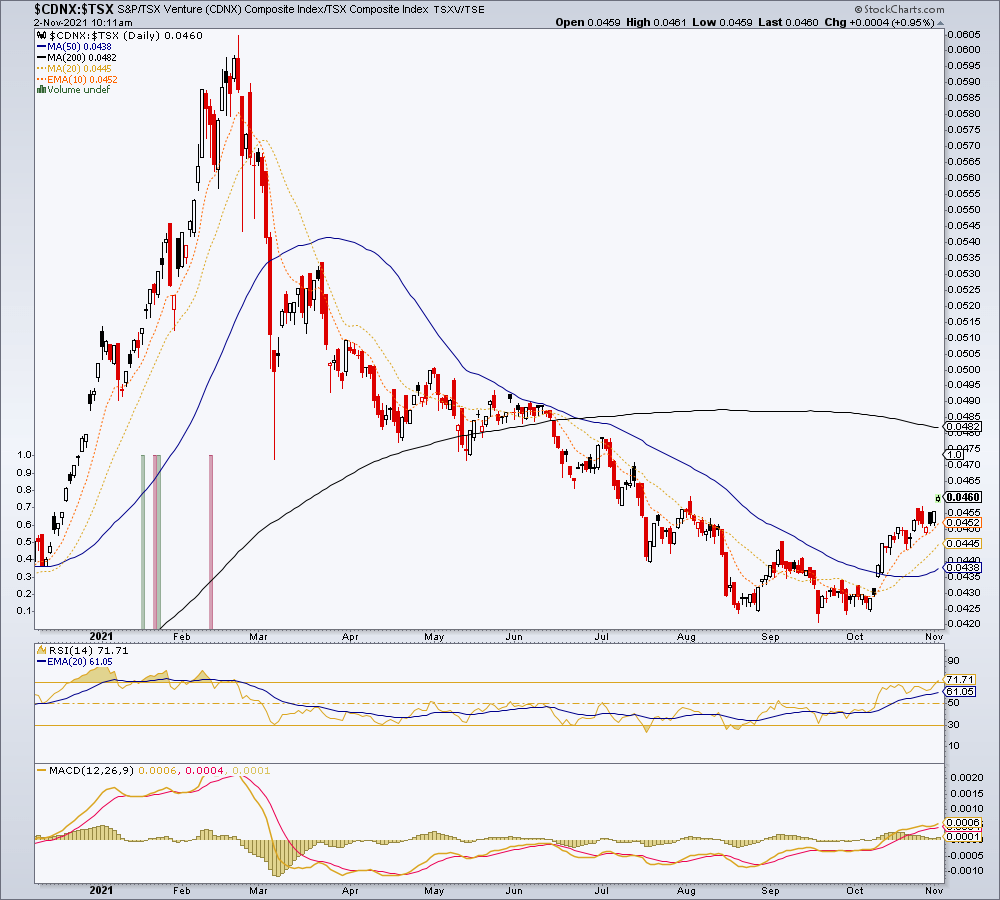

In May 2020 an NFTRH+ update reviewed the TSX-V/TSX ratio, which had taken out the 200 day average as we gauged the coming inflation trades with a bullish eye. Remember, back then it was hard to be an inflation trader, but this signal was a good one as proven now by history.

Then in June 2020 we noted a Diamond in the Rough, as the ratio paused before surging to higher levels.

Today the ratio continues to bounce and has broken trend after the long ride down in 2021. It is an inkling of regenerating inflation trades as long as that is the case. What I want to make clear however, is that the inflation trades may well have a limit. In fact, that is my bias with the 200 day average a potential target for TSX-V/TSX, the 2.6% to 2.8% range as a target for the 30yr Treasury yield Continuum, etc.

But even if it is a limited rally, it appears trade-able, if indeed the inflation indicators like ‘expectations’ hold around current levels post-FOMC and a new leg comes about.

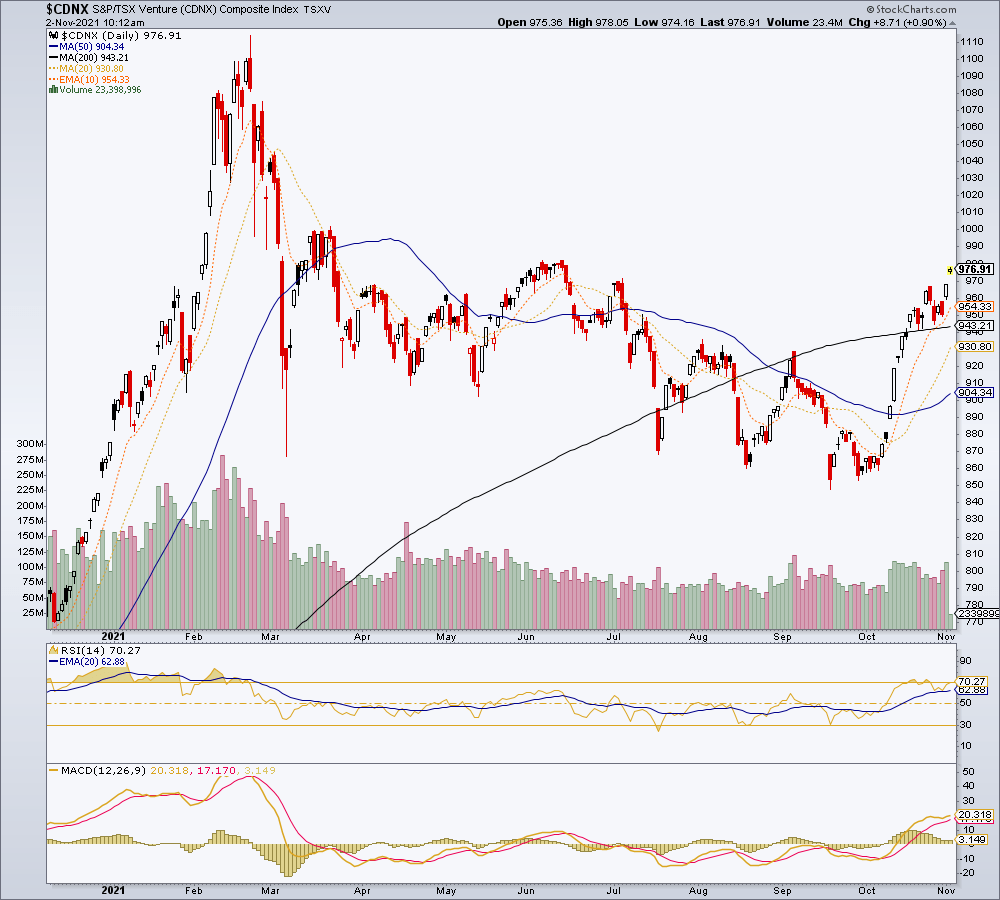

Of course, no speculative inflation trade is going to come about without the nominal TSX-V also going along, and it also continues to look constructive for further upside.

Let’s clear FOMC and see how the dust settles. But as it stands now we are still speculative inflation trades ‘on’, with an open question as to sustainability. For safety’s sake and for the sake of not getting caught up in the “commodity super cycle” promotions making the rounds, let’s plan on keeping a multi-week, even multi-month window open for a bullish view, but not further than that. There is no need for hysteria, hype or talk of a “super cycle”. Just management.