Something changed just before, during and after Armageddon ’08. That something is that the impulsive rise in growth stocks vs. value stocks (2007-2009) then maintained a grinding uptrend until a hyper trend (i.e. bubble) began to form in 2017. And this year it’s just been full frontally vertical.

Why would this be? Well, the easy answer (or promotion) will be that growth stocks are growing into their future leadership, as they tend to be innovative and destined to supply what a future society and economy need. Okay, okay, we get that. In 2001 the same kind of bubble popped and Warren Buffett suddenly did not look so out of touch.

The problem is those valuations. Believe me I know, I own some and have owned several this year. Ridiculous valuations (as I recall) like DOCU, AMZN, ZS, TDOC, even MSFT, a growth stock of decades yore and still valued as one today. But it goes further than simply claiming that a bunch of Robinhood kids are driving the action. Again, the ratio has been going up since 2007.

MarketWatch weighs in this morning with an article on the subject.

First of all, the article opens with this…

Value stocks have started to perform better than growth stocks.

Well no day trader MarketWatch, they haven’t. Here is the ratio of the two ETFs (IWF & IWD) highlighted in the article. All the ratio has done is make a couple pullbacks to test the up-trending SMA 50. However, that lower high last week is at least a slight hint that a successful test is not in the bag. At the very least that’s only not false information for people trading every twitch of the market. As it stands now Growth/Value is completely intact.

From the article:

Diane Jaffee, a senior portfolio manager at TCW Group, said in an interview that “valuations for value stocks, as represented by the Russell 1000 Value Index, are the most attractive they have been, relative to the Russell 1000 Growth Index, since 2001.”

She was talking about a comparison of forward price-to-earnings ratios for the indexes. Here’s how those ratios have moved over the past 20 years:

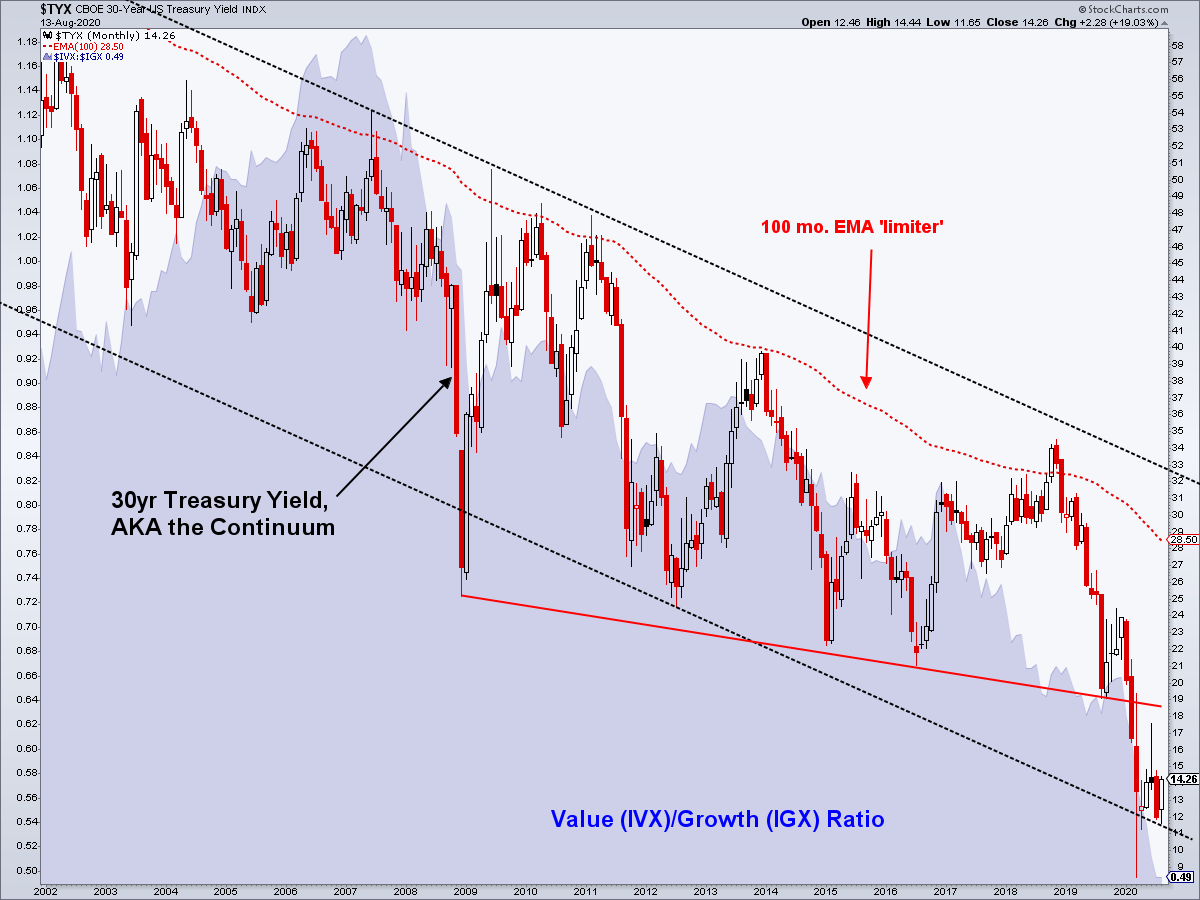

Yes, fine. But my thesis has been that value stocks tend to drag around a lot of debt on which they pay dividends that Grandma loves, but the Robinhood kids don’t much care about. Yet, in creating the chart below I realize I have been wrong in carrying an assumption that rising long-term yields would be bad for value stocks. Quite the contrary, obviously, as long as the Continuum stays in bounds (i.e. below the limiter, which was impaled in 2018 creating a mighty hawkish Jerome Powell back then).

Side note: Before Greenspan took us off the charts and paved the way for ever more sublime policy innovation debt was not such life or death issue. But now it is. The whole damn system is levered on the stuff and the Central Bank uses it routinely to implement its MMT TMM (total market manipulation). It seems like no coincidence that Value/Growth has changed character in the post-Greenspan years.

So I was thinking that rising rates would hurt these debt stuffed companies and that is why nobody wants them. But the chart says that if yields rise there could indeed be a shift back to Grandma’s point of view. That could be the case as long as yields stay limited by the upper bound we’ve carried for many years, the monthly EMA 100 on the 30 year yield. Because if the secular bond bull ends (yields break the forever downtrend) then it’s all going up in smoke in my opinion. As a side order, you just watch how fast who ever is Fed chief at the time flips hawkish again as Powell did in 2018.

Thus ends our little foray back into the Value/Growth debate. It is not a stretch to think that the Growth/Value bubble could soon blow out. That is because it is quite possible that this phase of the bond bubble already did blow out in 2020, with the deflationary angst of March-April. Yields could rise to or toward the Continuum’s limiter if a small cyclical bear market comes to bonds.

Speaking of value, NFTRH will still be valued priced after the soon to be implemented price increase. But the value has never been greater than it is right at this moment. Sure, it costs more dollars than when I launched it in 2008, but it’s also providing orders of magnitude more in comprehensive services to its customers. When I ran a physical company I learned that customer service and continuous improvement are Things 1 & 1A. Nothing’s changed. It’s a continuum.

A price increase will be in effect on September 1 ($38/mo, $390/yr). Subscribe to the value-priced NFTRH now to lock in the current rate (below) for the life of your subscription! Current subscribers never see increases and have never seen increases since the service began in 2008.

NFTRH Premium (monthly at USD $35.00 or a discounted yearly at USD $365.00) for an in-depth weekly market report, interim market updates and NFTRH+ chart and trade setup ideas. You can also keep up to date with actionable public content at NFTRH.com by using the email form on the right sidebar. Follow via Twitter @NFTRHgt.