The theme for a bear case has been to take back the Trump rally in 2019, using SPX 2100-2200 as an example.

Very simply, that would take SPX down to the massive support area that launched the Trump rally after the US election in late 2016.

Now, consider that an H&S top could be taking place. With the over bearish sentiment that whipped up, the holiday seasonal into ‘January effect’ season (as post-tax loss buying theoretically kicks in) and the Fed whispering sweet nothings in the market’s ear, who knows what bull stories could get cooked up to raise the market to a right side shoulder?

If an H&S scenario does come about it could be several weeks (even a couple of months) of grinding higher. It took much of the winter and spring to grind down from the January price and sentiment high (left shoulder) after all. Now, the good part is that if (and it’s all just theoretical above the dashed neckline) this is an H&S, it’s measurement is right down to the big support area, just above 2200. I love confluence.

So consider that if things stay bullish after the Powell jawbone, they could stay bullish into January or even February. After all, to make a proper right shoulder people will have to gather their courage and maybe even overconfidence back again. If daily charts start to indicate further upside above the 200 and 50 day moving averages, I’ll probably cover shorts and ride long and cash for a while.

Now, a big part of the original Trump rally was supposed to be reflation, which would pressure the US dollar, raise commodities and materials and with rising interest rates, Financials. These were the media headlines of the time just after the election. Well, things have not really worked out that way.

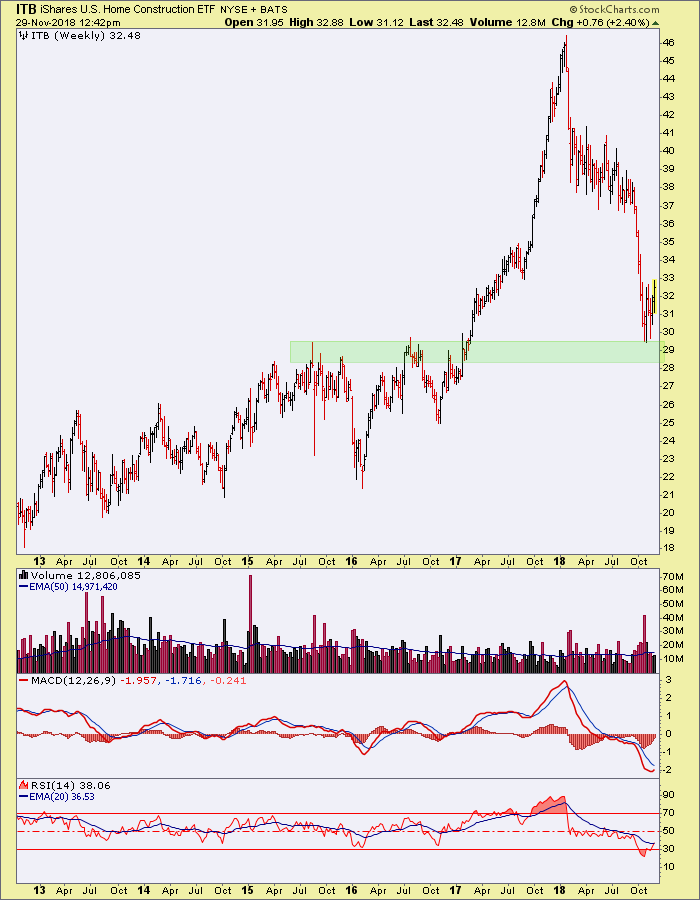

Sure, Housing took the big hit as might be expected with the rise in long-term yields. ITB (and HGX) took back the Trump rally.

But so too now have Materials. At least XLB took back the majority of it before reversing recently.

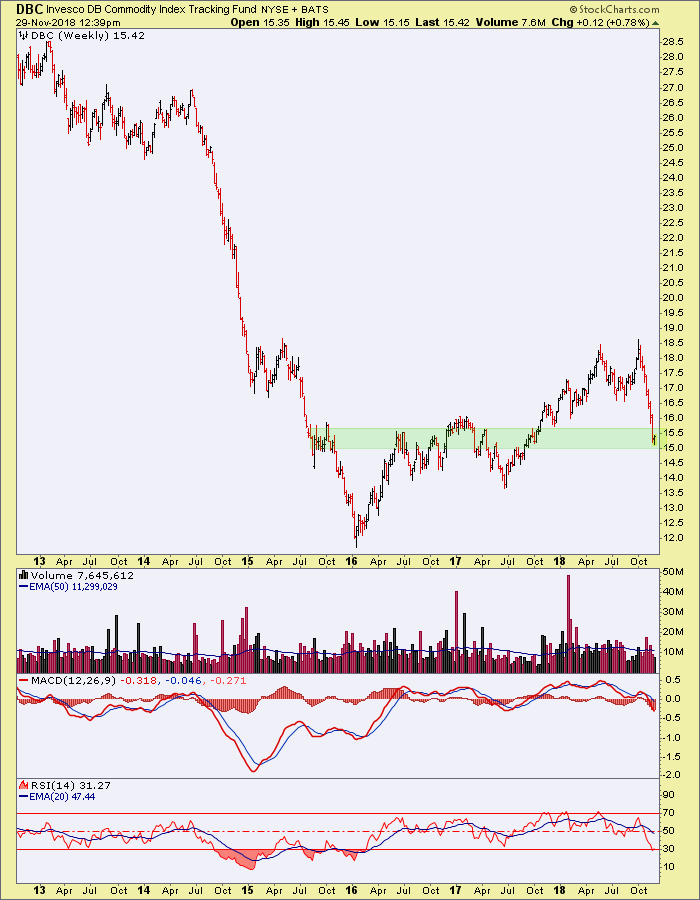

And Commodities gave it all back.

So my point is that it is very possible that the most oversold sectors can rally (these and many other sectors are bearish, but probably due for a bounce) and possibly rally hard. All while the SPX makes its theoretical right shoulder to an ultimately bearish H&S top. Voila! There’s our 2019 bearish projection to 2100-2200.

No man staring at charts is doing more than hypothesizing and trying to scout probabilities. But when I took at look at these sectors and consider SPX, a theme came forward. Let me know if you have any questions or even better, contrasting or enhancing views. A near-term bullish but 2019 bearish market view fits well with the above. It also makes sense with the recent sentiment washout.

What might this mean for the gold sector? It could mark and bide time during the making of a right shoulder, preparing to get bullish when it fails (again, we’re theorizing here) or it could take a final dump if bullish risk ‘on’ spirits are sufficiently renewed.

We’ll develop the whole ball of wax moving forward. Again, I am just putting forward a scenario that makes sense to me from a few different angles.