This week has been a gamble. If you’re a stock bull you lose, if you’re a gold bull, you win. This morning’s reaction to Britain’s exit from the EU is pure casino stuff, practically speaking as an investor in the very short-term.

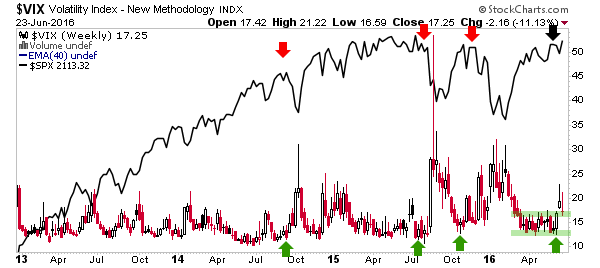

From Tuesday’s update (with an updated chart of the VIX)…

“If I could sum it up in one chart I’d say let’s consider the VIX. A big pop in volatility is now being ameliorated as peoples’ nerves ease. VIX is settling back to the support zone. This is a week that will make a lot of headlines and with VIX at or above the support line, we should be open to resumed volatility and the potential of negative market events. If it breaks down, we can get further-still toward a bull stance.”

“We are looking ahead to a potentially bullish (if inflationary) phase but this is just a reminder for moderation and caution in the very short-term on the broad markets. The best time to buy is amid fear and angst.”

It may not seem like it at the moment, but the Brexit vote is an important step in the direction of a would-be inflationary future, although it probably pushes its timeline out. What do we suppose will be policy makers’ default stance now? Full on DOVE would be my guess. If the US market comes under threat, we’ll see how serious Yellen is about her assertion that the Fed does not consider the stock market in its policy setting actions (and non actions).

For my part, I took a few positions (including AMAT, LRCX and TEI from ‘+’ updates) and plan to not get shaken out of them based on today’s hysterics. As for the caution advised above, since I was somewhat exposed to the market, I decided to add some leveraged index shorts (SPXS and SQQQ to go with the already held short against SPY) on yesterday’s big rally on exit polls’ supposed Bremain lead. That was a gamble, but this casino patron for one, didn’t believe in the validity of the exit polling.

Along with this, precious metals positions were all held (well aware that the bullion position acts as a behind the scenes risk manager, AKA insurance). Make no mistake gold fans, if they had Bremained gold could have lost 60 bucks an ounce, as opposed to this morning’s +60.

So where do we stand? Little has changed. Europe was bearish despite the euphoria this week, and it is still bearish. I am holding India and other items that I thought were bullish before Brexit and plan to do so until/unless charts break down, pending a settling of emotions in the immediate-term.

But if/when the hedges are dropped I will have less tolerance with long positions because while there are fundamental reasons to be bullish certain areas, I try not to subject myself to the whims of emotional momentum players, whether they are momo’ing to the upside or the downside.

The gold sector’s fundamentals, as noted in NFTRH 400, were good before and I will say they are better now because of what this will do to gold’s ratio to stock markets and also due to the pressure on policy makers to continue to try to inflate/reflate.

As for the metals, gold’s probe above 1308 last week was indeed a bullish “scout”. As a side note, gold is up 5.16% to silver’s 3.73% this morning, so we have no breakout on the silver-gold ratio. This makes sense, given the global angst.

The miners are probing new high territory in pre-market. The next target is and has been HUI 251. In Wednesday’s precious metals update we noted how all items were stable, with gold and silver stocks remaining in up trends. We also noted…

“Of course it is T-minus less than a day on the Brexit/Bremain announcement so everything can be taken with the grain of salt of this unpredictable outcome. But I wanted to get you a mid-week technical look at the PM sector none the less.”

Bottom Line

This is a whopper of an inflammatory event. I often go on about how these media items need to be tuned out. But this one is different because it is fundamental and it is also indicative of a waning of confidence in centralized monetary authorities, which you may recall was our bedrock theme for a new gold bull market. We began talking about this nearly a year ago with the macrocosm theme, with ‘confidence declines’ being one of the major planets (it, along with yield spreads rise should actually be larger planets but work with me here).

‘But Gary, you have been waving your pom poms about the semi equipment sector lately and I see a big planet right there called ‘Economic Contraction!’

Well yes of course. Backward looking econ data are indeed tepid at best. Semi book-to-bill is a forward looker. It took months from the Jan. 2013 signal before manufacturing, payrolls, etc. eventually firmed. Again, what happened in Britain is another lever pulling for inflation, but it is deflationary or contraction environments that create inflation. The gold sector is the first to pick up on that.

If we are correct to expect an inflationary phase, the blueprint is the Greenspan era. Gold bottomed, gold miners bottomed and they turned up leading silver’s upturn, commodities and eventually stock markets during a phase of ‘inflationary growth’. If the signal in Semi Equipment is wrong I will bow to the experts and admit I was wrong. Until then, Brexit is not going to change the current ongoing themes. In fact, it could be looked back upon as enhancing them in time. None of this however, is sustainable. For reference, when the Greenspan inflation cycle ended it crashed. Whether this cycle ends sooner or later, I see no reason the same fate is not in store. I just don’t think last night’s event in and of itself has much to do with it.

More to come after today’s fallout in NFTRH 401.