Well here we are not only with the US market back to the equivalent of the SPX 2815 target area (hit a high of 2821 today and eased back to 2811 to close) but with copper still plucky as noted yesterday and designated as bullish by one mining analyst (Mark at IKN) you know I respect. On a related topic, I continue to hold my China longs. That would be the same China of the decelerating economy at last check.

Back in February we had noted how many US and global economic indicators that had fallen right off a cliff. From EM imports to Atlanta Fed GDPNow, graphs far and wide were looking like this swan dive.

The latest GDPNow estimate out today is even lower at .4%. From Yardeni.com, the CESI is pointing down as well as the stock market stays aloft and economists continue to get downside surprises vs. their projections.

But if the global rally drags on – which there are signs of it doing (for instance, if Mark is right about Doctor Copper) – at some point I would expect to transition to an inflationary phase (for the latest super detailed breakdown on CPI see this post from Michael Ashton) and likely a cyclical inflationary phase.

Mark notes that he is longer of copper than gold. If we go cyclical that would be the right orientation as we often note that gold mining would be a fundamental also-ran in a cyclical inflation although there is no telling how high inflationist gold bugs could push them while their fundamentals erode (see the extended 2004-2008 period and for a brief moment, H1 2016 as examples of this).

So my point is this; the global picture is still generally in rally mode (I even added Russia today) and I see some good charts out there. The S&P 500 is right back at the 2815 decision point. Copper lurks below the even number and confirmed long-term support/resistance level of $3/lb.

I am much longer than short (only short SPY now) along with cash, and to tell you the truth would rather we are able to put on an inflationary and even cyclical trade globally, including commodities. That would be easiest, sort of like 2009-2011 and 2003-2008.

But until SPX clears 2815, shows continued strength (beyond a lame top-test) and Copper clears 3, we’d look for US long-term interest rates start to climb again along with quite possibly the yield curve (which can steepen under pains of inflation) and inflation signals like the 5yr/10yr Breakeven rates, TIP/TLT and TIP/IEF, etc.

Until then, inflation will not quite have taken hold and I believe that if there is no inflation, there is no global economy. It’s how the damn thing runs and that’s why US and global Central Banks have done swan dives of their own, like doves falling out of the sky. Okay, dove dives. :-)

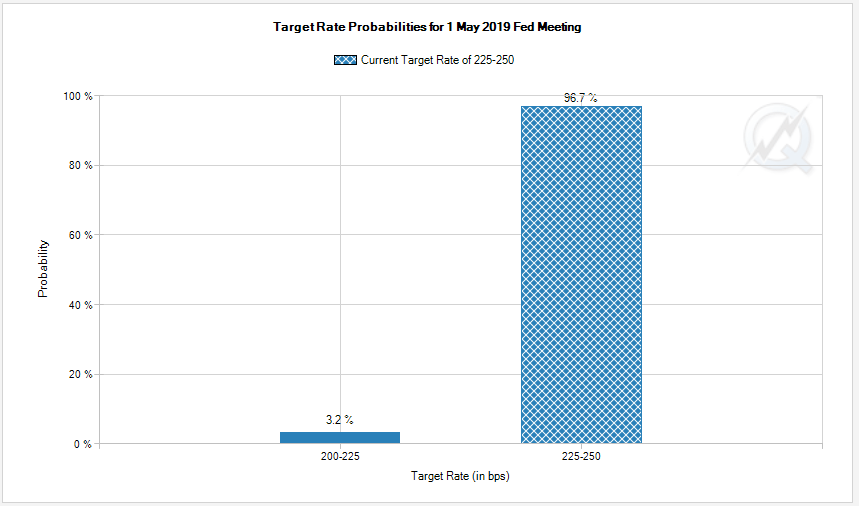

In line with the hopeful atmosphere the Fed Futures wiseguys are still predicting almost no chance of a rate hike through June. CBs are trying to woo inflation now after the Q4 2018 scare. The question is, will it work?

I want to stay disciplined about waiting for the signals rather than jumping the gun. If we go cyclical inflationary a world of investments could open up. But I am going to take this week by week and keep my pompoms for any outcome in particular in the locker until it is time to lean more heavily one way or the other. Those signals will be upcoming before long.