As the dust settles I want to make a few notes about the last week and about where markets stand as of now. Our general picture has been that the US stock market was bullish but in a high risk sentiment posture as well as overbought on Trump mania, or whatever you’d call it (whatever it was, it was an excuse for market operators to whipsaw the masses and ram a rally into gear post-election). In my opinion, the follow-on momentum came in the form of non-professionals, i.e. Ma and Pa entering the market after being highly suspect of it during the Obama years.

That appears to be getting addressed now to either a small or larger degree. The market needed a speed bump at least. I continue to question whether this is the end of the bull (with a classic, post-hype throw over and 2nd thrust in breadth and momentum in 4 months) or a fuel stop. We’ll figure it out soon enough by gauging it along the way.

- The first important issue that came in over the last week, at least as relates to our normal operations in NFTRH analysis, was the establishment of a 3 month downtrend in the SEMI bookings reading. I see it as a cyclical warning. This was hidden from general view.

- Then came the OPEC drama, which really got the front page news treatment as media large and small alike fell all over themselves to report the news. It’s the reason I suspect the burst upward in oil and the energy sector, because the technicals in the energy sector are looking good. I just do not think that a group of price manipulators who have had a checkered past coming to an agreement on price fixing is a good, enduring fundamental.

- On a related matter, I want to address the gold miners since a subscriber noted that I have not mentioned the OPEC news as it relates to a bullish Oil-Gold ratio. My answer to him was that I made an assumption that people know my stance, since it has not changed. This fundamental for gold mining was bad to begin with, and got worse insofar as oil has bulled on OPEC. In essence, gold mining cost inputs like energy (and materials) have been rising while their product’s price has been declining. Not a good underpinning to the fundamentals. More on this at the end of the update.

- Today ISM came in pretty good. It expanded to a PMI of 53.2. New orders were good but not eye popping, prices were flat. The big gain was in Supplier Deliveries, which is virtually meaningless for the purposes of economic signaling.

- ISM above is a laggard, as is Non-Farm Payrolls tomorrow. The market expects +200,000, up from the previous +161,000. That sounds doable. The media love to make a lot of noise around this report but we already know the odds of a rate hike are extremely high, the dollar is massively bullish, Treasury bonds massively bearish and well, you get the picture…

How much is cooked in to the macro backdrop that markets must decipher?

On the gold sector, which we highlighted as “in the mirror”, along with T bonds, Yen and other things that are extremely bearish since the election (actually, it was all bearish well before the election, as you recall) any bounce will not have fundamentals at its back; at least not fully formed fundamentals, until the stock market tops out for real and fear reenters the investment realm.

Gold has been crushed in relation to most asset markets, including several commodities. But let’s take a look at Gold vs. Stock Markets, which has been drubbed across the board. It has broken down vs. all major stock markets. But at this time last year it was completely broken as well. That’s the thing about charts; unbroken ones can break and broken ones can get unbroken. Hence, TA is a bunch of hogwash. Not really, but you see the point. Flexibility… charts do not control markets; it’s the other way around.

A final note about the gold sector, because I take very seriously the act of writing about the market for you and do not want to leave things open to misinterpretation (so please ask, if unclear on something)…

From the earlier update…

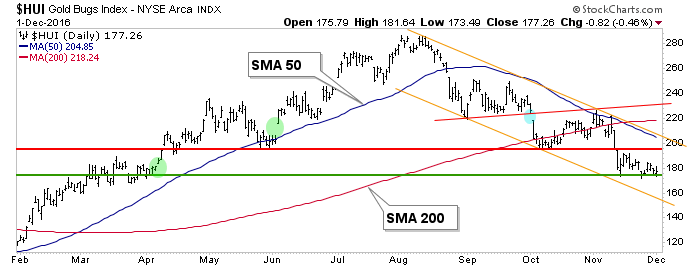

“Now, pertaining to the gold sector, if there is to be a bounce we should keep in mind that the HUI has maybe 40 points upside within the ‘bounce’ parameter before it can change the daily trend to up.”

I want to be clear that I am not saying HUI will bounce 40 points (assuming a bounce even occurs). I am saying that there are 40 points of upside to around 220, before it can even think of changing the downtrend to up. More realistically, if said bounce occurs (and how long have I been writing that?), the 200 area would be the objective. The reason I take it more seriously now is because of the weakness creeping into the stock market’s leadership areas and because of the despair now starting to paint the sector’s sentiment profile. [edit] But as the chart shows, a swoosh down to the channel’s bottom cannot be ruled out before a bounce attempt either.