Volatility. It is what we expected and it is what we have with Tuesday’s big down and upward reversal, down hard again yesterday and today very green in pre-market. This volatility applies to most assets markets including the precious metals. It is the nature of the beast during a news-rich summer, with many operators on vacation or semi-vacation (with some players not able to resist peeking?).

The S&P 500 has satisfied the 1st level of anticipated correction by weekly chart. It does not look like much, does it?

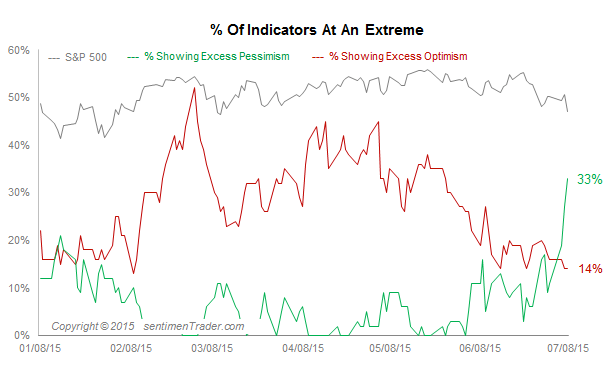

But it has been enough to launch pessimism to its highest level in many months. One definition of volatility: liable to display rapid changes of emotion. This is perfect for the whipsaw up and down backdrop going on by daily charts.

SPX daily shows that story clearly, with large swings up and down with a downward bias (series of lower highs and lower lows) since topping in mid-May.

Given the fading participation we noted last week (by Bullish % indexes) and the daily down trends (weekly remains up), the market is now bearish until it proves bullish on a short-term basis. Long-term it remains in bullish trends until it proves otherwise. In the meantime, welcome to volatile Whipsaw City.

Commodities will bounce and drop with the rest of the global asset world. China seems to be playing a role here. True commodity bulls may be looking for a triple bottom here. Personally, I am looking to own no commodities because I don’t like them at all until an inflation story can get going. While there have been a few glimmers in the last few months, it is not going.

Globally, the Euro STOXX 50 is bouncing as well. It has not registered the preferred 3200, but got into the 3200’s. I am still waiting on this one, personally. But if you believe the hysteria over Greece is an opportunity, you may have been slowly initiating as 3200 to 3400 has been the range for that.

We noted 42 to 43 as the initial support per Tuesday’s NFTRH+ update on FXI.

“FXI is getting to a point however, where it can bounce (1st support). It is also getting to a point where those who are bulls on China for long-term investment might take initial positions or add an increment to existing ones.

That said, for the purposes of this update, we’ll call it a ‘look forward’ like yesterday’s update on Europe, and use the stingy and conservative lower level as a buy.”

Here is the weekly chart from that update showing a drop right into the support zone and very close to the buy target of 38. This has been outright terror, and a buy around this level could provide quite a trade (stop loss is a loss of 36). For my part, I bought EWH (Hong Kong) instead. I’d like to get FXI but would rather not chase a strong bounce.

China 25 vs. SPX made a bull signal earlier in the year. China bulls can see this as an opportunity (again, I should be clear that I personally am not what you could call a China bull; not in the least) with the weekly moving average signal still on and a hard test of the lows. The ‘stop loss’ on this thinking would be new lows in the ratio on a weekly close.

As for precious metals, let’s subject them to the indicators since any serious bull stance will need to be backed by a stance that sees changes on the macro.

Beginning with yield spreads, the 10yr/2yr and 10yr minus 2yr spreads are in up trends for daily and weekly time frames. The bottom panel is the AROON trend for the weekly. This indicates building pressure on the financial system.

Gold and the Banks, for perspective. We are allowing BKX to drop to around 73, while still being intact for further upside. Below that, and the Pigs will have likely failed. A strong banking sector is not what gold wants to see, generally speaking.

Silver vs. Gold, which we noted to be THE decider on whether or not there is going to be an inflation-fueled bullish asset party, instead broke down this week. Silver is up vs. gold in pre-market. Volatility and Whipsaws anyone?

Flipping it over, the Gold-Silver ratio is breaking out from the bullish flag this week. Again, subject to this morning’s volatility. We are talking weekly closes with these charts, so the breakouts on each (down and up) are not real yet.

Palladium vs. Gold is broken down. This made a positive economic signal in Q1 2013, well ahead of the general realization that the economy was improving. Now it is scouting out ahead for a downturn.

Gold vs. Commodities is breaking up from a weekly bull flag consolidation, similar to Gold vs. Silver. Again, let’s see how the week ends, but these are constructive for a long-term gold sector bullish stance on the big picture, and if the breakout vs. commodities (especially crude oil, energy and materials) holds up, the sector’s fundamentals would be indicated to be taking another leg higher.

Now for the hold outs, Gold vs. Stock Markets.

Gold-SPX and Gold-Europe are still nowhere.

If the bounces in stock markets are just that, bounces, and gold vs. stocks joins other indicators in painting this as a buying opportunity, then the over sold nature of GDXJ and GDX would be THE opportunity to take positions. If… I don’t like that the precious metals are bouncing this morning as part of global asset market relief.

HUI-Gold ratio is very bearish, but here we will temper this by recalling the big monthly view, which shows that this could be a bottoming area of significance.

Here is the monthly. It could break down, but it is also at a point where we can watch gold stock performance vs. gold to see if we can gather positive divergences.

I want to remind you that there is still no technical reason to favor gold stocks over regular stocks, although the play is setting up nicely.

Finally, monthly HUI has dropped to a point where a bounce is very logical.

So let’s call the sector likely to bounce from this over sold condition (daily GDXJ and GDX above) and nothing more until the right signals and milestones come in.

For years now during the bear market, we have noted that real investors can wait for technical indications and buy higher in order to have more surety. If you miss the 1st 10% or 20% of a new bull market it will not matter 2 years down the road. We started talking like that 200 to 300 points ago on the HUI.

So keep bounces vs. new bull markets in perspective. That said, given what is happening in certain macro indicators, I believe we are on our way to a cyclical bull market in the gold stock sector (quality items only please!). Patience is required.