I did not make the point clear in the previous post but as NFTRH subscribers may recall, it is the Semi Equipment companies (they that supply the chip makers with Fab equipment) that are the Canaries in the Coal Mine’s Canary. In other words, they are the early mover (front end industry) to a new Semiconductor cycle, whereas the chip makers are the back end. Hence, the equipment book-to-bill (b2b) ratio is important.

Anyway, as you may recall we successfully NFTRH+’d Intel for a second time and then the SOX broke upward. To clear up any confusion, Intel is obviously an end user of Fab equipment.

If the b2b continues declining one might look at some equipment makers (like AMAT, LRCX, etc.) breaking out with the SOX with a suspicious eye. We did by the way discuss in depth some dynamics to a potential ← [key word] upside stock blow off in #318.

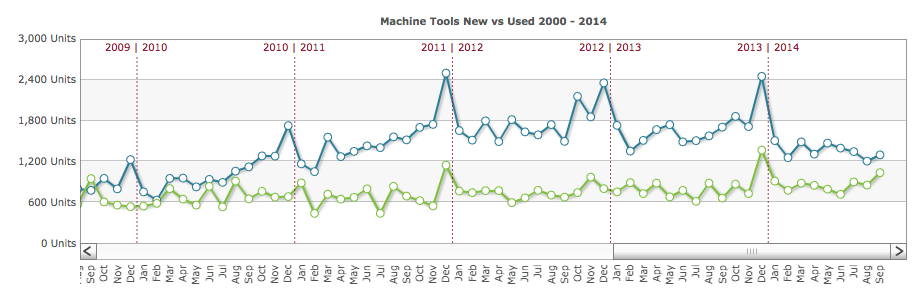

Equipment stocks blowing off with tanking fundamentals would be just such an actionable dynamic. This is similar to the year end bump we are expecting in machine tools. In other words, if/when machine tool sales goose up due to normal year-end tax considerations and certain stocks rise in tandem, while fundamentals actually degrade due to a cheap Yen/strong dollar wearing at the manufacturing sector… well, you get the idea.

Ain’t the macro fun?