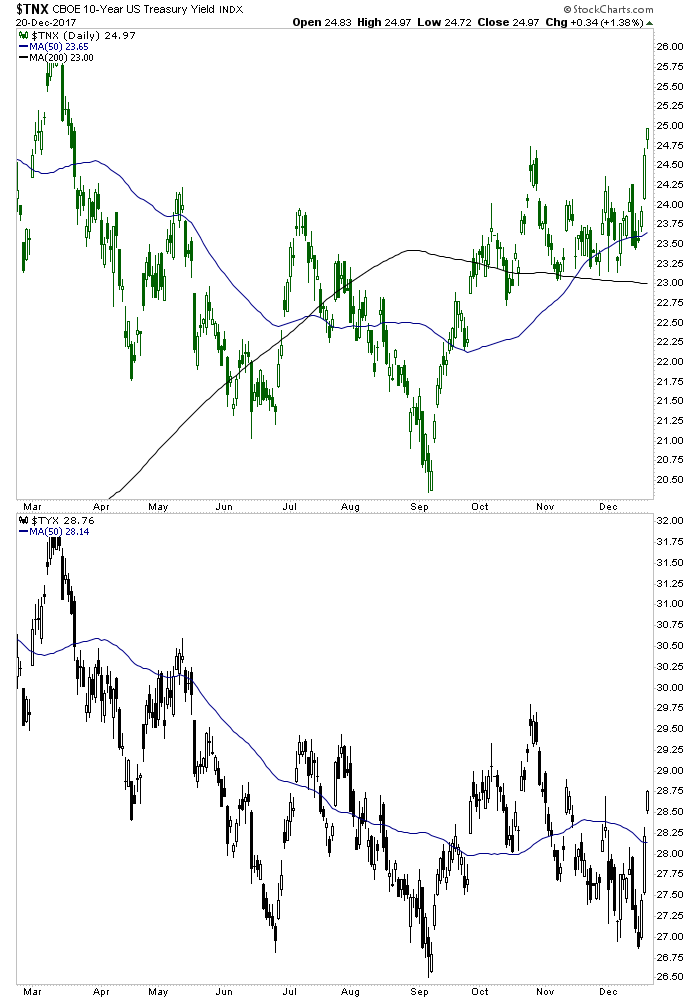

While 10 and 30 year yields are down a bit this morning, the move this week is a step in the direction of the favored view, which has been for this Amigo to ride upward along with the SPX/Gold Amigo to their would-be ‘limiters’, while the Yield Curve Amigo rides downward to or toward flattening/inversion.

Here are the 10 and 30 looking bullish (bearish for 10yr Treasury notes) and neutral, respectively.

After a mostly choppy Q4 my own trading/investing seems to have smoothed out and that is no coincidence because it seems like the macro themes are smoothing out after a lot of Q4 whipsaw. And it’s probably no coincidence that the tax bill wrangling is settling down and people are looking ahead, projecting growth and inflation. Hence, the bump in Treasury yields.

It will be important to either project a continued rise in yields or note a reversal, if applicable!

So again, this update assumes that yields will rise in the near to intermediate-term. That appears to be the play. But we’ll adjust the view if/as necessary, as always.

Here is an article at Bloomberg that gives a lot of details about the various inputs to the bond market. I have not read it yet but a skim of the article looks like it would be helpful. I’ll plan to read it later.

US Treasury Sales Are About to Double [in] 2018. Who’s Buying?

For our purposes we mainly want to know two things; 1) are 10yr yields and 30yr yields going to get to, near or through the targeted limiters (2.9% & 3.3% respectively), and 2) what are the right investments to use in the event they are?

So assuming Thing 1 will happen and the nominal interest rate Amigo will ride the full journey, I continue to believe that more traditional beneficiaries of inflation will probably benefit relative to the stock market, which has feasted on the ‘Goldilocks’ aspect of the current inflation cycle thus far. It doesn’t mean stocks will go down, but I think that assuming yields rise, rotation into areas that tend to benefit from rising L/T yields would be likely.

Making that view doubly attractive is the fact that certain would-be beneficiaries of rising inflation concerns have under performed amid Goldilocks (Energy, Industrial Metals, Precious Metals, for example) and present relative value. Here we recall the bullish patterns in Industrial Metals, which are not too far above the neckline breakouts. As for the PMs, be careful of assumptions. There could be trouble if the yield curve resumes flattening (it’s been bouncing the last few days). They are just part of a would-be inflation trade right now. The precious metals as a unique sector would come into play after an inflation trade is limited and resolved into liquidation.

In the here and now other interest rate beneficiaries are the Banks/Financials, Materials and Industrials, but many of these have been running right along with the stock market. So they may do well, but I think some catch up can be played in the items noted in the paragraph above.

My plan, as long as the interest rate view holds up is to bias toward the inflationary rising rate beneficiaries and not plan to be actively bearish general stock markets until the 3 macro Amigos either ride the distance or abort mission.

I am a little wordy above, so feel free to pop an email if you have any questions or comments.

Note…

I had planned to have a relatively normal NFTRH report this weekend (to be delivered on Saturday) but some holiday related and unrelated logistical details popped up. No, it’s not a Christmas party! :-) So NFTRH 479 will be more of a bullet point summary. I am sure you have other things to do as well and may appreciate its focus and brevity.