It’s the Wild West

The segment’s title references two things.

- I’ve always said that “investing” in junior/exploration mining stocks listed on the TSX-V is like the wild west, with adventure, profit and bust out failure all in play, and…

- Literally, the U.S. based minerals/resources stocks are mostly operating in the west, including Alaska, and some like Talon Metals, in the northern mid-west. Canada is more distributed East to West, with British Columbia and the Yukon being mining havens.

Let’s focus on U.S. stocks, given the Trump admin’s (in my opinion, right minded ) desire to invest in the mineral resources sector. You can (and I do) say a lot of negatives about the guy and some of the clowns he has appointed to the administration, but he is somehow smart enough to surround himself with sharp economic people (IMO) who know what they are doing, in some cases.

The team advising Trump on strategic acquisitions (which began with the DoD’s investment in MP Materials) is in my opinion doing exactly what should be done in a world of unfair trade balances, set up by the greed on Wall Street, goring out America’s manufacturing base (I was there dealing with it, automating to survive it, remember), putting U.S. manufacturing on its knees, impairing mining and other “dirty” jobs in service to King Dollar and the mighty U.S. consumerist/services economy. It was all finance, baby.

You don’t need me to go on about the real manufacturing that went on back then (beginning in the “trickle down” 1980s that did not trickle). We as a greedy nation led by the Wall Street/Washington alliance, outsourced it all and manufactured a massive and sprawling rust belt while financially backed palaces in the sky were built to house millions of 9 to 5 clerks and corporate ladder climbers to operate the vast, growing (and financialized) services economy.

This brings on an…

Interlude

While I have actually witnessed abuses to the environment happening in the bad old days, which needed to be regulated (and how), the EPA and in a different area, OSHA became like thugs making you jump through an inordinate number of regulatory hoops. We had our ship battened down environmentally to a closed-loop overkill degree, making sure we were tight because, well, I was scared of EPA. While we were not polluting before hand, I felt the nee to throw 10s of thousands of dollars into over-killing the closed loop system just to make sure.

I also had to waste a couple days dealing with OSHA, because they did not like the wiring on an outlet or something like that. They stopped in one day, looked and looked until they found something, took up two days of my time and then dropped a fine on me. All this after we’d modernized, automated and done everything to be a top notch globally competitive manufacturer. Frankly, I hated having big brother leaning on me because with China and other cheap labor hubs constantly undercutting American manufacturers, the whole thing did not feel worth it.

That was due to not only lack of support by the U.S. government, but a perceived adversarial relationship with the government. That’s how it felt back then. You’re doing all you can, and then some administrator walks into your shop and “finds” something.

Interlude within the interlude: Since I am airing my grievances about the way things used to be, I’ll also detail the most galling example of government not working for my company, but instead, actively against it. We won a contract by $40,000 less than the “other guy”. I ask Dan, the buyer, “WTF are we not getting the award?” His answer: “Gary, I gotta go to a minority. I’ll get you later” (I don’t recall he ever did). The government routinely and willingly paid more to entities that had the status of “minority”. Yet all too many of these entities were not materially representing minority interests. Awesome.

Here’s the thing; those “minorities” were often either a company full of white people with the guy’s wife installed on top, or a company full of white guys with a person of minority nationality installed at the top. Good old boyz gonna be good old boyz and dey gonna play da game. The government didn’t seem to care as long as the i’s were dotted and t’s crossed. A lot of sharp players knew how to dot and cross. Personally, I just wanted out.

Back on message, the initiatives by EPA were necessary. As I said, I saw abuse in my industry that just should not stand. It’s the overreach and punitive nature of the relationship between government and industry that was bad (at least back then, I’ve been out of the game for 13 years).

That is unrelated to our discussion of mining, but this punitive relationship was a concurrent challenge for manufacturing that piled on with the global outsourcing that systematically eroded America’s ability to robustly manufacture for itself. It was led by Wall Street types and politicians in whose pockets Wall Street resided. We became a nation of consumers and services recipients in the financialized economy with the King US Dollar sitting on top of the whole thing.

America had largely risen above the dirty jobs, like making things with the equipment necessary to do so, or digging critical minerals out of the ground, again with the equipment necessary to do so. Speaking of dirty jobs, I believe that if a large portion of politicians could have simply voted “make mining in the U.S. illegal” they would have done so. Manufacturing too. Let other countries do that dirty work while we rule the world under King Dollar’s tyranny.

In my agreement with current policy, I am talking my book as we began tracking the strategic investment case for MP back in 2023, and it finally proved out in 2025, under Trump. MP is the daddy, the Rare Earth producer and processor. But the case for small, viable exploration situations is compelling. This goes beyond REE and strategic minerals, obviously, with gold flying around at $4,000/oz. and silver at $50.

Au, Ag, Cu, Ni, Pd, Pt, Li and various REE.

As I look back on the last few months I realize that I began with a “basket” concept, as you may recall. A group of highly speculative, mostly TSX-V listed items for pure gambling. But over those months new information has been presented.

Information like the admin taking interest in smaller “resources” companies, as opposed to the already producing MP. Information like the TSX-V’s relentless drive upward from the depths of an 18 year hell. Information like gold, silver and now other metals ramming higher, which means demand it strong.

Strong demand presents a problem for miners of finite reserves. Hence, the hole diggers up north and west who’ve been nearly asphyxiated for 18 years. In short, I am coming to see the play as having progressed from “basket” speculation to “try to find the best, most strategic and viable items and hold ’em.”

Among my holdings in the speculative exploration stocks operating in the U.S., Talon Metals is in Minnesota, Bitterroot (the stock is quite illiquid) in Michigan and Nevada, Metallic Minerals in Colorado and Canada’s Yukon, and Stillwater Critical Minerals in Montana and Alaska, along with interests in the Canadian Yukon, BC, and Ontario. All of these stocks are multi-metal/mineral.

Lest I forget, my holdings exploring for metals/minerals in the U.S. also include Idaho Strategic Resources (small gold miner with a large REE land package) and Dakota Gold. I also added Lithium Americas, after it got Trumped but then declined sharply before making new upside.

The point being that while I think the case is compelling for viable (read: non-scams) projects in the U.S., Canada and around the world, the Trump initiatives and “in the books” investments like the MP, Lithium Americas, Trilogy and Intel show an obviously motivated administration, putting its semi-nationalization strategies where its really big mouth is in the United States.

Here I will repeat that I have guidance from a couple geologists in the subscriber base. I plan to introduce them at an appropriate time through Podcast interviews and possibly written content if they so desire. Two things here: I’d like to get through my treatments first, feel okay, and then get going. The other thing is I have to figure out how to effectively set up a Podcast. Yes, I just wrote that. Maybe my daughter is up on that stuff, but I’ll take any advice you might have.

I would not have even known about Talon if it were not for Michael. I would not have know about Stillwater or Metallic Minerals were it not for Greg. The keys here are not only Trump (his people are not going to be taking interest in holes in the ground with no validation), but also investment sponsorship of large miners and/or proven expansion of resources.

I’ll let Greg have the last word, speaking generally about the mineral exploration sector:

With the mining industry reliant on the juniors for nearly 100% of future production through dependence on the market to fund early stage to advanced stage projects (the majors only do exploration around their existing mines to replace reserves that have been depleted), and having starved those same juniors of capital for over 15 years, I think we are seeing the beginning of a generational revaluation of resources in the ground from extreme discounts to something that more realistically reflects the challenges of finding and developing these critical assets.

Bessent on the Right Track?

Am I going to add another positive check mark to an otherwise chaotic and sometimes infantile, sometimes petty, always vindictive Trump administration? Well, let’s see who Bessent picks as Fed Chair.

SecTreas Bessent, is interviewing a list now down to five Fed chair candidates, none of whom are named Miran. At least one (Rieder) has ideas about rolling back the Fed’s all omniscient power. If so, I was wrong in assuming Trump would install a robot who would simply carry on and make the worst of the Fed from Bernanke on, even worse.

“Roll back the use of some of its tools”???

Those “tools” created inflation through Funds Rate policy, QE, MMT and ever more eggheaded experimentation. Then when that went too far they went off the charts cynical (Bernanke: we’re going to “sanitize” inflation signals, he actually used that word) and ever more ingenious (and destructive) means. That God damn egghead created Operation Twist as a corrective to his previous policy.

And you wonder why the bond market erupted in 2022 and puked all of this toxic garbage up?

Maybe I am being naive in catching a glimpse of someone saying something I’ve been advocating for since Bernanke took us off an unsound path and right into a Wonderland of magical (and inflationary) possibilities. Please allow me this moment of positivity. :-)

A Trifecta for the Orange Man

All sides seem to be laying the credit for the cease fire in Gaza at Trump’s feet. You can click the pic to read, if you’d like. You can (and again, I do) say what you want about this lunatic, but he’s gettin’ shit done in a world that probably needed a cattle prod right up its behind.

I’ll reserve further comment on Israel/Gaza because the politics behind the cease fire are anybody’s guess, and the true effects may not be known for some time.

Silver’s Pop, Drop, Pop

When I made the update in pre-market (U.S.) on Thursday it just felt overdone. Silver was up again and it was banging through the 1980 (Hunt Brothers) and 2011 (inflation hysteria) highs. It was a set up for short-term failure at least. While my puts quickly registered profits of 100%+, the silver price did not really suffer in any abnormal way. It was a classic bull gap & trap (in SLV).

I had to figure out if I was an investor guarding precious metals positions for the longer haul or a dirty rotten trader. It turns out I was that second thing. The put positions were relatively heavy and they spun off a big profit, so this dirty rotten trader took profit. The darned puts, combined with those on GDX and GDXJ, actually had me very green overall during the worst of the pullback. I’d have had to buy a ton of ZSL in order to get performance similar to what these little options did.

Then, going back to the well (the scene of a successful trade, often not a good thing) I added back the puts on Friday, but only in half the size of the original positions. That is because things are much less clear to me right now compared to Thursday morning. Silver so easily could bash through that 50 (+/-) and leave it behind, much like gold did with our previous but long-standing target of 3000+.

So now, along with the GDX puts, I am back in “insurance” mode with hedging that eats away at my upside potential, as it should, while at least partially protecting against a potential real pullback/correction (the likes of which were illustrated for Silver in the update linked above).

The precious metals complex is fully capable of sending this insurance to options hell, which would mean other areas of the portfolio are succeeding. It’s the weird way of hedging.

Precious Metals

Gold: $4017/oz., new all-time highs.

Silver: $50.12/oz., new all-time highs.

HUI: 613.23 after ticking above the 2011 high of 638.59, to a new all-time high of 642.46.

So there it is. By definition of momentum and price activity, the situation is bullish. What’s more, we have consistently viewed both the macro fundamentals (e.g. gold vs. stocks, inflation signals, commodities and the cyclical macro) and mining operational fundamentals (e.g. gold vs. cost inputs like oil and materials) as positive.

In other words, the big time upside has proper fundamentals behind it, even with the stock market keeping up nominal appearances. Ideally, we’d want stocks to be in a bear market for a purely positive fundamental view of the gold mining sector. However, stocks are entering a terrible bear market right now. It’s just that it’s only visible in “real” terms, gold terms.

I just love this chart. Yes, the dorky nerd sometimes falls in love with the charts he stares at. with the hook downward at the far right it sure does look like casino patrons have already missed the first and best bus out of Stocktown. Although, with their SOX, NDX and SPX still flying around up near all-time highs, they don’t see it.

Remember, most patrons are not dorking out on ratio charts and analogs like this. They are cheering AI and mentally masturbating about “Tokenization”. In other words, their heads are in the clouds of the previous macro phase. The herd will come into play far down the road when we sell to them.

Off that soap box before I make any more off color statements or write any more bad words.

Precious Metals Bottom Line

Bullish, with gold, silver and HUI in essence at/above all-time highs. And it’s about time!

That last sentence says it all. While there is risk of sharp pullbacks or corrections at any time in a real bull market driven by real fundamentals, a major consideration is how long HUI, GDX/GDM, etc. were in the wilderness. Or if you like, on a cold street corner, tin cup in hand while the suits on Wall Street with slicked back hair, $10,000 suits and $50,000 watches * stride by, not wanting to even take a look at Huey, let alone drop a nickel in his wooden can, or those of his fellows.

The same can be said for mineral resources exploration sector, which was almost literally asphyxiated (capital-wise), but which has incredible supply/demand fundamentals shaping up in a trade war torn world. Still gotta pick the right ones, but work with me here.

The point is, you get a real bull market after so many years in the wilderness, there has got to be pent up demand even from the believers, let alone the drones who are still getting their heads turned by Tokenization and AI.

The bull market has a long way to go. It is going to get violently volatile at some point. Personally, I am going to try to deal with that as I have been. Being ready hedge with options at points of high energy, like I felt silver’s Thursday morning smash upward was.

In a bull market, that one upward pop and drop may have cleaned out the market for a few days or weeks. It may also have been a sign that the goons are going to defend 50. I just don’t know. So I am going to go along, every week measuring the macro, the sector and weighing the odds of rally vs. pullback.

In a perfect world I would like to be hedged while adding preferred positions. I did just that in increasing positions in PGE.V and MMG.V, after admitting my mistake in paring them down to begin with. They are not nearly pure precious metals exploration, but I mention them by way of general example.

Let’s end with an internal look at the miners vs. the metals. When the first real correction comes, it will come with these two items breaking down. Not terminally, but severely. As yet the HUI/Gold and SIL/Silver ratios are completely intact with the HGR looking for a normal tap of the 50 day average, while the SSR breaks its SMA 50 and looks to the green shaded zone for a still normal, but fairly deep test.

These, along with the Gold/Silver and Silver/Gold (see end of report) ratios should provide guidance. Right now it’s pretty normal. It could even be considered healthy. But as I’ve parroted for a while now, a correction will come and it will not be comfortable if it’s not anticipated.

* I have no idea how much a fine suit costs as I’ll only get dressed up if absolutely ordered to by my wife, and the same goes for a fancy watch. Haven’t worn a watch in decades. But if I did it would be a cheap functional one. As an irrelevant side note, you would never catch me wearing anything gold either. My only jewelry is my silver wedding band. I can’t stand the sight of men wearing gold. But I am a lunatic of my own kind, I guess.

U.S. Stock Market

SPX took a hard drop on Friday amid renewed Trump-China trade war noise. We shall see if that is just an excuse to correct or not. My guess is that it was an excuse to pull back and shake ’em out.

SPX is making a test of the uptrending 50 day average. It could even decline to the uptrending 200 day average (6050) and still be technically intact.

The key chart resides in the segment just above. I expect the stock market, king of the Greenspan>Bernanke>Yellen>Powell era, to relinquish its crown and be exposed as a bloated pig. It may continue to make Americans think all is well with their 401Ks, but in reality the real, gold adjusted price looks about cooked.

If gold takes a serious correction, I’d expect SPX to take one at least a severe given the ratios between the two markets from short (daily chart) to long (monthly chart) term. If gold and silver keep bulling, the stock market may continue to keep up appearances.

The SOX > NDX > SPX leadership chain is still fine, despite Friday’s market drop.

However, Junk bond spreads did tick up a bit last week. Upside follow-through would indicate building market stress.

It’s companion, the VIX also popped, to the tune of 32% on Friday. Follow through here would also be painful for stock market patrons.

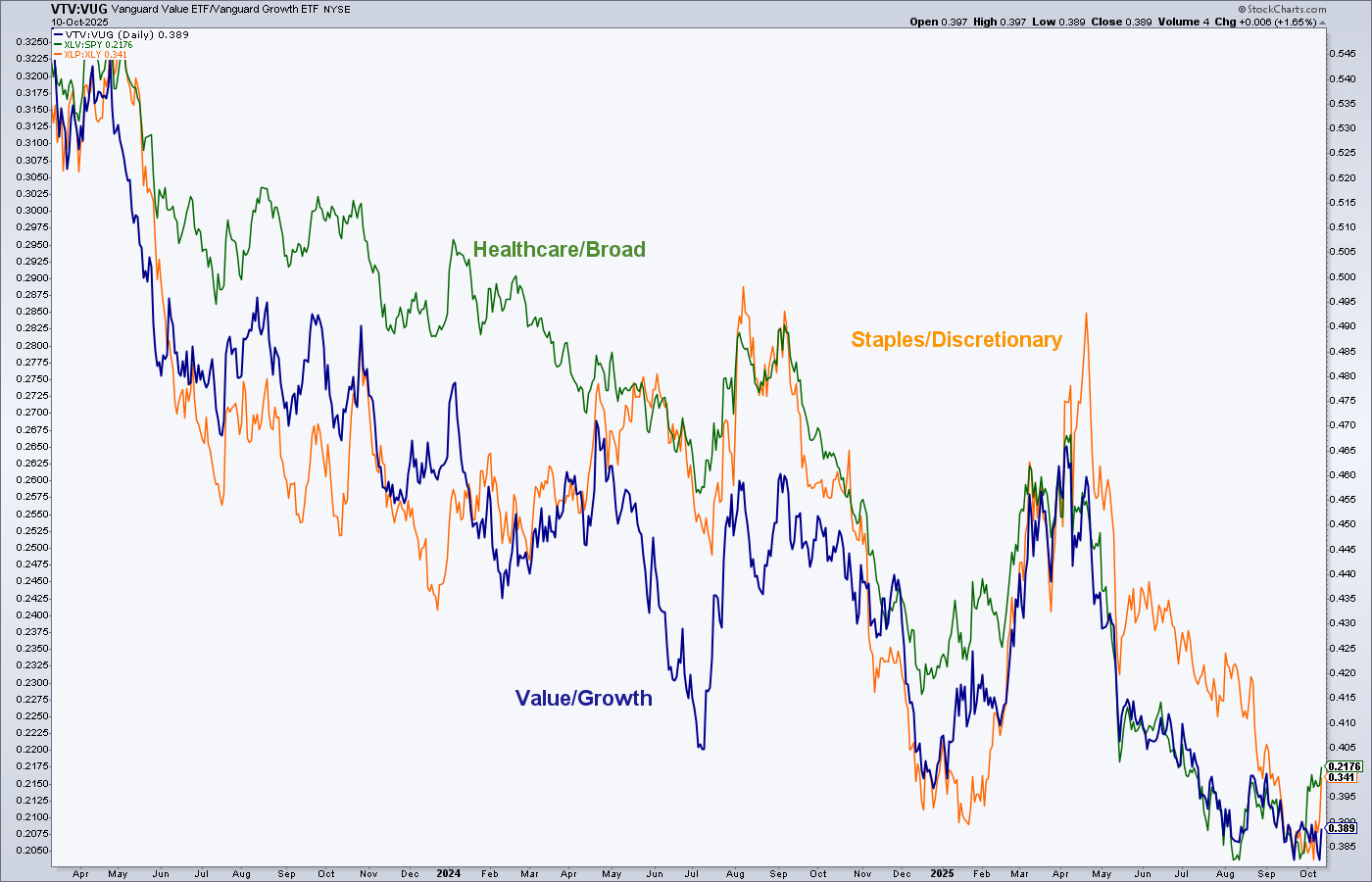

The up-close view of the XLV/SPY ratio (relatively defensive sector vs. broad) is still postured to bottom. That does not mean it has bottomed, but it’s set up that way. If there is follow-through here too it would go nicely with the two charts above.

Meanwhile, XLV/SPY and its fellows have a lot of work to do to turn the macro defensively bearish.

Bottom Line

While trends are up and certain leadership internals are still positive, last week closed with a few signals in not so pleasant alignment. Junk bond spreads rose, and will need follow-through to continue inflicting pain. VIX popped and would need the same. The XLV/SPY ratio is on the verge of making a short-term risk OFF signal.

While I did not short anything because there was no setup, just a drop, I will continue to clean out more bull stock positions if/as needed. I’ve already gotten rid of several, in some cases to limit small losses and in others to grudgingly take profits. The Portfolio segment will show what is still there. I actually came close to increasing my ALAB positioning, as an example of how I may actually want to buy this stock market pullback.

I think there is a moderate possibility that Friday might have been the start of something deeper, and if so, it could affect the precious metals, strategic commodities and other areas that have been raving bullish. But that’s all speculation for the moment. The bulls have the ball and thus, the bulls have the advantage. Let’s see what the market holds just ahead. Friday may have just been news-driven blip.

A narrative has sprung up in the media that we are entering a positive seasonal and that a bull/bubble ends in an upside blowoff. I would not take either of those prospects as gospel. Just possibilities. If some of the negative indications needing “follow-through” actually do follow through, a solid market correction could easily manifest.

Meanwhile, the broad stock market is still bullish.

Global Stock Market

The world (ex-US) also apparently quaked at the prospect of Trump-China. ACWX is also testing its 50 day moving average.

It’s ratio to SPY remains undecided about who’s going to lead going forward, the U.S. or the world which the U.S. is increasingly segregating itself from.

The answer will likely come in the form of the U.S. dollar’s fate. USD did not like the trade saber rattling on Friday much as it did not like the trade war hysteria back in the spring. A resumed downtrend in USD would probably see the U.S. underperform and global outperform, if recent history repeats. A continued rally in USD would likely bring the opposite.

Closing With the Silver/Gold Ratio

Among the only items that did well during trade war stuff in the spring were gold and the counter-cyclical gold miners, which got hit and quickly recovered. Even silver got cracked hard back then. Another reason to pay close attention to the relative performance of silver to gold as the Silver/Gold ratio continues to poke a decision point of “success or failure?”

I think that the SGR is important to much of the macro right now. If this weekly chart breaks above the April high we’d likely have a big asset market party. If it fails as it so often has at similar junctures, the pain could be pretty widespread.

I’ll reserve judgement on gold miners because a failure by the SGR (rising the Gold/Silver ratio) would represent a fundamentally pure macro situation, and they did remain unbroken in the spring, unlike most other markets.

One issue for gold stocks would be the makeup of the investor base. You just know there are silver bugs, inflation bugs, “America first” bugs, non-believer institutional bugs and plain old momentum and FOMO bugs in there.

Any bugs who don’t fully understand why they are there would puke first, ask questions later, especially if the Gold/Silver ratio were rising along with USD.

So let’s watch the Silver/Gold ratio as usual, shall we? The mode has been and still is week-to-week.

Portfolio

Gold is and has been viewed as long-term risk management & monetary value/stability in a balanced portfolio.

Taxable Account

In order of position size. Running short on time, so this week we simply present the current holdings with no further notes.

The taxable account carries high cash levels as long as cash and equivalents are paying out. This is considered a savings account of sorts, rather than a speculation or even investment vehicle. The goal is to speculate around the periphery. In another market phase (e.g. post-crash), the account may get much more in the game.

Trading Account

No positions.

Roth IRA (non-taxable, no contributions)

The chart is still being driven by the guy with the white knuckles, week-to-week.

Cash & Equiv is 74% in a risky market. Watching silver’s relationship to gold and the stock market’s character in order to decide whether to reduce cash, add cash or add shorts/puts. For now, I am comfortable, unlike the guy driving my chart.

Cash & income-generating Equivalents are at levels that are right for me and my real-world situation. Your situation is different. Cash will be adjusted as needed.

Refer to the In-Week Notes under the NFTRH Premium menu at nftrh.com for market talk and occasional trading info, if interested. Also, you can follow on X @NFTRHgt for notice of updates.

NFTRH is not to be distributed to third parties without prior written consent

Notes From the Rabbit Hole (NFTRH) is a weekly market report in which we provide analysis on financial markets. We make every effort to provide accurate and high quality content, but this analysis ultimately represents our opinions and these opinions are provided without warranty or guarantee of any kind. See full terms & conditions of service under the ‘About’ heading in the main menu.