Summary

- US Stock Market: Why, it’s bullish! What’s more, SPX took out 4300 and now the next objective – if what I think is a FOMO induced blow off continues – is the 4800 area. Risk is rising every step of the way. Still Goldilocks, led by Tech. But if the rally is to continue there could be internal sector rotations to come.

- Market Sentiment (US): When we began the rally theme way back in Q4, 2022 the aim was to build a pervasively over-bullish sentiment backdrop born of FOMO driven MOMO. Well? That is what is happening now. With extreme bullishness comes extreme sentiment risk, which will only increase if/as the market goes higher. Sentiment is not a timer, but over-bullish sentiment will be a condition of the next market top.

- Global Markets: Mainly bullish as well. It’s an anti-USD situation, after all. Japan is an outstanding performer as it targets our years ago plotted upside of Nikkei 35000 or so based on a long-term base breakout (could be a beneficiary of the weak USD/bearish Yen double whammy). India, bullish in blue sky. EM/Asia extending the trendline breakouts and China is also making some noise. Global will be subject to the USD discussion below, much like commodities and most US sectors.

- Precious Metals: It’s a normal correction, especially as it comes during a cyclical party phase (eh, Garth?). There is potential for an interim bounce in the metals and miners. But the targets generally looking for a higher low to the March lows are still the best, unless/until the 50 day averages and then the May highs are taken out.

- Commodities: USD? Up? Down? The report contains much discussion on that topic. A commodity rally sooner than expected could result if the buck breaks down. As yet, USD holds support.

Inflation

I found myself buying commodity/resource related stocks last week. The trends are down in the broad commodity complex (CRB), in headliners like crude oil and industrial metals, while NatGas has been trying to base after getting bombed last winter.

Several stocks I added are bombed out, like NatGas play AR, Rare Earth Materials play MP and Fertilizer play NTR. Others, like unique Energy stock NOG and Uranium producer CCJ have pretty good charts. So on the plus side, I do not feel like I am chasing the market’s FOMO, as buying bombed out charts sure does not feel like FOMO. But it does feel strange because we have been tracking and favoring the disinflationary Goldilocks theme (to turn deflationary) all year and she decimated the stuff noted above.

A friend, fund manager Mike Churchill, ponders whether there could be “some kind of quasi-QE from this [debt ceiling raised yet again] event”. The US dollar, anti so many markets and often a taker of market liquidity when it is rising, weakened as if on cue of the debt deal. A related source of liquidity would theoretically be the ole’ “stealth QE” play, whereby the Fed acts tough while using big brain Ben Bernanke’s esoteric tools behind the curtain to manipulate liquidity streams into markets. The spate of bank meltdowns turned out to seemingly matter very little (as we’ve noted all along) after the Fed and US government applied a band aid that may have also pumped liquidity.

In pondering the US dollar, I have had two very different views.

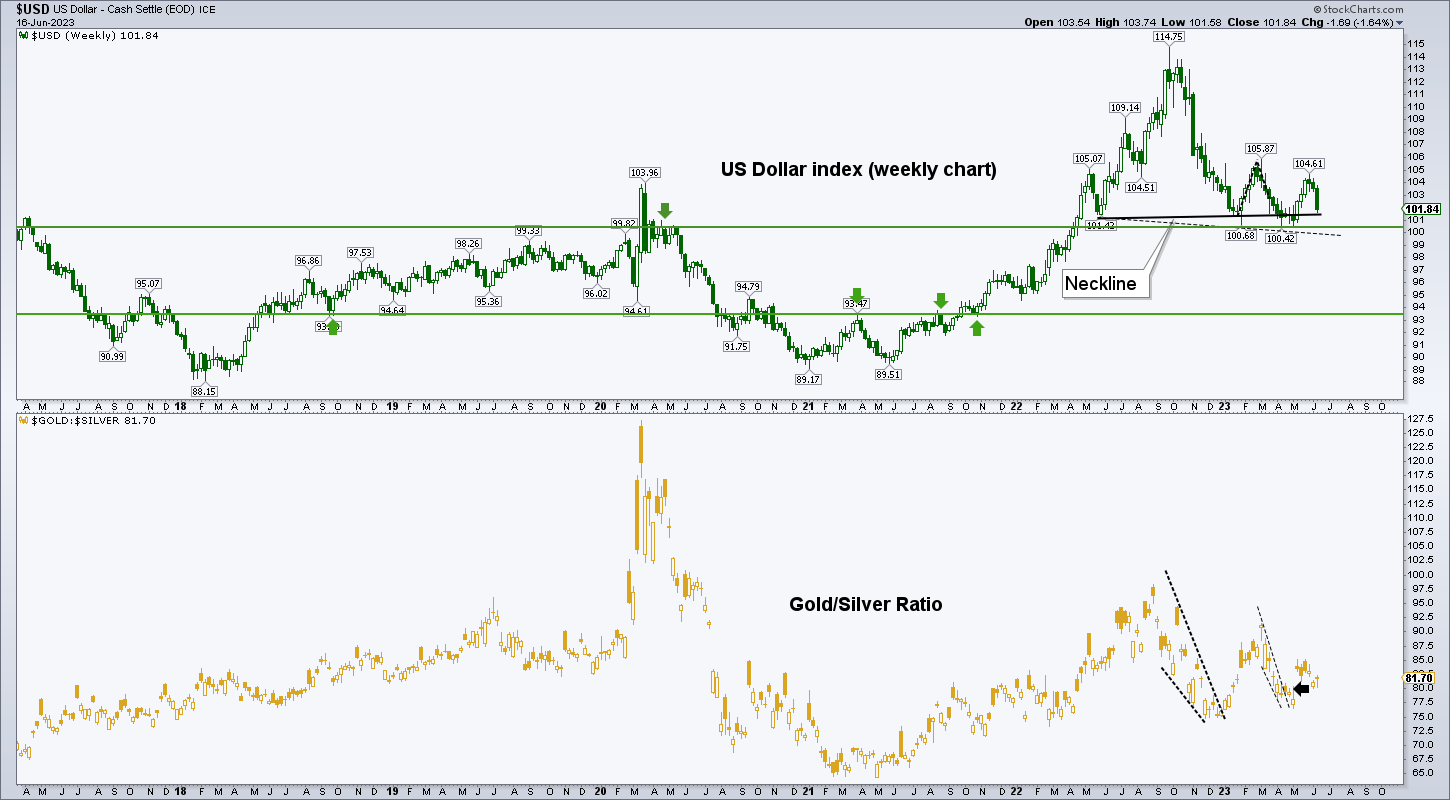

- USD holds the neckline (weekly chart below) and the support area it dropped back to last week and turns up amid liquidity stress when the stock market tops and rolls over, or…

- A new inflation trade coming sooner rather than later that would not be born of USD weakness at the hands of a dovish or even liquidity-panicked Fed, but instead, would come from fiscal policies (governments, US and global) as opposed to monetary policy (central banks).

Or it could come from both. Stealth QE in combination with governments borrowing and spending. For crying out loud, I cannot drive 2 miles without getting stuck in what seems like constant fiscally funded “roads and bridges” work going on (here in Massachusetts, at least). Now think about a coming end to the Russia/Ukraine war and governments’ ability to tax locally, spend and rebuild Ukraine under moral imperative. Might commodities not take up the bull under such a scenario. Yes, they might.

Still Goldilocks

Still Goldilocks, but open to a change. Remember, we were the first to call a Goldilocks backdrop that I know of, with Tech and Semi leading the charge, while most were still fully beared up. Now, I feel like I am running with dumb money by adding positions last week. And make no mistake, dumb money is on the market, big time. But might we be looking at another rotation within the markets?

What I call the Goldilocks stuff, Tech, Growth, etc. took much harder hits in 2022 than the broad (multi-sector) S&P 500, and the phase in place so far in 2023 has seen these areas play catch up. This chart shows that to still be the play. Semi is leading Tech and Tech is leading SPX. This has been the play for all of 2023 and it is still in force.

That said, as I look around the landscape of bombed out commodity/resources producers and prospectors, I cannot help thinking “to everything, there is a season”, and just maybe there is a wiseguy machine programmed to rotate into that season. Well, our job is to get there at the same time as the machines, if not shortly before.

Everybody Knows

Everybody now knows that the effects of the last inflation are fading, or at least the backward looking YoY comps are fading as the headlines broadcast the good news. Yet still we have the hawk posturing Fed. Tin foil hat affixed, does the Fed know full well that it is inflating out the back door while showing the public a nice, neat and buttoned down policy house through the front door? Is the liquidity that the Fed and government conspired to produce to keep the bank sector whole an aspect of ‘fire hose’ policy that is not so accurate in its specific targeting?

I realize that this sort of “stealth inflation” talk is the stuff of commodity bulls who really want you to find a reason, any reason to be perma-bullish on a “Commodity Super Cycle”. At this time I am potentially in transition to a new and unexpectedly regenerating inflation problem. But please note the word “potentially”. Our operating theme has been for Goldilocks to transition to a deflation scare and market liquidation.

Perhaps the best indicator for our purposes in the near-term is the US dollar, Uncle Buck, he who drags all that policy around like Marley’s chains. So we are actually still on the same 2023 plan. But as mentioned previously, if Unc breaks down we’re looking at potential inflation trades coming sooner rather than later.

USD’s rally never made it to the 38% Fib retrace and daily SMA 200 before turning down around the time of conclusion to the Debt Ceiling drama. As if to play ball, the Gold/Silver ratio (GSR) is also below its SMA 200. As we’ve (probably too closely) tracked that little ‘would-be’ short-term bullish pattern in silver we observe the GSR not indicating liquidity pressure in the least at this time. It is currently in line with the bearish USD.

The weekly USD chart has not broken down, however. I am going to be a stickler about this and not put my forward speculative brain ahead of my view to this point, which has been a) USD is in a long-term bull market (it is) and b) if/when it breaks down from key support (it hasn’t) then we can project a significant drop within the bull market to the 93.50 area. That would unleash quite a global inflation trade, or anti-USD trade or whatever you’d wish to call it.

There is no USD breakdown after a noisy week. There is only growing rationale for commodities, EM and other aspects of the anti-USD trades to go bullish.

Bottom Line

As SPX looks upward to the next target (4800 +/-), copper out-performs gold in the short-term (always was going to happen with a gold correction and/or an oversold bounce in copper), sounds of easing emanate from China’s central planning orifice (after the great ‘reopening’ pump never came to pass, as the economy began to slide), the headlines trumpeting tamed inflation, the Fed appearing in control with an extreme yield curve inversion (recessions are not indicated by the inversion but rather, the subsequent steepener) and a Goldilocks veneer on the surface, dumb money is in da house and it thinks it can make some coin now.

So it is entirely possible – if not probable – that the opening segments of this report are the types of forward speculation that a rampant bullish atmosphere would instigate. Meanwhile, SPX (weekly) is motoring toward the next target after taking out 4300 with authority…

…and frankly, the more I look at it the firmer I am that it is exactly as we’d speculated, a “last chance power drive” so to speak. An upside reaction to 2022’s incomplete bear market that could be a sentiment event for the ages.

Within this, commodities and emerging markets could just play some catch up (rotation) with stories like the one I’ve spun above about sources of liquidity and stealth inflation. But until USD breaks down for a deeper correction within its bull market and speaking personally, I don’t buy the big bull trade. Not yet. If the buck loses support it would be a long way down to 93.50 and could be a humdinger of a trade. But it has not broken down and therefore NFTRH is on the same plan we’ve been on all year long with an open mind, and specific indicators (USD/GSR) in place in order to alter the view.

Goldilocks is still in play and she will likely either morph deflationary as yield curves complete the inversion and turn up to steepening or she will revert inflationary, also with steepening yield curves. Deflation or inflation? They both happen with steepening yield curves (with the direction of nominal yields being the difference). One of those is likely after the sentiment event back to massively over-bullish terminates. Again speaking personally, I am not going to get caught leaning the wrong way into what would be two very different (like, opposite) backdrops.

So depending on the signaling, I’ll either press a bit further long or abort and the primary signal would be the US dollar (with assists from the Gold/Silver ratio and other gold ratios and market indicators), which has been bearish but has not yet lost support.

Precious Metals

So if the original plan (disinflation to deflation scare, post-bubble in equities and policy making) is maintained then our interest in gold stocks is maintained (I am always interested in gold because I don’t put price expectations on its insurance value). A post-bubble era really would be something quite different, with new rules and indicators to those rules.

But the opening segment in essence discussed new, more covert methods of bubble blowing. If they do re-liquefy cyclical, inflation-sensitive and risk ‘on’ markets that would go against the best and over the last many decades all too rare fundamentals for gold and especially gold stocks. With a tanking USD I’d have little doubt that the inflation bugs would get ‘er going again, full pom pom mode…

…but for a real and longer-term bull market in gold stocks we’d want to see Goldilocks morph deflationary, broad cyclical markets liquidate and then buy quality gold miners as gold zooms upward in relation to stocks, currencies and commodities (esp. mining cost input commodities and materials).

Here is the daily chart updating the situation. To avoid a breakdown of the important Gold/SPX ratio gold should gather itself now and start to rally or SPX should top and drop. A failure to do so would not necessarily break the play, but it sure would not help in the short run and would likely extend the gold miner correction. Gold/Global should not make a lower low. Gold/Commodities are on a still normal uptrend pullback. Gold/Copper is more severe, but Doctor Copper is the poster boy for global ‘risk on’ cyclical party time, which the dumb money graph above shows is in full effect.

The gold price (daily chart) is lurking below the SMA 50 in a potential little bounce pattern, which would only imply a test of the previous highs if it were to manifest. RSI and MACD are ready for such a move if it were to play out. But gold is still in a normal correction of an ongoing uptrend. If no short-term bounce comes about the best corrective target is the SMA 200 (1851 and rising) with allowance to the 1820s, which would still not break the uptrend from Q4, 2022.

The big picture monthly chart view continues to be bullish and has been bullish since gold took out the “gateway” in 2019 and then made its new (Cup) high in 2020. The resultant grinding of a very volatile and now 3 year old handle shows a monetary value asset lurking in wait while the macro party plays out. It is doing this without putting the time/price expectations on it that you or I or more likely, most other casino patrons may put on it.

The measurement of the Cup implies an eventual target of around 3050. If it comes to be, it will have been worth waiting for because not only would it spring a big rally/bull in the miners, but it would be doing what it always does, which is to provide real value, in this case, quite possibly with other aspects of the financial world under duress.

Gold purist sermon over, let’s move on to gold’s wild little bro. Silver (daily) continues to lurk below the resistance at the SMA 50 and it continues to sport the little pattern we’ve been tracking. Personally, I’d still like to see silver make a real hard test of the previous low at or just below 21, but markets being markets, there is the potential for the bounce pattern to play out first for a test of the previous high (much like gold’s daily chart situation).

Here is the log scale monthly chart of silver that I like to peek at once in a while. The fork is a novelty, but the chart itself is constructive. Since the bear market bottom at the hysterical COVID low in 2020 an uptrend is in place. We’d want to see silver hold above the March low (above) and that is the expectation. But if things were to get off the hook, like in a deflationary episode, silver could drop to 18 and not be broken on the big picture.

The daily GDX chart finds us where we have been. That is, managing an ongoing correction. But as with gold and silver, gold stocks have the potential for a bounce. The volume profile, the states of RSI and MACD and the little flag structure that has formed in June would all be supportive of a bounce, perhaps to test the resistance at 33 that coincides with the SMA 50.

As with silver, the preferred ultimate corrective target is lower, however. That is for a quick spike through the now uptrending SMA 200 and a gap fill below 28. Or at least a test of the SMA 200. I am not now and never have been predicting that because people who make predictions are clowns, in my opinion. Carnival barkers. A market intent on really going bullish could abbreviate its correction at any time. But right now the favored view is for an ultimate corrective low and a tick below 28, with the potential for a solid bounce in the interim.

With GDX going nowhere last week HUI (weekly) is obviously little changed as well. The way the gold stock sector usually rolls is that its corrections end hard, not soft. If the interim bounce scenario plays out Huey will hold the 240 area support and like rise toward 260 (a daily chart’s SMA 200 is at 258) and resistance. If that were only ‘interim’, the best low/buy area would be 220 to 230.

Bottom Line

It’s a normal correction with the potential for a bounce amid macro party season. Such a bounce could happen for the ‘wrong’ reasons of renewed inflation trades or just the general party atmosphere as Wayne and Garth party on. But the best targets for the metals and miners are and have been to make higher lows above the March lows. If wrong about that and if a bounce does occur then taking out the 50 day averages on the upside would be the first step in calling the correction over. The final step, using GDX as an example, would be to take out the May high (36.26). As for the big picture, the target of HUI 500 (+/-) is still in effect.

Global Markets (weekly charts)

Everybody is as we left them last week; World: trending up in an ongoing rally, same with Europe, while Great Britain, Canada and Australia under-perform.

Japan is going a little parabolic, as if to finally prove NFTRH correct years after the projection (and more recently after you letter writer had been miserly, looking for a better buy at 24000). Ah, markets. The combo of weak USD and bearish Yen probably very much in play here.

Hong Kong/Asia are still in bounce mode, EM put in another week rising from the trendline breakout, India is flying around near blue sky and bullish.

Importantly for this week’s discussion about commodities and inflation trades, Canada’s TSX-V continues to creep the support floor. A turn up in the index would likely coincide with an inflation trade involving commodities/resources.

I took the profit on the Brazil ETF, but BVSP remains on a firm rally. Argentina… ha ha ha. Mexico is flat out bullish. Africa bounced to ding initial resistance. FM ETF is bouncing from unspectacular looking support.

Commodities

After months of summarizing a bearish situation in commodities, and thus the need to deemphasize them, let’s revert to the old days when we used to review charts like these, showing multiple commodity indexes and some related commodity prospectors and producers (daily charts).

CRB index bounced hard last week within its major daily downtrend, right to the SMA 200. So far, it has proven nothing but a bounce. Taking out the April high would prove more.

The same goes for Crude Oil, which barely bounced at all in its downtrend. Gas has been blown up from the highs but we’ve been managing the potential of a base (caveat: the seasonal average declines into September). I added NOG and AR as plays on Energy.

Industrial Metals are trending down and bouncing a bit. They are following their leader, copper, which has bounced to $3.89/lb. and crept above its SMA 50 and SMA 200. That will be important to hold if the rally is to continue.

The Ag index is trending down and bearish, but also bounced hard while the ETF (DBA) broke hard upward from the base we’ve been noting. While I have not taken the time to look into it in detail, we can speculate that the heretofore downtrending Wheat has been driving GKX while the likes of Sugar and more recently Soybeans and Corn have been driving the ETF. Either way, something went on there last week and it bears watching. I added fert play NTR and also have MOS on watch.

The Uranium patch has maintained the constructive (bullish for CCJ) look we’ve been noting lately. This chart includes the u3o8 fund and my personal four main watch list items (I hold CCJ and UUUU). The situation is technically constructive rather than bullish because there is no established uptrend yet, other than CCJ. But with a positive view of Uranium in the future it’s a sector I don’t want to risk being out of when there is even a hint that it could go.

Here is a look at more of the outlier/specialty commodities that I keep a close eye on for reasons of their strategic use in electronics, EV/clean energy and other progressive areas. You could almost think of the dirty likes of crude oil as the old fashioned Dow Jones of the commodity complex and these items as the sexy Nasdaq growth stuff. At least in the minds of many investors.

REMX is constructive to attempt to end its downtrend (still very much in force) and REE producer MP (I added it) is purely trending down. The thing about MP would theoretically be a revaluation (it’s already richly valued on a global scale) if much more tension between the US and China come about, let alone sabre rattling. Talk about strategic, MP’s Mountain Pass is a key US producer of REE. Someday that should matter. As with Uranium, it’s a position I don’t want to be out of when that time comes. So I poke it periodically.

Former holds LTHM and ALB the premier Lithium plays, but I researched a bit and added LAC instead. If the situation firms, I might buy LTHM back as well. The trends are still down, however, with LTHM attempting to do something about that.

Finally, future Nickel producer TLO.TO/TLOFF is still on watch, especially now that battery metal Nickel showed a pulse last week as it bounced nearly 6% off the lows. Both miner and metal are firmly trending down, however.

Bottom Line

As for a conclusion to the commodity segment, the opening segments pretty much said it all. If the USD holds support and rallies most of this stuff will go back under pressure. If USD fails and actually targets 93.50, an epic and unexpected inflation trade could generate in the interim.

Portfolio

Savings balanced by gold.

Trading Account: No positions

Roth IRA (non-taxable, no contributions)

IRA is 81% cash and equivalents, all paying healthy income. Hence, a great and also rewarding risk management tool, as opposed to the more risky shorting. Holdings represent a mix of Goldilocks type stuff, some global (Japan, India and China), commodity/resource related and gold stocks.

The portfolio is very interested in the USD question that ran through this report. If it turns up along with the Gold/Silver ratio, cash will very likely be raised. If it breaks down and the GSR weakens, I’ll press further into the play. For the moment the positioning is ready for either situation. The US stock market is postured to blow off if it is not already doing so. Dumb money is frothing at the mouth. It’s unhealthy. It’s also bullish. For another day, week or month. But the risk profile is bad.

Cash & income-paying Equivalents are at levels that are right for me and my real-world situation. Your situation is different. Cash will be adjusted as needed.

Refer to the Trade Log under the NFTRH Premium menu at nftrh.com for trade info, if interested (not that you necessarily should be). Also, you can follow at Twitter @NFTRHgt for notice of updates.

NFTRH is not to be distributed to third parties without prior written consent

Notes From the Rabbit Hole (NFTRH) is a weekly market report in which we provide analysis on financial markets. We make every effort to provide accurate and high quality content, but this analysis ultimately represents our opinions and these opinions are provided without warranty or guarantee of any kind. See full terms & conditions of service under the ‘About’ heading in the main menu.