have gone, there would be more upside ahead. Potentially a lot of it.

With that in mind, I’ll be prepared to increase positioning when I get a better read on the next couple/few weeks. Meanwhile, the ratio of the Silver Miners ETF to the Gold Miners ETF hints that there could indeed be a little grinding or turbulence in the short-term. The ratio has cracked its daily EMA 20 for the first time since the rally started. Could be nothing. Could be something. But even here, if it is a short-term negative something the play would not get broken unless it were to lose the moving averages and make a lower low to the June low.

As for the commodity complex…

- Oil and Gas are struggling. As such, I took a frankly unexpected loss on AR but still hold the sector, XLE. But I do not now and have not to this point favored Energy, Trump or no Trump.

- I think it is pretty interesting how how dirty Energy is languishing while clean Energy (is it really that clean when considering the dirty carbon it takes to manufacture its components?). The Solar ETF is trying to bust its downtrend and looks buyable if you believe solar has a future. It does in much of the world, and may again one day in the U.S. as well.

- Copper continues to be a featured metal that is globally strategic, even critical. It is near all-time highs at 5.83/lb. while Copper Miners have not kept up. This may be an indication of a coming correction in the copper price, which would fit the economic recession view. I considered taking my profit on COPX, and am still considering it.

- The Uranium patch is still in rally mode. I am holding NXE for its chart and its future, but will require it to hold the shaded short-term support area in order to continue holding.

I am aware that Rare Earth Elements have gotten all too much hype over the last 6 months. But in the case of MP, the hype manifested in the government actually putting its money where its mouth is, with the DOD investing heavily in this strategic U.S. producer and processor of REE. If it were in the IRA instead of the taxable account, I’d have probably taken the profit. But for the foreseeable future, it sits in the portfolio.

Elsewhere in the REE patch, Aussie producer LYSDY is more under control and quietly held in the Roth IRA, while the more speculative IDR is also held with no tax constraints. While I don’t want to sell it, I may sell it as a 28% tax free profit it tempting. It will depend on the market. I did not want to shed too many positions too quickly last week, just on speculation that some market volatility could be upcoming.

- To this point the Nickel price has been planted in the ground while Ni prospect TLOFF (TLO.TO) has pulled its moon shot. Last week Ni started to rise to test its 200 day average within an intact downtrend. We’ll see if it’s got more upside. Meanwhile, I’ve got my TLO position where I want it in relation to other exploration items, a basket of which is being cobbled together.

Bottom Line

The case for commodities in an inflationary macro that is increasingly in war mode (literally, and economically) is a strong one, especially for the more strategic commodities like REE, Copper, PGM, Uranium and maybe even once again, Nickel.

We’ll continue watching silver vs. gold and TSX-V vs. TSX for internal technical indications. Meanwhile, if there is an interim deflation scare (liquidity event), commodities would likely get clobbered on that interim basis.

U.S. Dollar

And who would potentially benefit from a liquidity event? Uncle Buck, that’s who.

But the buck made a bounce off of the positive RSI and MACD divergences and failed as usual at the downtrending 50 day average. However, it did hold support (defined by the 2021-2022 highs, not visible on the daily chart), so if there is a summer market disturbance USD could still gain traction on a bounce. However, it is technically bearish until proven otherwise and would not even think about breaking its major downtrend unless it were to take out the May high of 101.97.

Portfolio

Gold is long-term risk management & monetary value/stability in a balanced portfolio.

Taxable Account

In order of position size. Some positioning was trimmed, mostly from profit taking in “bull stocks” like XYZ and OKTA, as well as some trimming of AMEGF (AE.V) and TLOFF (TLO.TO) to bring them closer to other basket items (though still largest positions by a good margin).

Speaking of basket items, these exploration stocks will generally be noted as (basket) going forward. This means I consider them speculative, and as a group. I have a couple geos and a couple pals for fundamental guidance. But ultimately, mineral exploration is Speculative with a capital S.

The taxable account carries very high cash levels as long as cash and equivalents are paying out. This is considered a savings account of sorts, rather than a speculation or even investment vehicle. The goal is to speculate around the periphery of that. In another market phase (e.g. post-crash), the account may get much more in the game.

Trading Account

No positions.

Roth IRA (non-taxable, no contributions)

I am obviously a little dubious about the chart’s breakout from consolidation to another high. Hence, locking in some profits. Okay market, go ahead and prove to me that there will be no classic July/August market disturbance and I’ll continue to play bull. But in the IRA especially, profit-taking is always good.

Cash is up to 82% now as the profit-takers axe came down on bull items like GOOGL, AAPL, AMZN, OKTA, along with PALL. Some other riff raff was dismissed as well. It just felt time to reel it in a bit and evaluate. No big shakes.

Again here, the exploration stuff will generally be denoted (basket).

Cash & income-generating Equivalents are at levels that are right for me and my real-world situation. Your situation is different. Cash will be adjusted as needed.

Refer to the Trade Log under the NFTRH Premium menu at nftrh.com for trade info, if interested (not that you necessarily should be). Also, you can follow on X @NFTRHgt for notice of updates.

NFTRH is not to be distributed to third parties without prior written consent

Notes From the Rabbit Hole (NFTRH) is a weekly market report in which we provide analysis on financial markets. We make every effort to provide accurate and high quality content, but this analysis ultimately represents our opinions and these opinions are provided without warranty or guarantee of any kind. See full terms & conditions of service under the ‘About’ heading in the main menu.

Bob Dobbs for President!

Nice, Steve!