Summary of NFTRH 751 and the Macro Situation Leading Up to It

US Stock Market: Q1 Ends, Bear Market Rally (BMR) Intact

We come to the end of the Q4 (2022) – Q1 (2023) rally we projected back in November. As I was driving my daughter home from a train station in Connecticut yesterday we were talking about media headlines and markets. She searched “stock market” on her phone and up came headlines blaring about the rally and in particular, how Tech stocks are leading the rally. It’s too perfect, and it would probably be too perfect for it to have ended on Friday with the end of Q1.

But it is perfectly aligned with what we – and no other entities that I have seen – anticipated months ago; a bear market rally (BMR) that would have a Goldilocks (inflation fading along with Fed hawk angst) component to it that would boost Tech (and Semi) into leadership roles for the BMR. I am not tooting my horn here (okay, I guess I am, a little). Just stating facts. The stock market has done as we anticipated… and it is still doing it.

So what is next? Well, in my opinion the next BIG thing is going to be the bear’s resumption. But in the meantime, we are allowing for higher levels in this sentiment adjustment rally to rebuild the bullish mindset (fragile, gambling addicted, FOMO’ing mindset that it is). But the next smaller thing may well be to finish up the BMR.

Daily SPX held the 3900 area support, proving not to be in a short-term bear flag, after rising from a successful test of the December low of 3764.49 and taking out the daily SMA 50. Then on Friday it added emphasis and thrust to close out the quarter. With the index not yet overbought we’d look for a higher high to the February 2nd high of 4195.44 and finally, a gap fill at 4219, which is the unfinished business of this rally. That and the resistance at 4300 are the favored resistance to cap the rally. The less favored scenario is a test of the highs if a real unbridled FOMO * sentiment event takes place.

* FOMO = “fear of missing out”. I include the definition because I hear that my lingo is not understood by all.

I am unable to access my Sentimentrader account and do not know what the problem is yet. But we have enough alternate sentiment views to suffice. Sentimentrader’s readings tend to be very short-term and skittish, anyway. Last we checked in, however, the one reading I have the most interest in, Smart & Dumb money indicators, showed dumb rising and smart fading. This weekend, it’s a pretty good bet that the picture is worse from a contrary sentiment perspective.

Meanwhile, the other usual suspects are aligned as follows:

AAII (Individual Investors): Over bearish and contrary positive on March 29. The market then did the logical thing and rammed upward in the face of Ma & Pa’s bearishness. But sticking to the 3/29 reading, sentiment was constructive for a continued rally with the Bull/Bear ratio at .5.

Investors Intelligence (Newsletters): Well off the depressive lows but the Bull/Bear ratio was still muted at 1.52 on 3/28. We have noted that newsletters tend to be more stable, sentiment-wise than Ma and Pa, who are trading their own money. This reading is okay for the market but when the newsletters start to spike their bullishness we’ll have a good warning.

NAAIM (Investment Managers): Here they go again, as of 3/29. NAAIM have been reliably aping the market, signaling its micro rally highs and its pullback lows. You can bet that after 3/29 they chased the market higher and are a developing contrary sentiment negative.

Okay, the Sentimentrader glitch is fixed. Here is Smart/Dumb showing dumb rising aggressively now. As dumb emboldens it will make good sense to become increasingly defensive about this rally. I think we are in late innings or if you prefer golf, well into the back 9 of the rally.

Meanwhile, the US market leadership chain is intact with Tech still briskly leading the broad market and Semi consolidating in Tech terms and leading broad SPX as well.

Interestingly, the Bank index continues to be very depressed in relation to SPX after the ratio tanked from what had already been a downtrend over the last year. Not good internal market signaling at all and maybe this will eventually crop up as a fatal flaw in the US market’s internals after the sentiment fueled BMR terminates.

More Indicators

Speaking of the banks, the indicator that would signal real trouble spiked but has halted with a non-fatal spike, as yet. Libor/T-bill yield is not yet alarming. But we will surely keep it on watch as one of the market’s under the surface macro indicators.

High Yield (junk bond) spread is rolling over and is supportive of the bear market rally in the short-term if it continues to do that. When this indicator rises for real (e.g. Q1, 2020), everyone out of the pool (or short if that’s your thing).

The 10yr-2yr Yield Curve is on a historic inversion to a degree not seen since 1981. As you can see, a new steepener (and it’s coming) is not yet confirmed. The most recent trend has been the Fed fighting the inflation it created with steroidal policy on the short end in relation to the more “free” * market influenced long end (10yr). As the market transitions from this pleasant and interim Goldilocks phase to what I believe will be significant market (lack of) liquidity events a steepener will be driven by the herds flocking to the liquidity of short-term Treasury bonds, driving those yields down nominally and in relation to those of bonds at the long end.

When it comes, a rising YC would signal economic recession (in my opinion) of the deflationary kind.

* With the Fed manipulating bonds of all maturities for various purposes, I don’t actually believe we have a “free” bond market. It’s more like a market they’ve used as a tool and that is the reason I have growing conviction that this tool will no longer be as effective as it had been because something changed, as exemplified by the broken Continuum, among other things.

The ‘real’ yield on the 10yr Treasury note continues to grind out a volatile phase that could be a preparation for a top in Fed policy control and inflation hysteria, and a precursor to a coming deflationary event (if our analysis theme of Inflation>Goldilocks/Disinflation>Deflationary liquidation plays out according to plan). As a side note, gold bulls definitely want to see this control wrested away from the Fed and its appearance of total control.

After all, they were able to exert this control for at least the last 20 years and the work we’ve done to this point indicates that jig may be up. Ref. Friday’s public article on the Continuum and gold.

The Fed’s balance sheet is a concern because it bloated to an epic extreme in 2020 and 2021. That latter part of the bloat came even as most rational observers realized that a significant inflation problem was already in the works while the Fed blathered on about its “transitory” nature. This alone should show us that the great and powerful Fed of Outer Limits fame has lost its fastball. Meanwhile, the balance sheet actually hooked upward I assume in response to the banking meltdown (of sorts). It is also a potential clue about a coming hyper inflation that could come with a deflationary liquidation as its trigger. Confusing? Not to me. Logical.

If you are of a mind to, you might want to read this segment over again and also please let me know if something is not making sense or if you think I am barking up the wrong tree. We need to get this right.

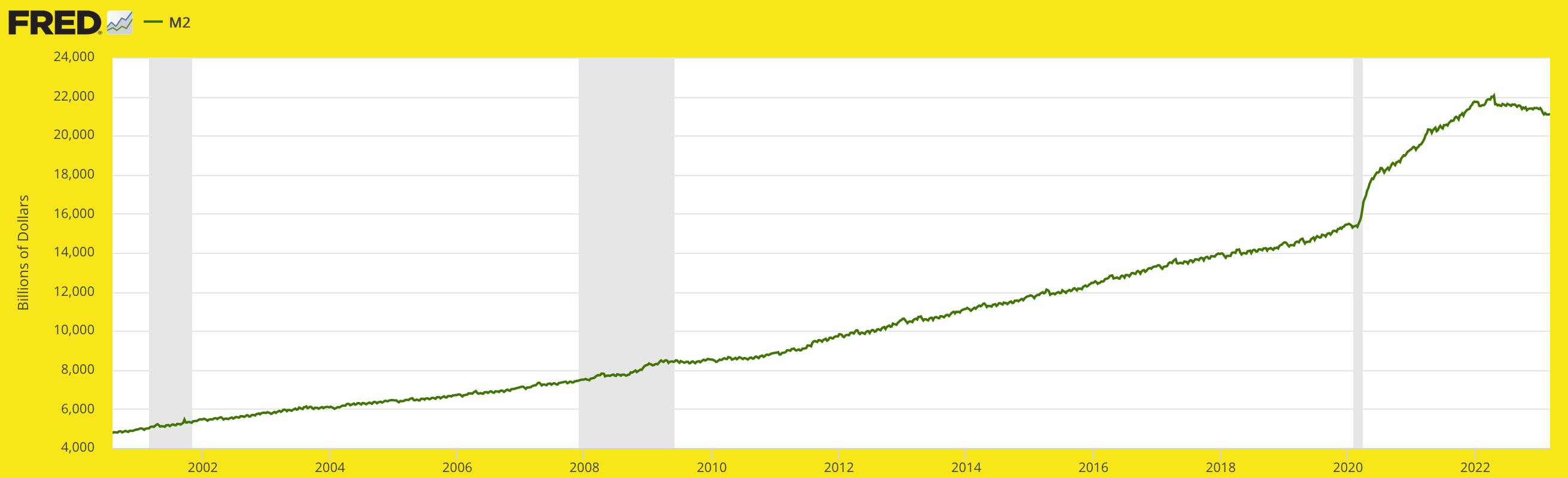

Finally, another concern related to the one directly above is the M2 money supply measure, which was blown way out of already inflated proportion in 2020 after decades of money supply abuse known as monetary (and where government has been involved, fiscal) policy. It is rolling over as YoY change tanks and even if it were to just drop back to the (inflationary) trend of the previous couple of decades it sure could feel like deflation while it adjusts.

Global Stock Markets

Global markets are largely going to be predicated on the US dollar to varying degrees. With many global markets, especially EM and Asia, ‘anti-dollar’ markets, they benefit when it is weak (like now) and will be at risk when it strengthens (like when the next global market liquidation takes place). We had an update on Thursday charting a few global ETFs in the face of the weaker dollar. These should generally work inverse the weak dollar for as long as it remains weak, but…

I have heard the term de-dollarization buzzing in the background lately, with the buzz getting louder. This is a cult. The “death of the dollar!” cult that has been exactly… WRONG for decades (since 2001 in my experience). It is in my opinion a fetish that some people just cannot or will not get over. As if China, Russia, the oil rich Middle East and others are any more capable of managing sound money than the US.

While I don’t think the USD has a preordained right to remain “King Dollar” to use TeeVee star Larry Kudlow’s old and annoying term, I believe that the sources of these de-dollarization stories that almost seem to revere China and Russia (an authoritarian communist regime and another one that pretends not to be) because of their combination of cheap labor and resource richness betray a bias. Usually pro-gold and/or pro-commodities and/or pro-inflation.

That said, as I watch a former president get indicted, creating another societal shit storm, a current president warmed over, propped up and supposedly doing whatever the people behind him are actually doing and shudder to think about what the next presidential election holds, maybe it is different this time. Maybe King Dollar is done for. But why don’t we wait for the test of the next liquidity crisis before jumping too quickly on that bandwagon? Eh?

As final side note to global markets, the Canadian TSX-V index is still firmly in bounce/rally mode and implies a still intact positive indication for the global inflation trades and anti-USD trades.

US Dollar/GSR & Currencies

USD continues to correct below the 50 day moving average after topping out below the SMA 200 and associated resistance. The Gold/Silver ratio is also dropping, which makes sense with the last update we reviewed on Silver’s stellar Commitments of Traders vs. gold’s mediocre one (we’ll update in the Precious Metals segment).

I’d expect the broad bear market rally to last about as long as these two riders of liquidity destruction continue to correct.

But referring back to the weekly chart, which I have not touched since the theoretical A-B-C rally was projected in a theoretical USD bear market, we find an A-B-C bear market rally projection still viable. So regardless of the USD bull/bear argument, we should be open to a new surge in USD should global market liquidity become an issue as expected in 2023.

Just for the sake of argument, if the USD is actually in a real bear market (I think it is in a cyclical bear at least) and given that the relief rally in stocks and commodities is very logically coming with a down leg in USD, does not a ‘C’ leg up go well with a projected end to the wider global rally and resumed bear market in cyclical items like stocks and commodities? Yes, it would go well with that. Again, I would tune out that de-dollarization crap until it proves out, maybe later in this USD bear if indeed it is more than just a small cycle.

Here is Uncle Buck’s rag tag bunch of paper competition. Not surprisingly, the Swissy/USD pair looks firm as it is the closest paper currency pair to the gold price. Switzerland has a reputation (still deserved or not) as being relatively sound, monetarily. The Euro has a firm ECB behind it and is firm relative to USD at least. The rest of these tramps are just trending which ever way they will against the global reserve Super Tramp. The blue SMA 50 is the intermediate trend indicator.

Finally, BTCUSD (weekly) is knocking on the door of the 30000 resistance zone target. While other speculations are rallying the world over, why not this one? As with the “de-dollarization” cult, I’d resist falling for any new Bitcoin promotions unless BTC takes out 32500 and holds it. But that’s just me, a non-believer. Or more to the point, a gold bug.*

* Unlike some ‘Twitter influencer’ bugs who hedged their bets by also becoming Bitcoin bugs (you know, near the BTC top). Got to at least hand it to Peter Schiff for not taking that promo but instead, participating in entertaining Twitter influencer wars about it. Clashes of the Titans, ha ha ha.

Precious Metals

Let’s use a different view of the gold and silver Commitments of Traders this week to show a spike in speculative buying and in open interest along with the commensurate ramp up in Commercial shorting. While this is not necessarily a rally killer (CoT is not a good timer, it is a condition) it is a picture of a coming gold price reaction, sooner or later. The trend toward briskly over-bullish may not be over and rallies ride those trends. But it should be kept on watch now as a warning as the gold price deals with what would be a much hyped 2000 level.

Silver is better from a CoT perspective, as it has been recently. But shorting by Commercials did engage as of March 28th and then silver spent three more days in rally mode. So it is safe to say this CoT view is also on its way to what will be the next caution point. Interestingly, as of this reading large Specs were not really engaged and open interest reflected that. It does not yet appear to be a picture of termination. But with the way week ended it has started in that direction.

Gold

Very simply it is lurking below what would be a much anticipated 2000 level resistance, which it is attempting to deal with for the third time. Resistance is often taken out on the 3rd or 4th tries as it theoretically weakens each time it is banged upon. Again, I gave my purest long-term fundamental views in Friday’s article. Let’s not belabor the thing. Gold is value for the very long-term and we have a technical target of 3000+.

Silver

This is the leader as the Silver/Gold ratio (ref. 3/29 update) continues to rise lately. The ratio will be a good adviser about when to become cautious not only on the precious metals, but the whole global shootin’ match, in my opinion. It could come sooner (it is the end of the Q4-Q1 time frame originally projected for the rally, after all) or later (silver’s CoT does not yet appear terminal).

So keeping an eye on the current short-term leader, we see the silver price lurking just below the next resistance level after it took out the daily chart’s SMA 50 and the key 22 area support it coincided with. While risk is increasing, I think silver is capable of breaking through resistance and it sure would be sweet if it could ding a new high above the 2022 high (27.50) before the next correction comes about. That could be an overbought level at which to prepare for a coming macro bear phase. Far from a prediction, but it is logical. That said, silver needs to take out the January high of 24.78 before any thoughts of 27.50.

HUI Gold Bugs Index

Likewise, it would be nice to see HUI tick a higher high above the January high of 267.35 before any thoughts of the 2022 highs come to the fore. On that note, however, the GDX chart we’ve been using for the last few months to guide us into and out of the January-March correction shows several upside gaps, the highest of which equates to around HUI 330. But that does not appear doable in the near-term unless gold stocks take a serious upside blow off that would probably need to be sold.

Regardless of that short-term noise making, the monthly chart will one day target 500 or higher if the view of a new bull leg is correct.

Fundamentally, a broad cyclical market liquidation and/or bear resumption would benefit the gold mining industry as gold’s value gets marked up in relation the cyclical stuff. The problem is that the inflation bugs tend to sell when their inflation trades start to fail. Classic baby out with the bathwater. So if that were to happen again, it could be the next big buying opportunity in what may well be a significant bull cycle out ahead.

I am not going to chart the miners now as the rally matures. I’d like to use gold, silver and especially HUI and GDX as guides for when people should either prepare for volatility/correction in whatever way they would. That could include holding/adding or if trading, profit taking and patient waiting for new opportunity. But I’ll simply note my holdings and watch items once again.

Meanwhile, looking at an internal indicator we’d like to see the HUI/Gold ratio continue upward to remain short-term constructive. As with the metals and miners, a rise above the January high would be a plus going forward as a ‘higher high’ marker.

Gold/Silver Stocks Held

Aside from Gold/Silver bullion fund CEF I hold in order of size AEM, MAI.V (MAIFF), BTG, SILV, ORLA, MAG, OGN.V (OGNRF) and OSI.V (OSIIF). My tendency in the past has been to do some profit taking in advance, but then wish I’d taken more when the inevitable correction comes and it inevitably bites harder than you’d think it would. Given the bull market view, however, I am not sure how I’ll handle it this time. A real bull market in the precious metals can leave you behind in a flash. I’ll plan to just evaluate the macro along the way. Hedging is a thing too. But that has to be timed right or else it becomes frustrating.

Gold/Silver Stocks on Watch

In no particular order, producers AGI, which I wish I’d never sold, HL, GOLD, KGC, NEM, SSRM, WDO.TO, EGO, even NGD if it ever gets its act back together, more speculative items like SKE, and perhaps a royalty or two (RGLD, FNV, WPM).

Commodities

CRB index is not bullish, despite the bounce/rally rationale we gave for it last week. It is bouncing and regardless of whether that stops here at the downtrending SMA 50 or sucks ’em in with the a continued bounce to the downtrending SMA 200, it will remain bearish until/unless it takes out the SMA 200, holds it and then proceeds upward to break the trends.

Crude Oil & NatGas: WTI Oil is also bouncing to test the underside of its SMA 50 and its status is very similar to its daddy, the CRB index. Gas probed a new low last week but retains an RSI positive divergence. It would not be surprising to see Gas bounce hard right into the ending phase of the broad rally. But that is conjecture at this point. I sold my one Energy stock, XOM, on the bounce.

Copper/Industrial Metals (GYX): I took my profit on copper miner FCX and rightly or wrongly am not buying the China reopening/China Growth stories because my gut says that a macro liquidation event would hit everything, supply/demand fundamentals or not. There are some smart people begging to differ though. It’s just that I am personally not buying in because I am a top down macro nerd, not a supply/demand fundamental commodity dork. Copper is still flagging but looks technically constructive while the greater metal complex (GYX) is a lesser version of that. It’s still weakly bouncing but is in danger of turning the intermediate trend back down.

Uranium: I took NXE as a long after last week’s Commodities segment that was open to a bounce. It and the sector (URNM) are in ‘W’ bounce patterns and I am going to give it exactly as long as it does not ruin those patterns. But if the inflation trades are only on a bounce, so too likely is the u3o8 segment. However, as with the likes of Copper, Lithium, REE, etc. there are longer-term supply/demand positives out on the horizon unless the world just stops.

Lithium, REE, Nickel, Palladium & Platinum: I took a position in Lithium producer ALB on spec, but am watch what is potentially a bear flag. The second that breaks down I’ll dump it. The other usual Li watch list stock is LTHM, currently not of interest. The Li price continues to tank. Fellow battery material Ni is still thinking about a bounce and I am keeping a casual eye on TLO.TO (TLOFF) as usual, after it dropped to test long-term resistance. Still holding strategic REE play MP for a would-be bounce. Pd is attempting to muster a bounce within its firm intermediate and long-term downtrends and Pt is actually constructive above its daily SMA 50 and SMA 200 and attempting a trend change. The watch item there is SBSW, which is still beaten down but could bounce if the PGMs do. SBSW also has Lithium and Gold components to its business.

Agricultural (GKX): Well there is a decent bounce… right to the downtrending SMA 200. Still no personal interest, but at least the Ags have joined the commodity bounce-a-thon.

Commodities can continue to bounce if the broad global rally does, especially if the rally does not reacquire its Goldilocks/Tech flavor, which it started to show signs of once again last week. But if a broad market liquidation is out ahead, it is best to tune out commodity perma-touts because the top down macro would pressure everything. Now, I may not be right about what is ahead, but I am pretty sure I’d be right if the deflationary macro view – even interim to the next inflationary phase – comes about.

Portfolios

Savings balanced by gold.

Trading Account: no positions

Roth IRA (non-taxable, no contributions)

Cash equivalents now includes the 3-7 year Treasury bond fund in alignment with the disinflationary macro view. Cash and equivalents at 82% is lower than I want it to be as the broad rally matures. I sense some more profit taking or loss limiting upcoming. So why did I add TSM at week’s end? With the symbolic end of the projected Q4-Q1 rally I want to pay attention now because I want to be the strongest damn market player I can be when the FOMO herds do get run.

Meanwhile, here is what I hold in order of position size.

Cash & income-paying Equivalents are at levels that are right for me and my real-world situation. Your situation is different. Cash will be adjusted as needed.

Refer to the Trade Log under the NFTRH Premium menu at nftrh.com for trade info, if interested (not that you necessarily should be). Also, you can follow at Twitter @NFTRHgt for notice of updates.

NFTRH is not to be distributed to third parties without prior written consent

Notes From the Rabbit Hole (NFTRH) is a weekly market report in which we provide analysis on financial markets. We make every effort to provide accurate and high quality content, but this analysis ultimately represents our opinions and these opinions are provided without warranty or guarantee of any kind. See full terms & conditions of service under the ‘About’ heading in the main menu.

Confused. “sentiment was constructive for a continued rally with the Bull/Bear ratio at .5″….I thought a number less than one was bearish?

Hi Lenny, the AAII Bull/Bear ratio never gets to zero and .5 is the lower bound of extreme over bearishness. An extreme over-bullish reading would be 3 to 4.

Hi Gary, I was reading a blog post https://michaelwgreen.substack.com/p/giving-credit-when-credit-is-due and this line was surprising to me: “Credit is showing signs of deterioration. Lower quality high yield, Caa and below, is seeing spreads versus Baa inline with the 2008 Bear Stearns takeover”. Chart is in the post. This is in contrast with BofA HY chart you (and me) are using. Not sure of importance, but thought it’s worth sharing

That guy is a serious macro nerd! I love it. I am going to link his Substack on the links page. Maybe his bond inputs are more sensitive that what the St. Louis Fed provides. But our HY spread is elevated and only on a small curve down. So it’s not exactly predicting calm waters. The next upturn could be the back breaker.