The Baltic Dry Index has dropped hard

I most often use the MSfM as a contrary indicator as you probably know. But this morning CNBC provided me with a valuable insight on an indicator that I have neglected to look at for a good long while, the Baltic Dry Index, or BDI.

Consumer prices jumped in October, but one indicator says inflation might be peaking

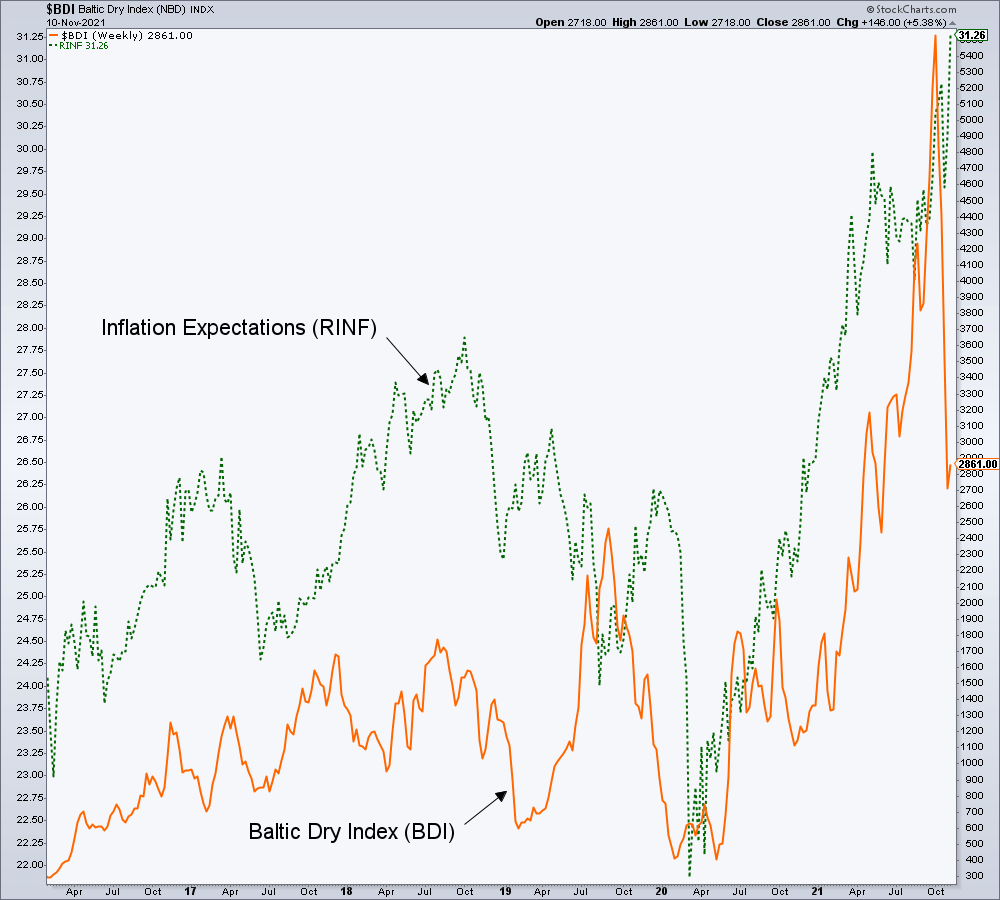

I did not take the article’s word for it. I decided instead to create a chart correlating inflation expectations with the BDI. Here is the linear scale view of a weekly chart.

Sure enough, the two have correlated well since the deflationary hysteria ended in early 2020. BDI is diverging RINF drastically of late.

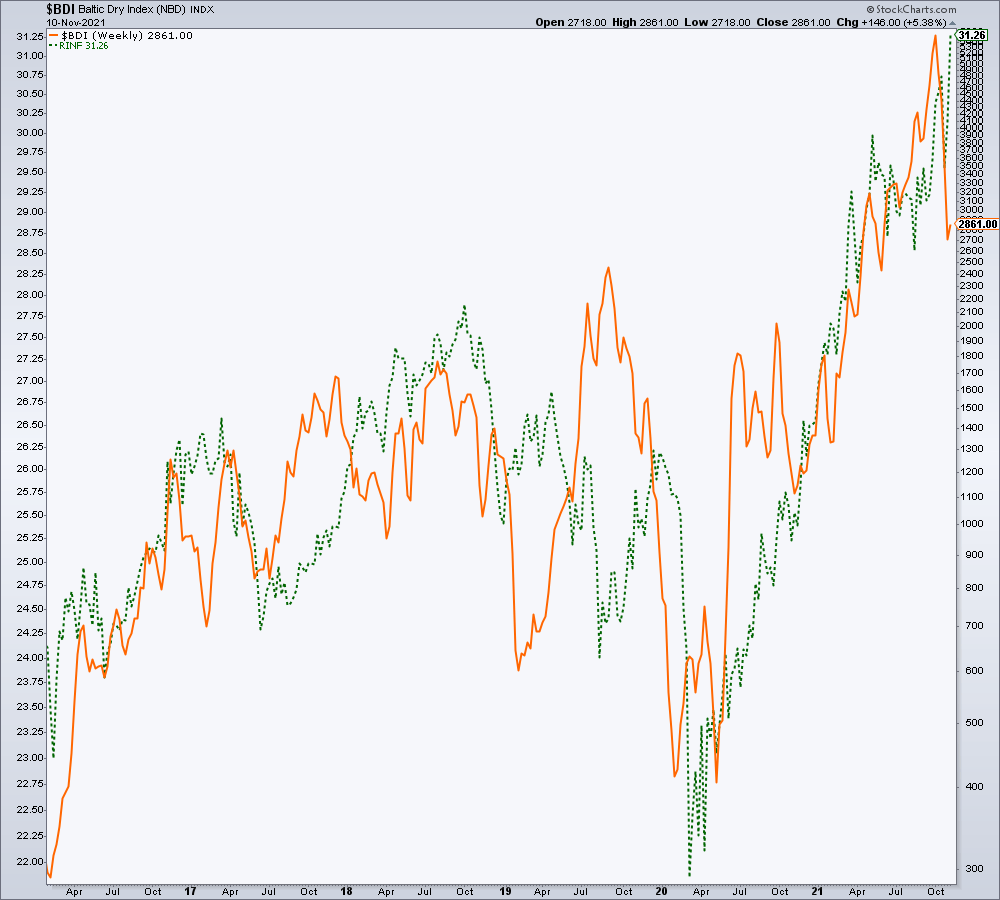

Shifting to a log scale version of the chart we find an even tighter looking correlation over time along with the recent divergence.

So who is real and who is Memorex when it comes to the BDI and inflation expectations? As a reminder, the BDI is not actually an index of anything. It is a continually updating view of global shipping costs.

As a companion, let’s look at another indicator I’ve used extensively in the past and need to be paying more attention to now. The yield curve is abandoning its steepener in favor of a new flattening. Now, two things can come of this…

- A continued flattening and blessed Goldilocks economy favoring Tech and domestic business, or…

- A grind in advance of a new steepener, bearing in mind that a steepening curve can be inflationary (e.g. 2020-2021) or deflationary (e.g. Q4 2008). And so, a new steepening could be inflationary or deflationary, and given the current interruption and 2008 (which steepened initially under inflation, ground around for a while and resolved with a new deflationary steepener) as a model, I would not bet on an inflationary resolution.

Interesting stuff folks. The yield curve is no longer on an inflationary steepener and I wonder how on point the BDI may be at predicting. We’ll find out soon enough, but the inflation headlines sure are deafening out there, eh?

Side Note: Goldilocks would not favor gold or gold mining. But a deflationary steepener would eventually, perhaps after running the herds of inflationist gold bugs over a cliff (again).

For “best of breed” top down analysis of all major markets, subscribe to NFTRH Premium, which includes an in-depth weekly market report, detailed market updates and NFTRH+ dynamic updates and chart/trade setup ideas. Subscribe by PayPal or credit card using a button on the right sidebar (if using a mobile device you may need to scroll down). Keep up to date with actionable public content at NFTRH.com by using the email form on the right sidebar. Follow via Twitter @NFTRHgt.