I was just poking around older posts and found this one from May 31st…

You Have to Invite the Vampire Into Your House

In this confusing world where the media are telling Joe Sixpack about this weird sounding thing called a yield curve inversion, Trump is jumping up and down on Twitter assailing the Fed chief like no other Fed chief has ever before been assailed before and economic eggheads are laying the breadcrumbs for the Fed to follow to the coming inflation… you wonder why I use cartoons and other pictures of popular culture to make my points?

From the first post linked above I now unashamedly quote myself…

A vampire needs to be invited in order to enter your house. So the story goes. But in this case, we are talking about the Macro house, with its nexus in the USA and its Central Bank.

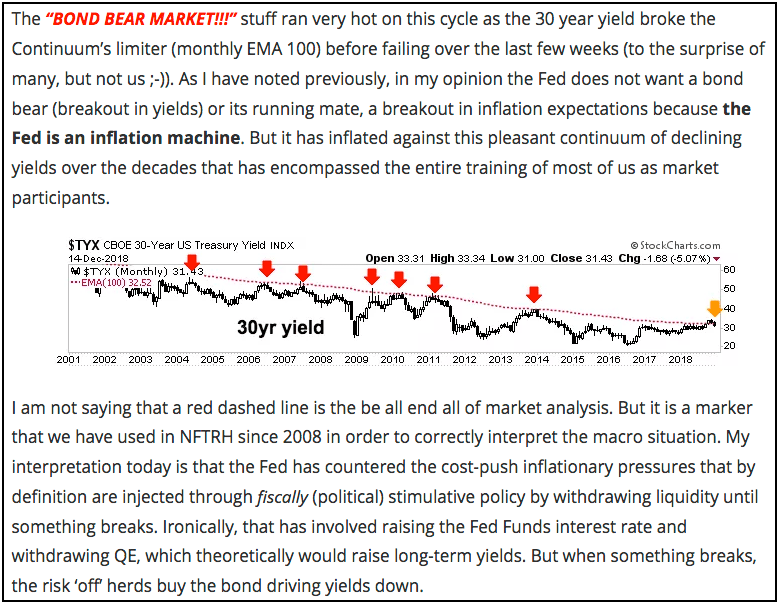

You see, the Federal Reserve inflates money supplies as a matter of doing business, which is why I noted so strenuously in Q4 2018 that Jerome Powell’s then-hawkish stance in the face of a declining stock market made perfect sense… because the 30 year Treasury bond was not bullish; it was bearish and getting more so under the pressure of rising inflation expectations.

So you can see that the Fed was simply not going to stand for a rebellion by the long bond as it threatened to undo its racket of systematic, long-term inflation (an out of control rise in long-term interest rates would seize up the debt-fueled system). The Vampire needed to be invited into the house and the invitation is sent via DEFLATION and the fear thereof! Got it?

But in Q4 the Fed had a threat if its own to deal with as the repercussions of its previous inflationary operations could be exposed to the light of day by the breakout through the Continuum’s limiter if it were not arrested promptly. The orange arrow on the chart below shows the point of concern for the Fed.

Our thesis of the time was that an impulsive breakout in long-term bond yields would end the Fed’s inflationary racket and thus, end the Fed itself (as we know it). Our view was that given the choice between an imploding stock market and a fatal breakdown in the long bond (break up in the yield) the choice for the Fed would be a no-brainer. And what do you know… the Continuum’s limiter held yet again.

This excerpt from NFTRH 530 was posted on December 19th 2018 and also included in the above-linked article.

The red dashed line indeed held once again. Ho hum. And today we have already pinged to the other extreme. Ho hum.

If the process that has been intact for decades is to remain intact, the Vampire has received his invitation and is just awaiting the proper moment to enter the house.

For “best of breed” top down analysis of all major markets, subscribe to NFTRH Premium, which includes an in-depth weekly market report, detailed interim market updates and NFTRH+ dynamic updates and chart/trade setup ideas. You can also keep up to date with actionable public content at NFTRH.com by using the email form on the right sidebar. Follow via Twitter @NFTRHgt.