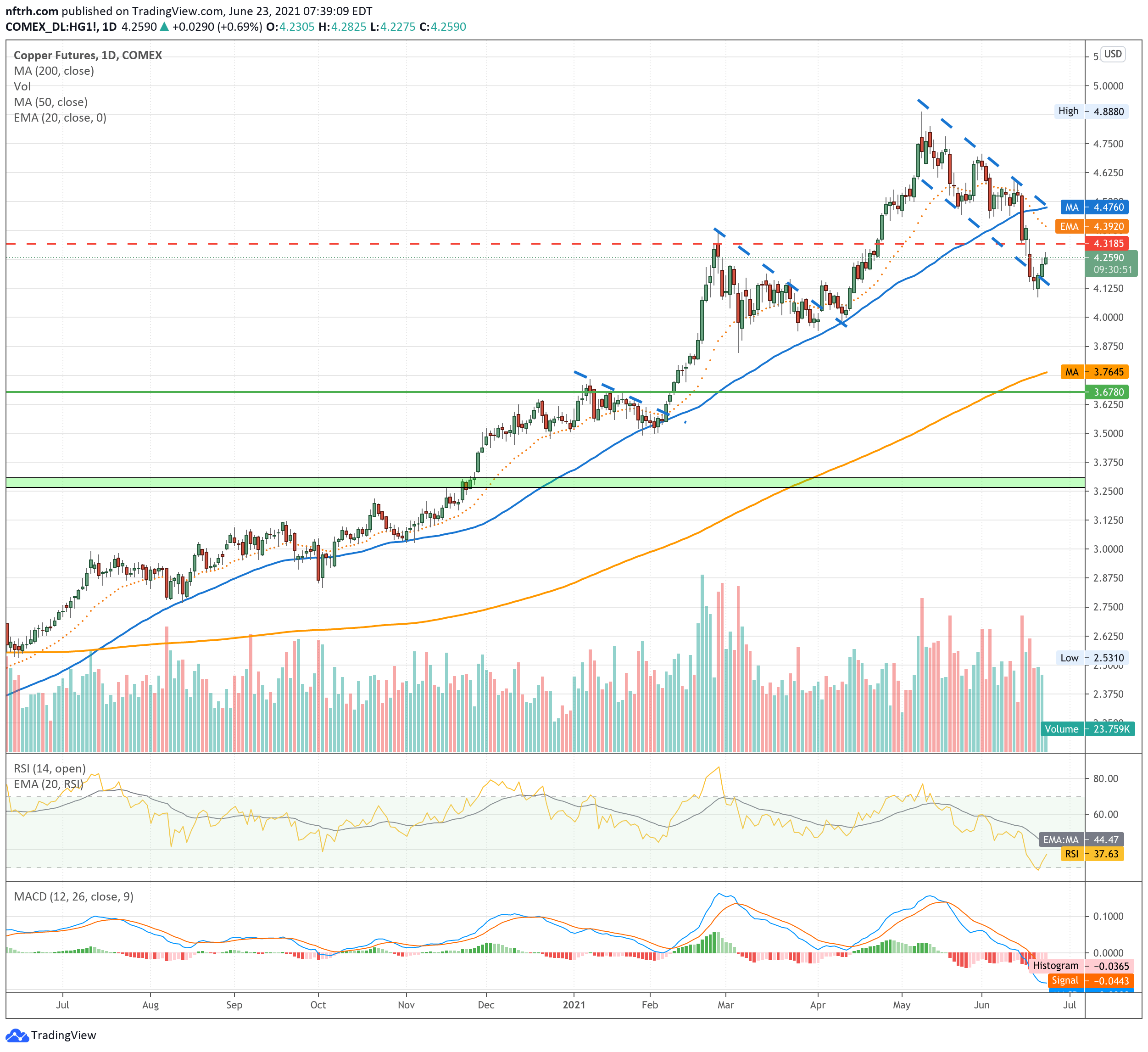

Let’s take a look at the headline industrial metal, copper.

After a fake below the most recent bull flag/correction channel it has popped back into the flag. Key resistance to the bounce will be at the SMA 50 (4.47), which includes short-term lateral resistance (not drawn in).

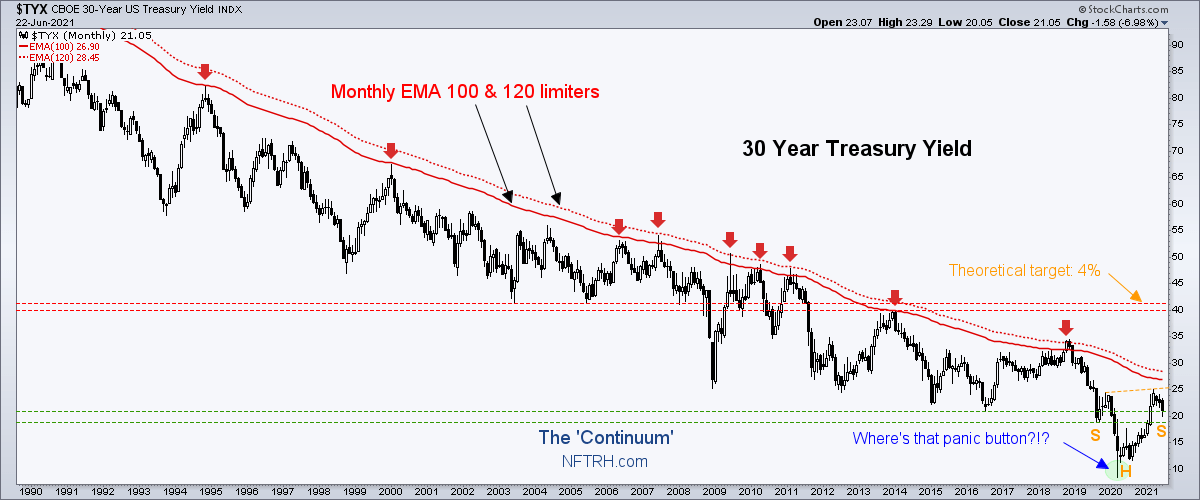

The larger macro fundamentals (let’s visualize just one of several indicators, the 30yr yield Continuum that we have targeted for ultimately higher levels after it makes its right side inverted shoulder) are positive for copper, industrial metals and the wider inflation/reflation trades. The next target on the 30yr yield is 2.6% to 2.8% (current: 2.1%).

As for the miners, the ETF (COPX) held a higher low to the March low and that should be the low if the miners are not going to go into an extended and painful correction. As such, and considering the macro fundamentals are still engaged toward inflation and the inflation trades (beyond this cooling off period) and the oversold level COPX hit last week, we can be open to a resumption of the reflation trades, one by one.

The various commodity/resources tend not to all rally or correct at the same time, and it could be time for the industrial metals as they began correcting sooner and more intensely than other commodity areas. Alternatively, if we start seeing lower lows to the March lows in copper, COPX, GYX (industrial metals index) and individual miners, this inflation/reflation cool down could morph into something worse. The bottom line is that the trends – in both macro indicators and in these markets – are still up and pro-inflation at this time.

We were on the inflationary cool down play before anyone that I am aware of and so, I do not want to be caught falling in love with this play, because it is not the dominant trend. So let’s be open to a coming resumption of the inflation trades (with parameters like the March lows as risk indicators).