The Semiconductor Equipment book-to-bill ratio for June came out last night and it remains solid. While bookings eased a bit they remained elevated and billings were the highest since 2011. So the question of whether this earnings season should be solid for Semi Equipment companies is answered; it should be because the April-June quarter was significantly better than Q1.

Some companies related to Semi equipment and materials are AMAT, LRCX, MKSI, BRKS, TER, KLIC, CCMP, ACLS, VECO, UTEK and ASML.

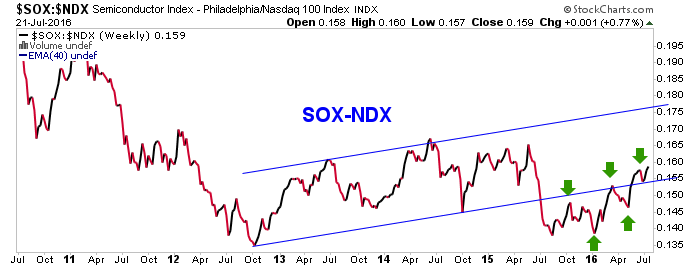

The SOX index includes some of these companies and many Semiconductor manufacturers. It continues to lead the broad US market on an intermediate-term basis.

Now lets look at the cross reference, the PALL-Gold ratio. While it has not crossed the weekly moving averages up it does continue to look like a double bottom, even recently forming a ‘W’ pattern and popping above the moving averages.

At this point the case for an economic bounce and positive market signals continues to build. This sounded like crazy talk 2-3 weeks ago when the world was ending and perma bears were in control. Now? Not so much. But anything can and usually will happen in a market that is so stoked by obsessive policy input, so we can just evolve our story week by week and be open minded.

Yesterday in a public post a target was established for the S&P 500. I’d love to see a drop toward 2100 to clear over bullishness but regardless, SPX targets 2410 as long as it’s at or above the noted support zone.

Globally, I see no reason not to continue favoring India, Emerging and Asia (ex-Japan). These weekly charts are all from NFTRH+ updates. The iShares India 50 ETF tested support and remains in an intermediate uptrend channel.

EEM weekly has now turned the neckline to support. Next time you see this chart it will be green, assuming it remains at or above 35.

AAXJ looks very good. So much so that I am starting to think about not trying to be stingy about a global ETF that I want in the portfolio for balance and strategy reasons. In other words, I may not wait for a pullback that might not come. I took a loss on the frustrating DBA yesterday, so there is some room to add it. I am not looking at these items as trades so much as being on the right side of the macro picture for an intermediate phase as long as said phase looks good.

I do not like the chart below as a would be ‘inflation trade’ participant. Commodities are a bit weaker vs. the broad market than I’d like to see on a pullback. Nominal CRB still looks like it can drop further and our target is around 180 (183.67 currently). I am not yet interested in commodities or the ‘inflation trade’. Remember, the first phase was a bounce, any coming pullback that would find support could set up an extended run but the complex is not there yet.

Now we’ll shift to daily charts for the precious metals sector. HUI got to 273.62 (target 275), consolidated and dropped. Last week I speculated that the sector has better than 50/50 odds that the rally’s highs have not yet been seen. That, in my opinion, remains the case. No major correction is indicated until/unless Huey breaks down below the 50 day moving averages. By the same token, that is where people looking to re-buy could add positions, with a ‘stop loss’ on that thinking being a breakdown from the channel.

Gold is consolidating rather than correcting. Last weekend we noted some concerns for gold, especially in the area of interest rates. But technicals are a separate thing and this chart, at face value, is bullish and remains so above 1290.

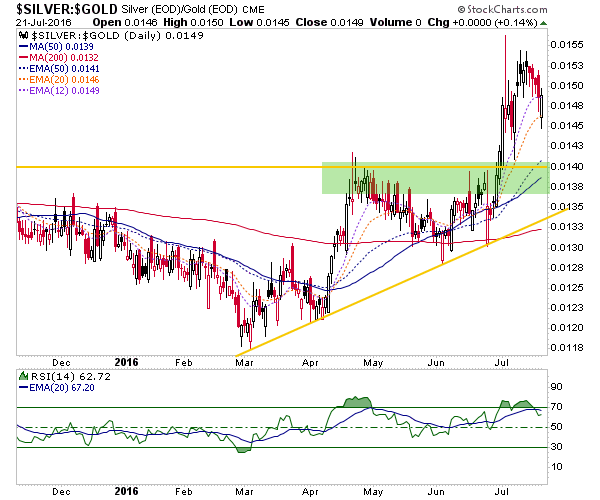

Silver became over done and deserves a trip to 18, which would look like a good buying opportunity.

Bringing it to a macro view, silver vs. gold did great work in signaling the bullish environment for stock markets (in the face of the Brexit hype, no less), the bounce in commodities and the bullish atmosphere for precious metals in general.

The ratio looks like it can continue to ease but the bullish trend from early March would only be broken with a loss of the 200 day moving average (red). The implication, if Silver-Gold continues to pull back, is the potential for continued short-term volatility in the precious metals, commodities and potentially, stock markets. But the latter are riding a cool wave of good feelings and are less sensitive to a firmer US dollar; many US stock sectors, at least.

Bottom Line

Our theme has been bullish stock markets with the potential for a short-term pullback, but intermediate-term rally (potential target SPX 2410) and long-term bearish. Favored US sectors remain Healthcare and Semiconductors. Favored global areas are India, Emerging and Asia ex-Japan.

Commodities continue to pull back with a target of CRB 180 (+/-). Commodities vs. SPX are weak, and I am not yet interested. Inflation expectations are still muted.

Precious metals are on a potential pullback but with no indication of the end of the first bull phase. That would be tested if/as HUI settles to its 50 day moving averages and the trend channel’s lower line.