The yield curve is in a down trend on the big picture. This has logically been attended by economic and market stability as its message has been one of little financial/economic stress or inflation.

The downtrend began in 2013, after late 2012’s Fiscal Cliff hysteria died down and the signals coming from the Semiconductor sector began indicating a positive economic cycle to come (recall that we extrapolated Semi Equipment > Semiconductor industry > employment > economic growth. Well, that last thing has been unspectacular, but you get the theme.

As you know, I am overwhelmingly bullishly deployed in this market (subject to change at any time of course). At least as relates to long and short positions, which currently are many and only 2 (consumer cyclical, junk bonds), respectively. Other risk management is in pro-USD vehicles (including a Euro short), cash and gold. But mostly, I am positioned to benefit from a rising stock market.

So all of that is a caveat in that I am not predicting doom by noting a potential bottom in the yield curve. First off, it is only the most preliminary potential and secondly, during the initial stages of a yield curve rise – if applicable – it is entirely possible or even probable that the Banks and Financials would rise with it, since the implication of ‘borrow short and lend long’ would be profits for these companies, assuming the curve steepening were happening along with rising nominal long-term yields.

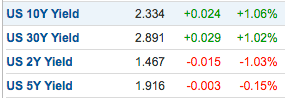

Here is how the yield curve ended yesterday’s session.

Today, by implication of nominal yields, the curve is up again as the 10yr yield is positive and the 2yr is negative. I try to balance between not sending you alarmist updates that jam your radar and not being too timid in sending you updates that I think may be relevant. I think this one has a chance to evolve into something relevant. More to come as needed in NFTRH 467.