As we wait to see if yesterday’s interest rate signal is confirmed as the beginning of the countdown to the 10yr & 30yr limit points (2.9% +/- & 3.3% +/-, respectively) I’d like to update how the US sectors are doing.

But first a couple of notes…

- If yields close the week in breakout mode per the charts in yesterday’s public post, it would go a long way toward confirming the breakouts.

- The rough game plan makes an assumption that some components of the stock market will continue to rise with yields into the potential termination points at the limiters (more on this in NFTRH 471).

As noted in yesterday’s update I have let the market instruct that I’ve been wrong in holding too many individual stocks while trying to balance the interest rate view, and have let the move in yields instruct about where to lean going forward, which will be mainly through leveraged and unleveraged sector and index ETFs.

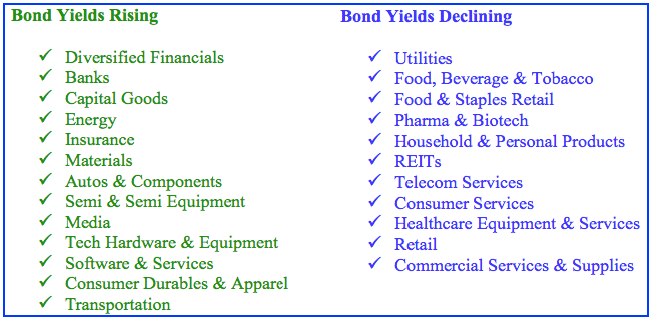

Here is the yields graphic for reference, with those toward the bottom of each column being the least sensitive to the respective yield conditions. If yields continue to move up near-term, the items in the top half of the green column will theoretically benefit most, and the top of half of the blue column the least.

First, here is the Bank ETF vs. SPY. If the rate move is real, this ratio will have to do some catching up. That could be used as another way of confirming the yield move.

So let’s get an update of how sectors look vs. the S&P 500 (SPY) and vs. each other in light of yesterday’s yield move. Financials and Materials look very good relative to SPY. General Healthcare is getting croaked by its Pharma and Biotech weighting (note that Medical Devices, which is actually part of ‘Healthcare Equipment’, is doing fine). Technology and Industrials are fine as well, in line with the yields correlations. One would think Energy would get bid as well, and with nominal XLE finally touching the SMA 200 for test yesterday and today, maybe it will yet resume its upward move.

Here is IHI making a bull move vs. XLV.

Against SPY however, IHI is not so impressive. So while Medical Devices are good for Healthcare exposure, they are nothing special stand alone.

Indeed, recall that the big picture for this former leader may have put in a double top already. Nominal IHI still looks bullish, however and I have some exposure.

Here is the train wreck known as Biotech vs. XLV. I’d purposely held IBB and AMGN due to lack of clarity on the interest rate view. With yesterday’s action, I got some clarity and sold both items.

Small Caps are in a bullish flag vs. SPY. A couple of things here; Small Caps often have relative strength when the USD is strong due to their majority of domestic business. But rising interest rates are not a benefit, so maybe it’s a wash. Regardless, this is a bullish consolidation as long as it holds the moving averages.

Semiconductors lead Tech and SPY, and yes I regret not just holding all positions since becoming bullish the Semis when it seemed few others were back in spring of 2016. But it would be impossible for me to still be long because this has long since become a momentum fueled play, IMO gamed to the hilt. It is however, still a good indicator on coming events. I’d expect Semi to diverge Tech as an early indicator of when the manic speculation is going to flame out.

If you can think of other sector views you’d like to see pop me an email and I’ll see if I can add them to NFTRH 471, which is going to begin the process of managing the macro backdrop now that it seems to be getting clearer. In the near-term the above pictures can help us know where to trade. In the intermediate to longer-term the macro analysis will guide on the next big play which again, IF this interest rate move is real, would be coming at the 10yr & 30yr yield limiters.

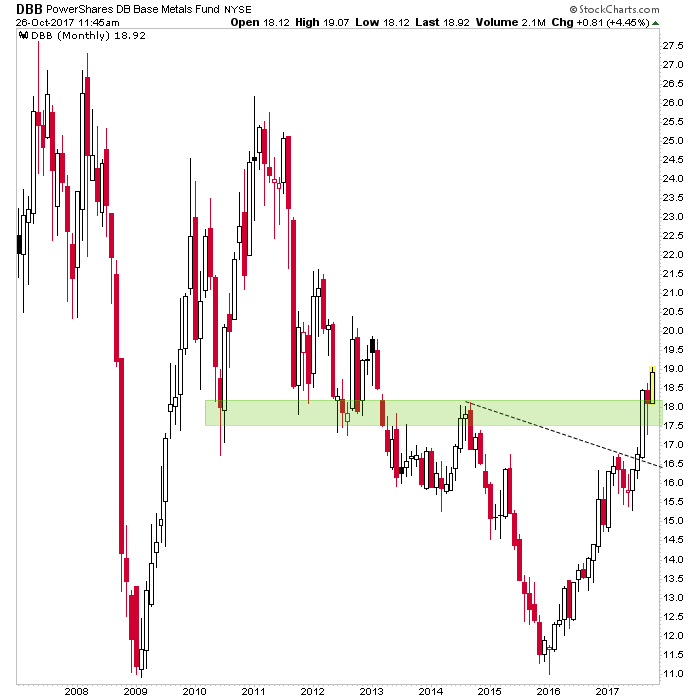

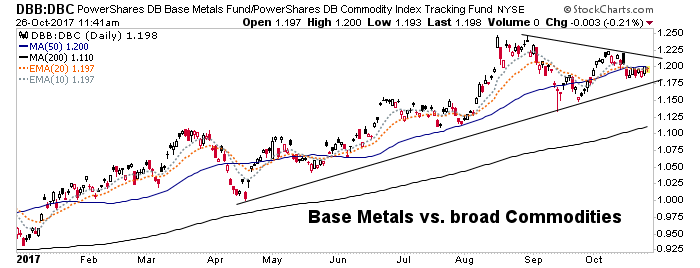

As a final note, to illustrate how I’d like to fix what I’d been doing wrong in owning too many stocks I’ve compacted the still bullish base metals view into one ETF, which is the Industrial Metals holder DBB. Here is its still constructive view vs. general commodities.

And here is its nominal monthly view, similar to the still-bullish GYX index.