Semi Sector

Let’s begin at the beginning, with our Semi Equipment indicators. Again, for the many folks who were not with us in January of 2013, we recall that month as the first inkling that the Semi Equipment (companies like Applied Materials, Lam Research, KLA Tencor, MKS, etc.) sector was experiencing a surge in bookings per the then-available book-to-bill ratio available from SEMI. These days SEMI only reports billings, which is far less useful than bookings as an indicator, but the site still provides useful industry information.

In the spring of 2013 we were able to confirm a (3 mo.) trend in Semi Equipment booking, we established a cyclical continuum: Semi Equipment > Semi > Manufacturing > Employment > Strong Economy; and the rest is history. So back then we had Fab Equipment bookings to work with. Today we have more general industry news (which has forecast growth in 2018, but at a sharply slower pace) and our ratio charts of two premier Fab Equipment companies vs. the broad Semiconductor sector and Tech.

Here are the daily views as reviewed in an update yesterday. AMAT & LRCX continued to weaken vs. Semi and held the S/T breakdown areas vs. Tech because the broad Semi sector was relatively less weak than Tech.

I want to add the weekly views to show that the intermediate trends (post-2015) are in the process of changing from up to down as the ratios have been below a supportive moving average for a few weeks now, continually testing but not rising back above it.

I don’t want to make too big a deal about a single indicator, but I cannot shake the symmetry of a thought process that asks if it worked in 2013 as a positive cyclical indicator, why not in 2018 going the other way? Now, a reminder that the process – and it is a process – took a long while to unfold back then and our minds work in real time while the economy’s mind works over time as it rotates, rationalizes and adjusts. So patience is important. But we just may have an important, and negative, economic cycle indicator in its infancy.

The above is the non-traditional indicator that probably only we are watching. Let’s take a look at a few other market ratios in light of yesterday’s rise in L/T interest rates (macro Amigo #2) and the bounce in USD, which after all, came from a logical long-term support in the 88-89 area.

Healthcare Sector & a General View

The reason I am even aware of Semi Equipment vs. Semiconductors is that my former vocation was as a manufacturing guy and this stuff was very important to manufacturing cycles. Another thing that was very important was sustainability through the economic cycles, which is why I transitioned my company into the Medical Device/Equipment segment. It was a much smoother ride (in my experience through the recessions of 2001 and 2008).

So here is the state of the sector after yesterday’s downside. It was firm vs. the market.

More importantly, the monthly chart shows an attempted breakout from the downtrend channel (needs to close January in this condition to confirm). This would likely do away with the noted ‘double top’ scenario if weakening economic signals start to come in.

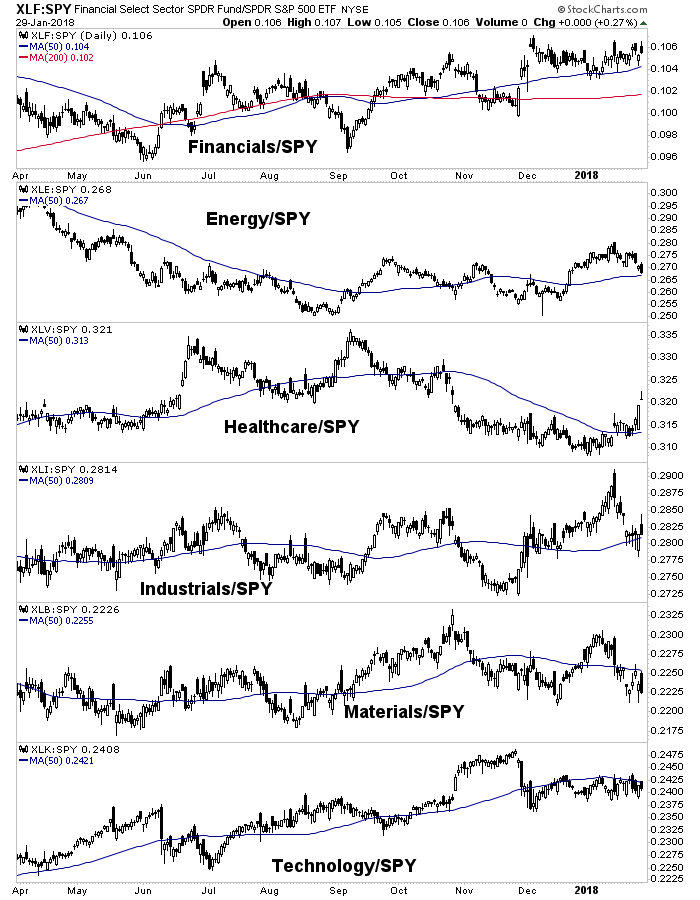

Healthcare in general would also be relatively firm in a decelerating economic cycle (if applicable). It’s not just devices. Here is what various sectors did yesterday relative to SPY. Financials were firm with the spike in interest rates, Energy is testing the SMA 50, Healthcare zoomed and the others held their varying sideways stances vs. SPY.

Per the Trade Log I gave EW (a medical device co.) and its Ascending Triangle a shot yesterday to go with other holdings in the Healthcare sector. I also tried shorting the Semis again. At this point I am trying to balance the portfolio between being bullish relatively favored and bearish on less favored sectors.

I am trying to keep in mind that our indicators may be early and not to over react to the speed of my own brain waves (a fault I have). But with gains thus far in 2018, my primary job will be to protect the remainder of them because taking a big picture view of an economy that is probably as good as it gets with a fledgling negative cycle signal and people WAY over bullish everywhere you look, dividend paying cash is oh so attractive.