Summary

- US Stock Market: Small (i.e. short-term) double tops in SPX and NDX? I shorted based on the daily chart technicals. But the larger rally is completely intact. Ultimate target is 4800 (SPX) with a potential for a ‘suck every last one of ’em in’ throw over to new highs.

- Indicators: Per last week… Indicators are reflective of the risk ‘on’, bullish atmosphere. High yield spreads, Libor/T-bill, Equity Put/Call, SPX A/D line, etc. are supportive. One ongoing bearish signal is SPX Equal Weight negative divergence. See below. Indicators show bull sentiment in effect with few immediate disturbing signs other than the Put/Call. That can turn on a dime. NEW: watching yield curves for potential steepening after the 10/2 tested its previous deep inversion. Also, SPX A/D line dropped harder than SPX pulled back last week and bears watching.

- Market Sentiment (US): Per last week… Brutally over-bullish now. Generally now near the degree of its opposite over-bearish condition last October. Sentiment is a condition for a market top and it is in place now. It is not a timer, however, as it is a reflection of what is going on (full bore momentum and fear of missing out). NEW: Sentiment only starting to get dinged and if a correction were to follow, sentiment is not standing in the way and has a long way to go before it would.

- Global Markets: Global rallies intact. Most pulled back last week, however. Watching German DAX as a potential guide. If it is double topping it could be a global warning, on developed markets at least. Up north of here, the Canadian TSX-V continues to creep support and that keeps on open prospects of inflation trades.

- Precious Metals: Per last week… It is possible that the precious metals complex is ending its correction now, but that is not yet technically indicated. The best feature is silver thus far successfully testing its SMA 200. The sector can rally at any time, but the best, clearest low risk downside objectives are lower and still open. See segment for more detail. NEW: PMs would likely rally along with inflation trades if USD breaks down. With a majority of the planned for correction in the books, so much the better.

- Commodities: Still mainly trending down. When viewing CRB and Oil, it’s a long, downward consolidation ‘handle’ that could break upward at any time… if USD breaks down and signals inflation trades. Personal special interests in outliers like Uranium, Lithium, REE.

- Currencies: As usual we watch USD and its liquidity destructive companion, the Gold/Silver Ratio. USD daily chart technicals are not good, but as yet no breakdown. If that happens, there’s a long way for the buck to potentially decline within its long-term bull market (2008), triggering global anti-USD trades. But if the Fed succeeds in breaking something, all bets go off.

- Bottom Line: We are playing a high risk and potentially high reward game with respect to speculating upon whether USD will break down in line with its degrading daily chart technicals.

US Stock Market; Short for a Trade (“how dare you?”)

A simple and humorous response to a tweet I made about shorting QQQ: “How dare you?”. It’s sad but true. My estimate is that well over 90% of the time shorting this pig is futile or worse, dangerous to your financial health. It’s been a decades long bubble after all, interrupted in 2000, 2008 and to lesser degrees 2020 and 2022. Stocks, especially large cap well known stocks of powerful companies, are ordained to go up (only).

With our potential upside target on SPX at 4800 or even a throw over to new highs and with the indexes 100% technically intact to their rallies, this can only be a trade.

Within that bullish framework, the US market is questionable. I decided to take short positions on that questionable situation. Beginning with NDX and per the trade log, I shorted QQQ due to a potential for a short-term double top. Meaning a pullback within the technically intact rally, not a new bear market. Of course that could develop, but as you probably know, I don’t get ahead of the technicals. But when I saw NDX/QQQ bounce to fill Thursday’s gap down it looked like a setup.

A routine pullback could test the SMA 50 (blue, 14179 and rising). A difficult summer could bring NDX to the gap at 13986, and if it does that, why not test clear support at 13200? It’s a plan, anyway. A plan I’ll manage risk on if it goes the other way and takes out the little double top as indicated by the red dashed line. There is clear resistance in the 15493 area, however. So depending on my tolerance at such time, that may be used as the tolerance point. But the original intent is that the Friday bounce and gap fill is a short-term kiss goodbye.

The rally was built on big Tech leadership like the good old days. Man, machine and casino patron alike buy Apple, Microsoft, Nvidia, etc. and it’s all gonna be just peachy. That’s the simple playbook, isn’t it? Buy what everyone knows are the US market’s true king pins? As you may recall, I’ve been long each of those stocks, especially Mister Softee in the past. But it was just time, here in deep summer, to take a shot from the short side.

I used SPXS to short SPX. Unlike NDX, it ticked a higher short-term high on the potential small double top. Can I get a gap fill at 4232? Pretty please? And while you’re at it, could you bang clear support at 4160?

Both daily charts show suspect RSI and down-triggered MACD. Worth a shot.

As a side note, in my view it would actually be healthier and more big picture bullish for these indexes to drop now and fill those gaps. If they were to do so and resume upward I’d increase the odds that maybe the bull rally is real and not an epic bear market suck-in. If I lose on my short positions and the gaps are left unfilled, ironically, it would increase my bearishness on the bigger picture.

US Stock Market Sentiment

Smart & dumb money indicators have taken a turn but are still no friend of stock market bulls, contrary speaking. Bonds, which continue to take seriously every hawkish utterance out of the Fed’s orifice and every positive tick in lagging/backward looking employment and GDP, are very much hated and stocks are just starting to turn down from very much loved. The signaling from a contrary sentiment standpoint is positive for risk ‘off’ and counter-cyclical and negative for risk ‘on’ and cyclical.

Incidentally, when we think about the possibility of a temporary inflation trade, it would likely be due to the continued fading in inflation signals and thus a fading in Fed hawk fears. In other words, it is conceivable that a good bounce in commodities could come in tandem with a bond market rally. Gold, oil and Ags are all decent, contrary sentiment wise.

Moving on, Newsletter sentiment was getting toward dangerously over-bullish on July 4, just as the market was making what I hope (bad word) was a short-term double top. That’s the kind of spike we want to see in order to be bearish on a contrarian basis. Newsletters and AAII tend to be more ‘sticky’ than the twitchy likes of NAAIM and Dumb Money.

Speaking of which, Ma & Pa also spiked. I think Ma’s constant reminders that they need a new roof and interior and exterior paint for the house finally sprung Pa into action. He couldn’t take it anymore and now he’s in da house! Contrary bearish.

NAAIM (investment managers) were actually relatively grounded as the players above lurched bullish. Certainly not contrary bullish, but showing some level of professionalism in an over-bullish market. Bravo.

Sentiment Bottom Line

On the whole, US market sentiment was fully ripe for a decent correction at the potential short-term double tops noted in the opening segment.

Global Stock Markets (weekly charts)

Please take due note that local currencies play a role in market performance for global citizens. NFTRH being American, cannot get too far afield managing all those moving parts with my simple charts. So global market comments and charts are for reference.

The global views are little changed from the last two weeks. World (ex-US) has flattened out within its rally uptrend, as has Europe (2nd chart below).

As a side note on Europe, when I look at the German DAX (European leader) I see a potential double top. Except that unlike the US indexes, this double top could be a major one. DAX is starting to do what Jordan and I speculated could be possible for SPX in the Podcast we did last week. A slight ‘suck ’em in’ tick to new all-time highs before a hard turn down. This could just be a shakeout prior to a resumed bull, but RSI and MACD do not seem to agree. Regardless, DAX bears watching as a potential forward guide (bearish or bullish) for other developed markets.

Great Britain continues to poke bearish as the inflation, and I assume hawkish headlines, fire up over there. Canada’s TSX is not much better, waffling along sideways, as is Australia. If (and it’s still just a theory) relief comes to the inflation trades sooner or later, these commodity/resources based economies could see their markets do better, relatively. But it’s not yet time to bet heavily on that or invest, in my opinion. If USD breaks down (see Currencies segment), that could trigger a big global inflation trade.

Japan’s Nikkei continues to consolidate its bull market. This is not far from the 35000 target we measured several years ago on Nikkei’s long-term base and breakout. In other words, risk/reward may not be nearly as bullish as the 2023 price action has implied. We’ll see. I’ll stay open minded on it.

Hong Kong (and much of Asia) continues to under-perform along with China and much of Asia and EM. They would likely get a relative improvement similar to Canada and Australia, if an anti-USD inflation trade were to manifest. But again, that is speculation at this time.

India is blue sky flying. Simply bullish. Yet I denied my greed and took a nice profit on RDY as I reeled in positions in favor of cash raising last week.

Speaking of speculation, Canada Junior is still on its slithering routine at important support. Not bullish, but not broken down either. As long as that is the case, a support for a would-be future inflation trade is also the case.

Brazil is another inflation trade indicator, as it is a resource rich EM. It held support at 100k and is testing minor resistance at 120.8k. A daily chart (not shown) does look double toppy, however. Argentina’s bubble halted for a few seconds.

Mexico is in blue sky and has been among the best looking global markets I’ve seen in 2023. Africa ETF remains just plain bearish and the Frontier ETF continues to bounce after a support hold.

Precious Metals

A look at the important relational view of gold to risk ‘on’ and cyclical markets (daily chart) shows that the fundamental vs. the US stock market took a beating with the recent up surge in stocks, while the view vs. global stocks continues to consolidate above the previous low.

Gold/CRB index is is still in a normal consolidation within an uptrend and that is not a positive for the prospect of an interim inflation trade. In other words, gold should lag in an inflation trade and it has already lagged since May. Either this ratio likely breaks down or the inflation trade, such as it is, is already happening.

Gold/Oil is fading within an existing intermediate uptrend. Very important for gold mining cost structures for this ratio not to break down.

Gold/Copper ratio shows the counter-cyclical metal still in consolidation vs. the very cyclical metal. It would be best for the case of favoring the precious metals if this ratio holds its SMA 50.

Gold and silver Commitments of Traders (CoT) went nowhere last week, although let’s note that the open interest in the would-be leader, silver, is low. All in all, still a risky picture. But only moderately so. Other indicators:

- ‘Real’ 10yr yield is very elevated once again and gold-bearish.

- High Yield credit spreads are very depressed and hence, macro-bullish and gold-bearish.

- M2 money supply continues to roll over and that is macro-bearish but also gold-bearish (until it brings on a future Fed panic).

- Nominal Treasury yields and inflation expectations bumped up last week and that is gold-bearish. I happen to believe it is b/s with respect to rising inflation on the near-term, but we are going to abide by the indicators.

- The 10-2 Yield Curve remains very inverted but we are on watch for the prospect of a new steepener after a secondary deep inversion that corrected the ‘banking crisis’ paper-over. If it is a secondary flattener/inverter and if it has halted and turned up… then macro stress (of inflationary or deflationary pressure) would be indicated. Either would likely be positive for gold, but the gold miners would prefer deflationary pressure, fundamentally. Technically, they’d be due for a rally as the inflation bugs carry the day under inflationary steepening.

But before talk of a rally, the miners need to hold above the March lows and turn up. That has not yet happened, although GDX (daily chart) is grappling with the now up-sloping SMA 200. I am remaining mindful of the sub-28 gap and thus continued to hold the DUST hedge.

Assuming the miners will hold the March lows, so much technical risk has already been bled out of the sector from the overbought highs of the spring. But bugs want to see those funda to stop consolidating/breaking down, hold and turn up again. Technical is technical and fundamental is fundamental. Two different things, sometimes at odds.

Silver is declining in what could be interpreted as a bullish falling wedge. The upside touch point last week could be the 4th of 5 touch points with the lower and perhaps final decline still to come. In other words the hold of the daily SMA 200 so far could be a small bear flag (with the wedge potentially a large bull flag). If silver breaks the upper line let’s scrap that plan for a more bullish alternative, short-term. Meanwhile, as with GDX/HUI we are simply looking for a higher low to March and a test of the shaded basing pattern as worst case, assuming the macro view holds up for the PMs.

Gold (daily) continues to flounder in no man’s land below clear resistance and above clear support. It’s got minor support here but I’d continue to prefer a test of the SMA 200, at least. We shall see.

Gold (monthly, linear scale) reminds us of the bullish big picture.

Gold (monthly, log scale) even more so. “Patience”, asks the monetary metallic holder of long-term value.

Precious Metals Bottom Line

All in all, the precious metals complex has been doing what it should be doing during a speculative relief (FOMO>MOMO) phase like we’ve seen in the stock market. Bugs who get frustrated that gold is not going up are shoveling that excrement against the tide. Using the extreme bearish indicators (real yield, yield curve, etc.) as a measure, risk/reward is very positive, by definition. But if you’re all in due to incorrect fundamental assumptions – like inflation – it does not feel positive.

Joy elsewhere, whether at the behest of inflation (circa 2020-2022) or disinflationary Goldilocks (2023), is no time to be cheering gold or gold stocks. When the high risk macro changes, it will be time to get very bullish on the gold mining sector (I am always positive on gold as a value/insurance instrument), whether they are due to rally or first get slammed in sympathy to the cracking macro. It’s so simple that the confusion introduced elsewhere makes it seem complex. Gold is fine. Always is.

Commodities

So, is this moderation of the downtrends in items like the CRB index and crude oil the inflation trade? Could be, say the Gold/CRB, Gold/Oil and Gold/Copper ratios on the chart above. And the nominal technical views continue not to impress.

CRB: Trending down and bouncing within that downtrend.

WTI Oil: Trending down and bouncing within that downtrend. Side note: Seasonal is positive as is CoT alignment.

NatGas: Actually in a modest uptrend since April as it tries to escape a basing pattern. This is probably the old line commodity I am most interested in at this time. Hence, the Energy sector is one I am thinking long and hard about before selling out of (NOG & AR), also considering oils seasonal and CoT.

Copper/Industrial Metals (GYX): Copper is perched below the moving averages, which have death crossed the daily SMA 50 below the SMA 200 (which probably means a rally is in the offing because death and golden crosses are the greatest canards in TA). GYX death crossed in May, made the obligatory post-cross rally and is now trending down and bearish.

Uranium: The sector (URNM) is neutral with a bear bias, technically. Yet its leader, CCJ is doing this potentially bullish thing on the weekly view. Not only did I continue to hold CCJ, I added more on its pullback. But lose 28 and all bets go off. Generally, I am neutral on the U sector at this time.

Lithium, REE, Palladium & Platinum: Li price is going sideways after bouncing from the 2017 highs (support). LTHM and ALB continue to bounce constructively. ALB is dealing with its downsloping daily SMA 200, but LTHM did that previously and took it out. So for now it’s an intact intermediate rally. I have a casual eye on them.

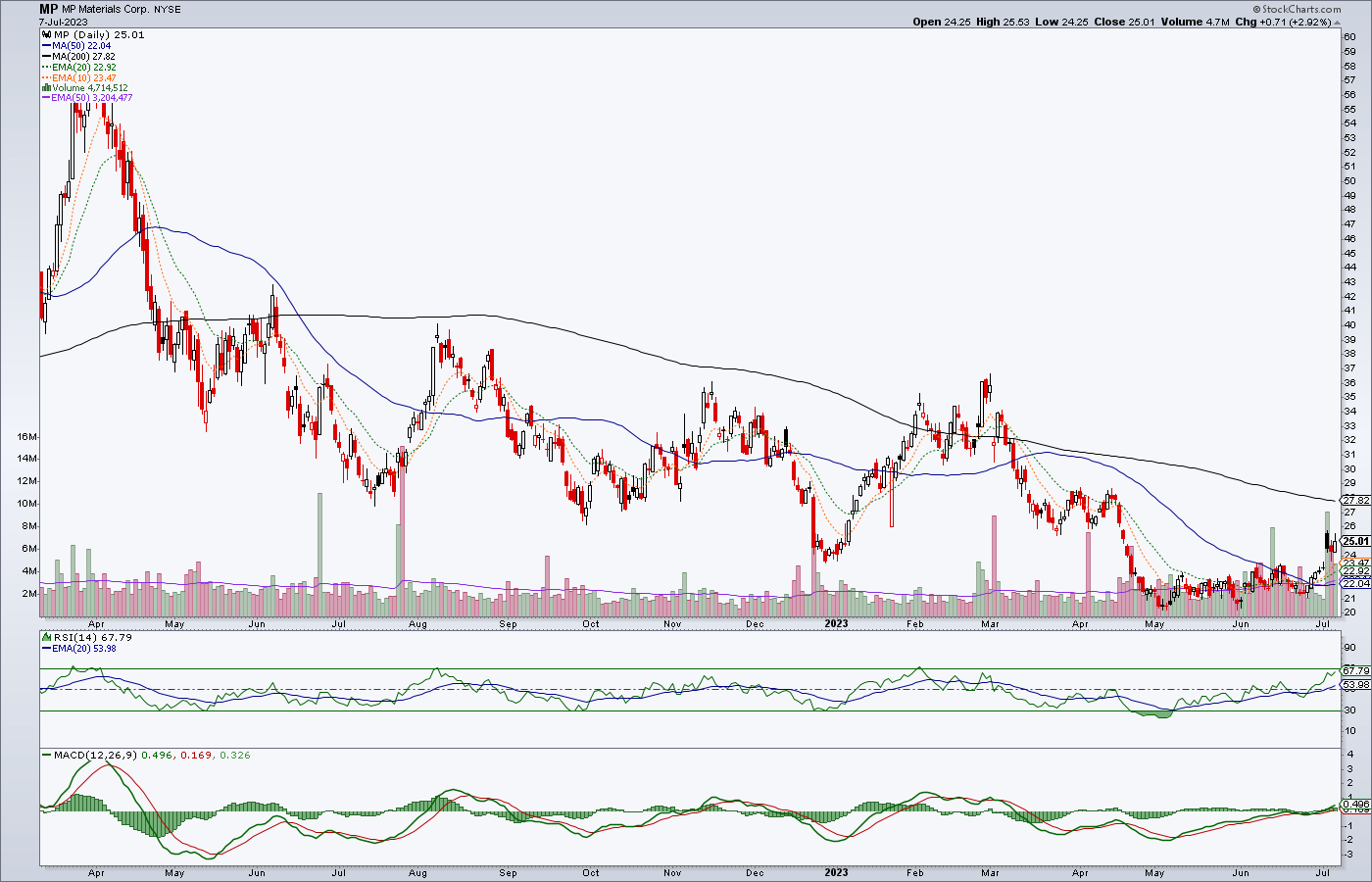

As for Rare Earths, there was some China hype last week that drove up the price of current holding, MP because China is threatening to curtail shipments of REE to the US. That is the very crux of why I’ve been watching and mentioning MP all these months. But from what I’ve read, MP still needs China to process its REE, and I am not sure how that figures into the equation. For now, the launch off the lows is appreciated but the major trend (daily chart) is obviously still down.

We noted Palladium’s positive CoT data last week but also its proximity 13% above clear support. So it’s mildly on watch, perhaps for a future more substantial inflationary phase. Platinum continues to try to bottom after ticking a slight lower low to the March low. Sometimes they do that to shake ’em out with a bear trap (a fact not lost on me with respect to the precious metals miners and the long watched March low, as well).

Agricultural (GKX): The index is pinging new lows in its downtrend while the ETF (DBA) is on a sharp pullback within its 2023 uptrend. Internal weightings of individual commodities obviously are at play here. I am keeping an eye on the sector, mainly with the related fertilizer stocks, NTR and MOS. For now, sidelines.

Currencies

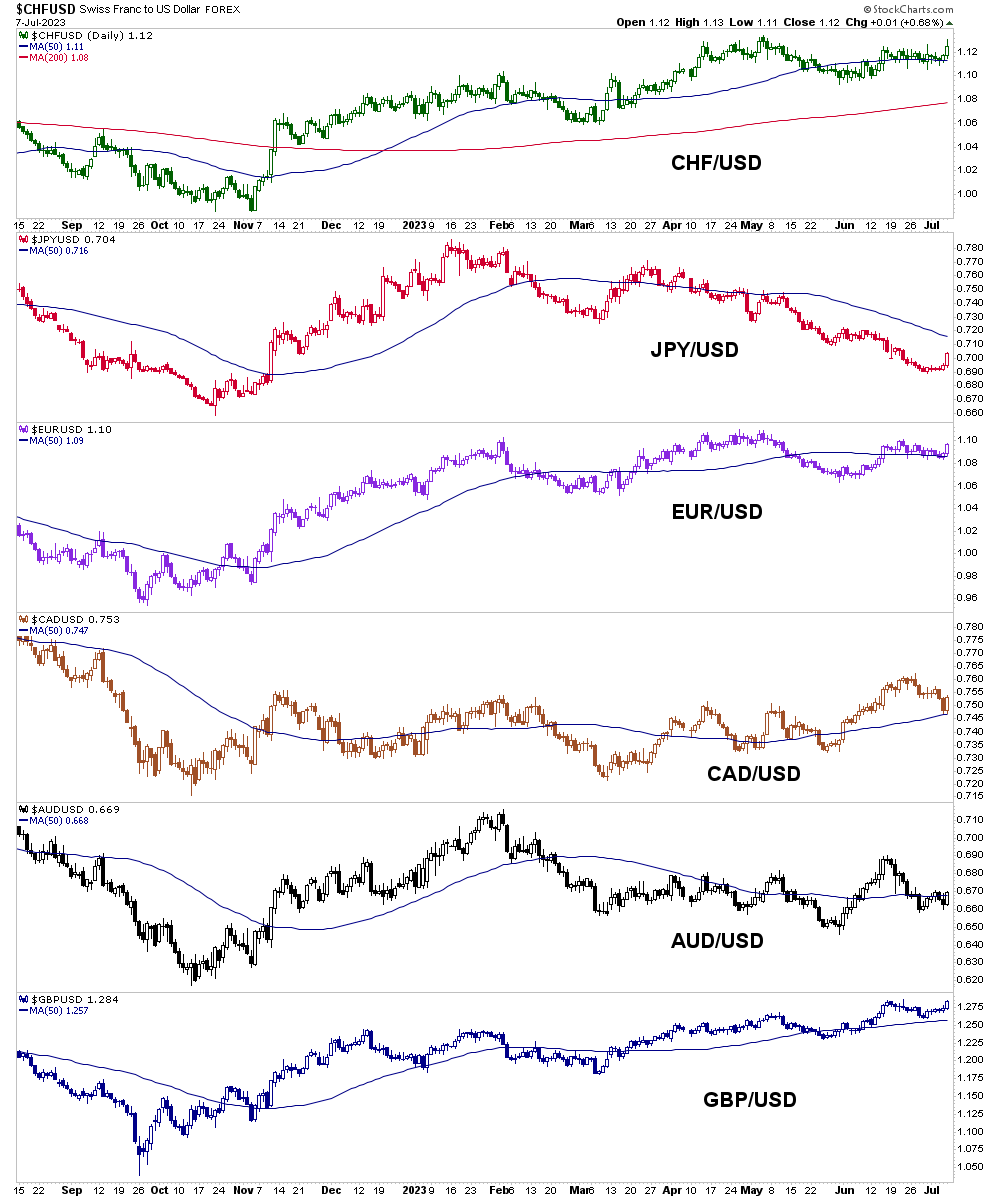

USD down, world of assets up on Friday. The buck (daily chart) bonked the first resistance level and fell below the SMA 50. The SMA 200 is sloping down and that is not technically a good thing. The history is a death cross in January and the obligatory hard move in the opposite of its implied direction in February-March. A tick to a lower low, a bounce to a lower high and now here we are. Frankly, the daily chart technicals are not good for USD.

Our thesis has been that despite the poor technicals, a rally can come about at any time if the markets liquidate. The Fed is trying to trigger that, but so far no dice. The market is flipping them and the buck the bird. Gold/Silver ratio (GSR) is a liquidity indicator and like other macro indicators noted above and all along these many months of the rally, it is calm. Recently I have increased my favorability toward inflation trades, and if GSR remains subdued, that prospect can remain in play.

The weekly chart shows how far USD could drop (within its intact bull market) if the support at 100 (+/-) were to be lost. That would-be target is 93.50, which would maintain a series of higher highs/lows from 2008.

Bottom line is that USD’s daily chart technicals do not look good, opening the door for a potential drop to 93.50, which would likely bring a big relief rally to commodities and other inflation trades (precious metals would tag along too, as the ‘death of the dollar’ bugs lather up). But if/when something breaks on the macro, all bets are off and USD would likely gain a classic liquidity bid. Watch GSR and other systemic stress indicators for clues (as yet, they are mostly sedate, with an eye on yield curves).

The currency cavalcade shows gold ally Swiss Franc taking a nice anti-USD pop on Friday and the rest of the pack also bouncing. For technical views, generally look at the slopes of the respective 50 day averages.

Finally, Bitcoin (daily) is testing the upside target zone, which was registered in April. It’s sitting on the first support level at the EMA 20 (29860) and has more support at the SMA 50 (28107). If USD were to break down this trade (and associated mania) could go back ‘on’.

Portfolio

Savings balanced by gold.

Trading Account: Short QQQ

Roth IRA (non-taxable, no contributions)

Cash is 82%. If an anti-USD trade manifests (still very much an “if”), short positions will most likely all be eliminated, although said trade would probably favor the likes of commodities, precious metals, EM/Asia, etc.

So today the IRA is in risk management mode as Fed fears infected markets yet again and drove long-term yields upward… yet again. But from here markets either take a correction with potential for liquidation (with the USD likely shaking off its poor daily chart technicals and gaining liquidity bids) or a seemingly improbable but rewarding inflation trade, potentially on a large USD decline within its bull market. I am ready for either of these opposite outcomes.

Cash & income-paying Equivalents are at levels that are right for me and my real-world situation. Your situation is different. Cash will be adjusted as needed.

Refer to the Trade Log under the NFTRH Premium menu at nftrh.com for trade info, if interested (not that you necessarily should be). Also, you can follow at Twitter @NFTRHgt for notice of updates.

NFTRH is not to be distributed to third parties without prior written consent

Notes From the Rabbit Hole (NFTRH) is a weekly market report in which we provide analysis on financial markets. We make every effort to provide accurate and high quality content, but this analysis ultimately represents our opinions and these opinions are provided without warranty or guarantee of any kind. See full terms & conditions of service under the ‘About’ heading in the main menu.