I hesitate to do these updates after roiling market events because they feel more like news reporting than market analysis.

Gold got hammered!

Silver got hammered!

The miners got hammered!

But the projections were gold 1300 (+/-), HUI 195-200 and silver 17 (+/-). Those are the logical supports and all items have declined right into those zones. Now, will they hold there? That I cannot tell you. But I can tell you that I am unhedged the miners again after noting a re-buy of the DUST hedges in a public post yesterday, pre-FOMC (monitoring all posts, subscriber-only and public is recommended because public posts often dovetail with NFTRH themes and analysis). I am still indirectly hedged by being long USD (UUP) and short the Euro (EUO).

This is a time to be cool and for crying out loud, to not listen to the “gold smack down!” brigade who always seem to find excuses to make the bitter pill of the precious metals’ volatility go down easier. The Fed is on a tightening regime, however slow it may be. It is also planning to shrink its balance sheet. These things caused a bounce in the US dollar and in Treasury yields, which have been rising anyway to normalize previous unsustainable downside (we have after all, been noting bearish bond sentiment and CoT profiles for many weeks now) as bonds had been getting bid up. But long-term bond yields have not yet made anything approaching a convincing break to new up trends.

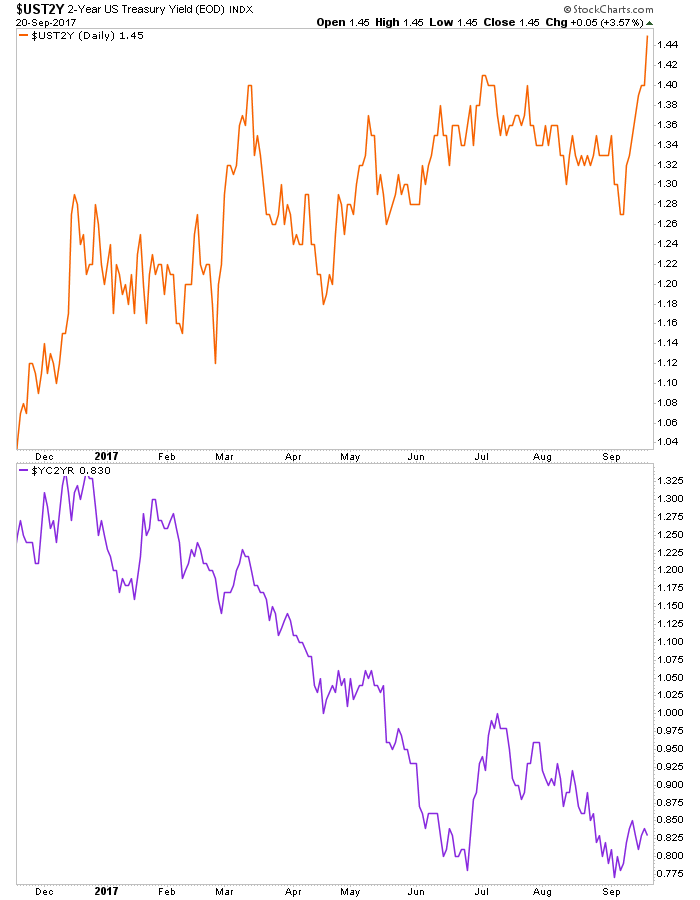

The yield up trend belongs to the 2yr, which has been up trending all along. On this chart, the top panel shows the 2yr yield and the bottom panel is the 10yr-2yr yield curve. Neither of these are gold-friendly and both of these are Fed/economy/market friendly. None of this is new. Now, were that to morph into a double bottom in the curve?… Then we’d be talking a different story that would include inflationary signaling and positives for gold, silver and commodities (which did not get clobbered yesterday, which I found interesting).

Yellen did some talking about the US dollar and inflation. The Fed is concerned that they have not yet been able to promote it to 2%, and I’d only say that one day she may regret getting what she’d wished for and more.

But for now, the signaling remains positive for the economy and the stock market. The gold sector needed a correction and the Fed (which did nothing unexpected) was an excuse to resume ramming it home. That is great work gold has done to boink below 1300 and HUI has done to doink below 198. If these support parameters give way, they give way (and people need to adjust or hold firm as their investment orientations demand). But the thing is, they have not given way.

We are right where we expected to be. The media will give… reasons. Emotions will stoke up. My view is that the macro is shifting on the bigger picture and that includes the stock market. Now, the current view of an impending correction for Q4 may be wrong. One example of how? Wouldn’t it be ironic if an inflationary situation were to whip up and get out of control as the Fed reduces its balance sheet? Crazy talk, eh? Well it seems to me that a global deflationary situation (Goldilocks in the US) whipped up as the Fed was expanding its balance sheet through QEs 1-3 (with a side order of Op/Twist).

There is an argument that stocks can correct under pains of inflation (as input costs rise), but they can also continue to rise as other assets get bid even more in an out of control monetary tide that raises all boats. So I am staying open minded, which seems like the only rational course in a market with so many signal-distorting inputs over the last 9 years. After all our other, I think more probable plan is that precious metals weakness can lead the stock market and commodities downward before the big inflation. Here we reference Q4 2008 (big event) and Q1 2016 (much smaller event).

For now, my orientation is long the gold/silver sector, long commodities and long stocks while remaining long USD and short Euro (all subject to change for reasons that would be noted in updates, reports and/or public posts if/as needed). I keep looking forward to shorting opportunities on the stock market, but I am being very patient there. It’s best to separate the daily goings on from the big picture view, which moves so slowly we can’t really see it on a daily basis. The bottom line is that nothing has changed… the stock market is in a firm uptrend, bond yields are aligned positively for the economy and stocks, commodities continue to bounce and the precious metals are taking the correction they needed to the parameters we projected.

Now let’s see what we’ll be updating on Sunday in NFTRH 466. See you then!