Summary

US Stock Market: Bullish and at high risk. Internal rotations in play.

US Market Sentiment: Extremely over-bullish. Not a timer, but a condition for a market top.

Market Indicators: An ongoing mix of indications stating two things: 1) a sedate backdrop with seemingly not a care in the world and by extension, 2) high risk to broad stock markets, but especially in the US. [unchanged]

Global Markets: Still bullish on balance. [unchanged, this week we note trends vs. US S&P 500]

Precious Metals (Last week): Rally continued in the miners after the post-FOMC disturbance and support hold. Gold is bullish on all time frames, as it has been for much of the last few years. Silver… ah silver. It don’t come easy. But it do come (I think). Please see segment for much more detail of the sector.

Commodities: Commodities may be ending a long downward consolidation. Items to watch closely are the Silver/Gold ratio (want to see it rise), USD (want to see it drop) and TSX-V (want to see it hold its rally parameters). See segment for more. [unchanged]

Currencies: USD now looks to resistance at 105 as the proving ground. Make and hold a higher high there and it reestablishes the uptrend from December. Fail there and Wayne, Garth and the global macro party on.

The Bull Expands

One of our main themes has been that insofar as the bull would continue, markets would rotate internally to include items like commodities, commodity/resource related equities, emerging markets, laggard cyclical sectors (Materials, Industrials, Banks/Financials, Energy, etc.) and in their incomplete but transitional fundamental suit, precious metals as well.

On Thursday all of these items rallied while US Goldilocks leaders Tech and Semi lagged. It was a snapshot of what could happen if the US dollar aborts its rally for a hard correction within its larger bull market.

USD (daily chart) closed the week firm after negating the bear flag scenario. However, it remains below the key resistance level of 105, which would represent a higher high and thus, a continuation of the rally from the December low, if exceeded. 105 is now the line in the sand and from the looks of certain sectors last week, the machines appear to think 105 will hold as resistance.

While the trends have been up for several cyclical US market segments, they have lagged the broad SPX and lagged Tech and Semi by even more. But they are moderately trending up and could represent buying opportunities. I already hold Materials (XLB), sold Energy (XLE) but hold AR and have CVX on watch, and am considering the Banks (KBE and/or KRE). This while maintaining a few positions in Cloud/SaaS/Security type stocks for balance as the macro shows it cards.

As an example, here is the daily chart picture of Banks/SPX, KBE/SPY. It was a year ago that the government and Fed got together to sanitize the banking sector meltdown with a friendly combo of fiscal and back-door monetary policy. *

* Begging the question, did the Yellen Treasury and the Powell Fed get comfortable coordinating with each other during this event, possibly rolling out another coordinated effort for the next crisis (that being the potential of a Trump presidency)? I have adopted that tin foil hat view for this oh so unique election year.

Here is the chart pattern of nominal KBE. That is a bullish looking pattern that has held the now uptrending SMA 50 as the SMA 200 also turns up. RSI and MACD look nice as well.

So, with respect to the potential for internal market rotations, let’s look at more sectors as adjusted by SPX/SPY beginning with the two leadership sectors.

Tech is still in potential rollover from internal market leadership.

Semiconductors are correcting what is still firm leadership. This is thus far a healthy pullback.

XLE (Energy)/SPY is counter-trend bouncing within a downtrend.

Healthcare (XLV) dinged a new all-time high on Friday, but trends firmly down in relation to SPX/SPY and as a market internal indicator, risk is still ‘on’ and this relatively defensive sector has given no bear market signal yet.

Let’s look at one unique commodity sector vs. SPY. The ratio had been bullish, spiking up from a consolidation within an uptrend and then getting reversed hard. The major daily trend (SMA 200) has turned up and that is being tested now. It should hold if a relative buying opportunity is to be interpreted for Uranium stocks.

Copper miners are on the internal rotation theme as the COPX/SPY ratio has popped to the downtrending SMA 200. Taking that out and ticking new highs would go a long way toward signaling a firm internal market rotation to include the cyclicals, if not favor them.

A look at that most ignominious of sectors, the gold miners. GDX/SPY is trending down and as they have pretty much gone as the ‘inflation trades’ have gone, the picture is not unlike the copper miners above.

The macro signal is pro-cyclical and pro-risk as the gold miners are going nowhere in relation to copper miners.

Ah, but the Gold/Copper ratio is doing this. The trend is and has been up, even after the China smelter production cutback hype spiked copper upward in early March.

This picture (GDX/COPX trending down while Au/Cu trends up) is one of many seemingly dysfunctional signals that the market has presented over the last couple of years, not coincidentally in my opinion, since the 30yr Treasury Yield Continuum broke its downtrend.

My view is, and since that trend break has been, that it is a new macro and certain internal signals are adjusting to that. Therefore we must adjust to certain new realities and try to avoid automatic thinking as bred by the previous trend from the 1980s to 2022. That is not to say that GDX/COPX disparity from Au/Cu will remain in place, but using that example, it is to say that some things just don’t make sense in a broken market as you can almost hear the machines grinding away (leading, lagging, speculating, retrenching and basically reacting to every bit of news that hits the tape), trying to figure it all out.

Global Relative to the US

Globally, Japan is a lonely out-performer to the US. Of course, Japan earned the right to spring to global leadership after the decades long “lost years” of deflationary pressure. Another major trend somehow broken by the implications of the picture directly above and its fellow global bond market signalers? I cannot quantify the macro internal specifics, but I sure can respect them.

Europe is trending down in relation to the US. That applies at least as long as the downtrending SMA 200 holds.

Global star India does not look so good in relation to SPY/SPX.

China (large caps)/SPY is purely downtrending and not yet actionable, although I personally continue to watch for the potential of a global macro rotation.

AAXJ/SPY shows Asia (ex-Japan) in even worse relative shape. Note that EEM/SPY is very similar and we need not show the chart. It looks like this one. I hold AAXJ for the prospect of a global rotation and for its bullish biased (but not yet bullish) daily chart.

ILF/SPY shows that the Lat Am 40 have tanked in relation to SPY.

However, nominal ILF still looks constructive and has the look of other items that could get internal market rotations from headline US stocks. The same dynamic noted within US sector can happen in certain global markets. This is a bullish market that, unlike the US indexes, is not overdone. Rotation?

Bottom Line to All of the Above

We have been on watch for the potential of markets to rotate to include US sectors and global markets that are more cyclical and anti-USD in flavor, commodity/resource related equities, and even counter-cyclical gold stocks. The trends are generally down vs. the mighty broad US market and its mighty fiscally stimulating government and its mighty back door stimulating Federal Reserve.

US Market Sentiment

- Smart/Dumb money indicators backed off just a bit, but continue to show extremes in over-bullish sentiment.

- Investors Intelligence continue to show the extreme over-bullish state of Newsletters at 3.99 Bull/Bear ratio.

- NAAIM made a big spike to get back to extremely over-bullish, hitting a leveraged 103.9% vs. the previous week’s over-bullish reading of 93.2%.

- AAII eased a bit but is still at a moderately over-bullish Bull/Bear ratio of 2.23 (for perspective, an extreme for AAII is 2.5 or higher and an extreme over bearish reading is .5 or lower).

Market sentiment continues to be over-bullish, indicative of very high risk, but a poor timer. It is a condition to a market top, not a timer of one. The condition is over-bullish. Here is the pictorial view of Investors Intelligence, which is now in a condition for a market top. One day it will matter.

Precious Metals

Let’s not over complicate it. Gold has broken out to new all-time highs. Target #1 is 2450 and target #2 is 3000+.

However, the picture is duller when viewed through the lens of headline US indexes like SPX. This has been an ongoing negative for the gold mining sector, which has for nearly 3 years now been correcting the 2020 excess. Gold is bullish, but its ratio to SPX still is not. When it does flip bullish that should be a strong tailwind for the gold miners. I expect it likely to happen post-election, if not sooner in a pre-election divergence by gold. This could happen if the stock market falls apart, or gold could start to out-perform a still bull trending US stock market despite (or maybe even because of) the combo monetary and fiscal policy supporting it.

Yet, along with the still cautionary chart above, the ratio of gold to a gauge of inflation expectations was positively diverging the miners at the end of February, as we noted at the time. Then the miners (HUI) rammed upward to start getting back in line with the ratio.

The indicator above is antithetical to most analyses of gold and especially gold stocks, which focus on inflation as if inflation protection is gold’s main utility (it is not) or as if the miners are ever good fundamental vehicles during a cyclical inflation phase (they are not, with the exception of a gold stock bubble phase like 2004-2008).

Here is the daily chart macro view of important gold ratios showing an interesting breakout vs. global stocks, a bounce to important resistance vs. US stocks, ‘steady as she goes trends vs. commodities and copper, and a consolidation vs. mining cost driver, oil. As has been the case, it is a picture of an incomplete macro slowly grinding positive for the gold sector. If the break upward vs. global stocks means something, that positive grind could gain momentum.

Retreating back to the daily chart of GDX we find the miners on a strong rally leaving gaps aplenty behind. The lower gaps do not need to be an immediate concern because they represented a launch from an important low that may one day prove to have been a trend breaker (from down to up).

Resistance at 32.65 represents a slight higher high just as the February 28 low represented a slight higher low. GDX could tick a higher high, correct from resistance, test support around 29.60 and/or the 50 and 200 day moving averages, and then proceed bullish again. Alternatively, it could reduce the overbought reading by pulling back to fill Thursday’s gap up before attacking resistance.

Expanding the view we find our old friend, the gap at 39.49. That was the potential objective of the rally before the final plunge in January-February took it off the table. Well, it is back on the table, but there is much work to do, beginning with the noted resistance in the 32s.

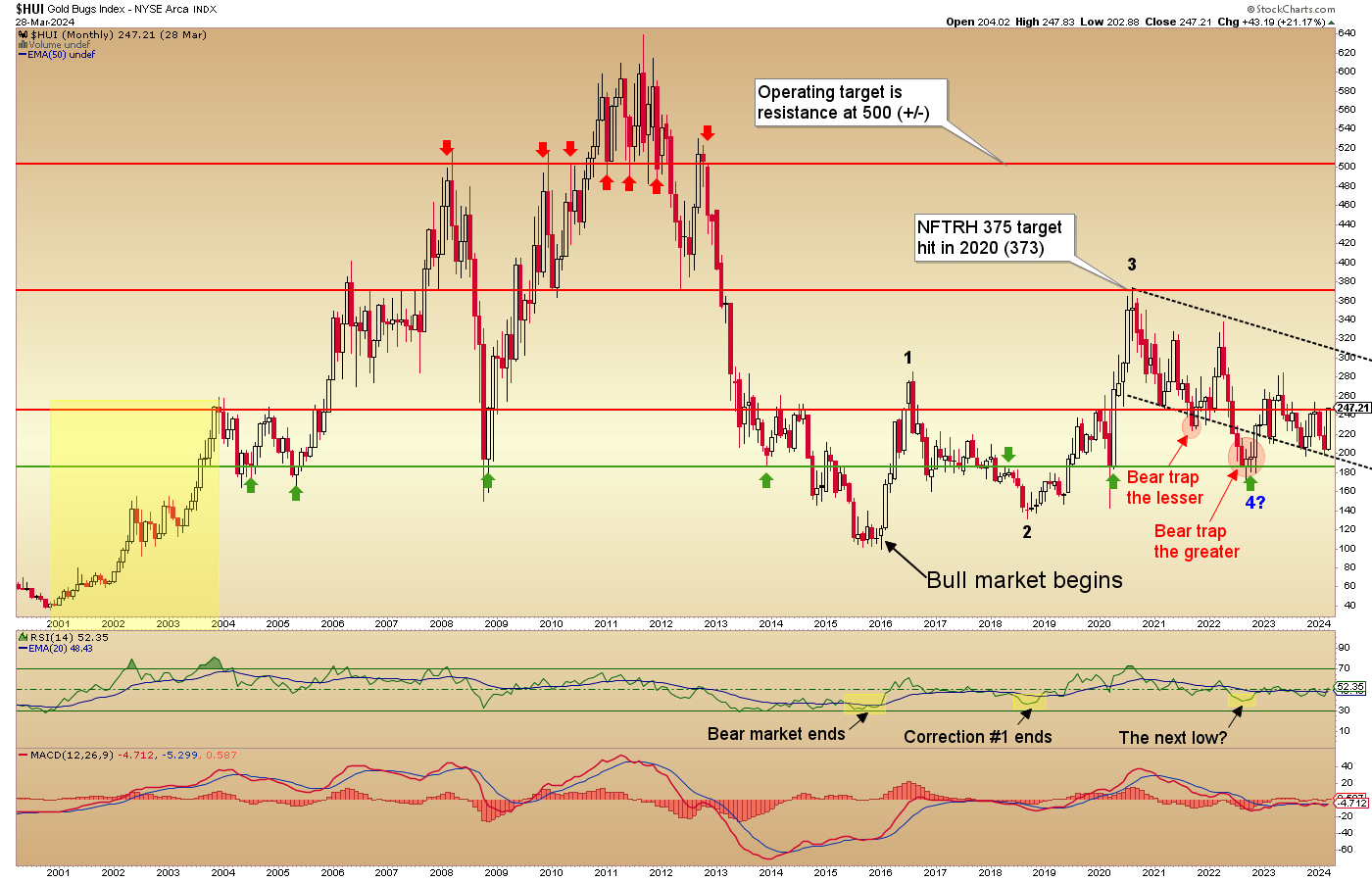

Reverting to HUI for the larger view, we find Huey bumping its head right back at the resistance level that has held it in check since May, 2023. Considering that the macro is not yet fully set to the preferred fundamentals (with stocks still bubbling along and the economy okay) the goal for the rally is the top of the downtrend channel at around 300. That would come close to filling the GDX gap near 40, if not fill it.

Extrapolating further, we might speculate that the gold miners would put on this tradable rally, reverse at the channel top and correct as the broad stock market ends its bull. Then, when the economy is clearly in a counter-cycle (the bust side of ongoing boom/bust cycles) will the miners rally for real in a new bull market that would target a minimum of 500 and possibly much higher.

But that is all forward speculation at this point. It is important to realize that it is okay to have preferred plans like this, but it is not okay to pretend to be a guru and make predictions. That stuff leads to heartache much more often than not. I have illustrated my preferred plan and I am going to have a lot of patience as it either plays out over the next 1-2 years or requires alteration.

With Easter Sunday being the last day of the month, Gold has closed March at all time highs. It can now pull back to fill a gap and test the 2150 area, pull back deeper to test clear support coinciding with the SMA 50 (2089) or just keep on going with the whole world seeing the breakout. But it is important to realize that whatever happens on the short-term, gold is technically indicated to be very bullish after having been constructive to bullish in one form or another, depending on time frames, since taking out the bull gateway of 1378 in 2019.

Indeed, it deserves another look at the big picture monthly chart. Pattern Senior (Cup & Handle) targets 3000. Pattern Junior (shaded yellow) targets 2450. If stocks (SPX) are in a mature bull market, gold is just getting started in a new leg of its post-2018 bull market.

Silver’s weekly chart pattern continues to tantalize men who stare at the chart. In my case stare at the chart and then get skittish and mentally whipsawed on another failed breakout. But George and Ringo advise how not easy it don’t come. They worked so long and hard along with mates Paul and John before the Beatles became THE BEATLES.

Silver has a bullish look, very appealing weekly RSI and MACD, and well, it’s time. The pattern was built of 3+ years of corrective consolidation. It don’t come easy, but it do come I think.

Commodities

- CRB/GNX commodity indexes are still postured to break the long consolidation from Q1, 2022.

- WTI and BRENT Crude Oil are not surprisingly in similar postures, driving the indexes.

- NatGas is seasonally positive well into June, with a dip into July before a strong remainder of the year. Of course, the seasonal is not playing out thus far. But with Gas at very long-term support going back to the 1990s I think it is worth a shot (my vehicle is AR, which has rallied hard as if it thinks Gas will also rally).

- Copper is bull biased even after dropping to correct the ‘China smelter’ hype. The copper price looks to me like a bull flag at support in the 3.93 area. Fellow industrial metals (GYX) appear to be in a basing pattern that could precede a rally of some kind. The associated miners think that copper and its fellows will rally. Copper miners are near the highs despite copper’s recent decline. I am bag holding a small position in Ni/Cu prospect TLOFF (TLO.TO) with little concern. It is the kind of thing that could wake up one day and say ‘see ya!’.

- Uranium has been the leader for the commodity sector I assume due to its unique global supply/demand fundamentals. Using URNM as an example, the sector has declined to test support at the 2021-2022 highs at 45 and thus far held above that level. Current price is 49.29. It is possible that the sector is preparing for a new up-leg, but follow through is needed as other areas gain bids and this leader remains in correction. We had an NFTRH+ update on Thursday highlighting an interesting (and technically bullish) chart for a leader, NXE, which I took shot with and added.

- Uranium stock UUUU has an REE component to it and I’m holding it. Watch item for REE is MP, which I’ve poked several times and will likely do so again. The original analysis a few months ago illustrated a stock that had corrected far more severely since 2020 than the prices of the Rare Earth Elements that it produces. Palladium and Platinum are currently of little interest because I cannot get a great read on their global supply/demand fundamentals. But they would be likely to rally if a broader commodity/resources rally gains some steam. Lithium stocks (ALB & ALTM) are super volatile (up and down) within a terrible bear phase. I may consider them at some point, but it’s low priority at this time.

- The Ags see the ETF (DBA) making a new high for the cycle and the index (GKX) on a rally within its downtrend. I don’t care for the actual Ag commodities but do keep MOS and NTR on watch and each of these are making moderate moves off the lows.

The Canadian TSX-V is often included in the Commodities segment because it represents the speculative end of the commodity/resources stock realm. When da ‘V’ is rallying, it indicates a tailwind for the wider commodity/resources patch.

As you can see, the black arrow shows where the index held a critical higher low before ramming upward. Now it is at obvious resistance at the downtrending 200 day moving average. It is proving time with respect to the potential for the bull trades to continue fanning out from Semi and Tech to a significantly wider market view.

Portfolio

Funds are balanced by gold (long-term risk management & monetary stability).

‘Savings’ account holds AE.V (hat tip to geologist Michael), thus far without new opportunities to increase the position on significant pullbacks. A little NEM was also sprinkled into the account. This is because at some point I’d want to be holding the gold stock sector for a significant bull move. So I poke a bit.

Roth IRA (non-taxable, no contributions)

Cash is around 76%. The portfolio reflects the prospect of the bull fanning out to include other areas (aside from big Tech and Semi) as has been our recent theme to watch for.

For gold stock holdings, I tip my hat to Joe (WDOFF), Rich (OGNRF), Fred (CXBMF) and myself (AMXEF, AEM, KGC & NGD). :-)

The portfolio continues to carry a few Tech related items in the SaaS/Cloud/Security area while expanding the diversity to Uranium, Gas, Real Estate, Biotech, a couple Semis on the sector’s moderate pullback and most recently, Cannabis. That last one will be watched closely, because my two positions followed some hype coming out of government about rescheduling pot from a controlled substance in class with opioids to something more in class with alcohol. We shall see on that. I am going by the charts, which are changing daily trends from down to up.

Also, Asia and US Materials have been held for a while now, on the prospect of the play fanning out from Tech to other sectors/markets.

From a macro view, this is a high risk game. But the market appears at this time to be playing to our theme of an election year “last chance power drive” toward or into the US presidential election. And again, that is not some guy with only a tin foil hat speaking. It is a guy with a tin hat AND actual facts like the Federal government spending deeper into debt for economic stimulus and the Federal Reserve remaining tight on the Funds rate, but not at all tight in its internal bond monetization operations.

A final thought is that with the Funds rate unlikely to rise again on this cycle, I am considering adding 1-3yr Treasury bond fund SHY, joining the actual Treasury note already held. This would be looking forward to when the Fed starts cutting rates and devaluing the US debt note, the USD.

Cash & income-paying Equivalents are at levels that are right for me and my real-world situation. Your situation is different. Cash will be adjusted as needed.

Refer to the Trade Log under the NFTRH Premium menu at nftrh.com for trade info, if interested (not that you necessarily should be). Also, you can follow at Twitter @NFTRHgt for notice of updates.

NFTRH is not to be distributed to third parties without prior written consent

Notes From the Rabbit Hole (NFTRH) is a weekly market report in which we provide analysis on financial markets. We make every effort to provide accurate and high quality content, but this analysis ultimately represents our opinions and these opinions are provided without warranty or guarantee of any kind. See full terms & conditions of service under the ‘About’ heading in the main menu.