We have shorted GS, longed GS and shorted it again (NFTRH+); all for profit (if only all trades worked so well). We also had a successful short setup on the Financials ETF, but it has been noted lately in NFTRH that Financials are actually still bullish relative to the S&P 500 (SPY) on the big picture, as the leadership has consolidated downward (but not broken) with bonds bouncing and long-term Interest rates declining.

With the bond play being over (whether or not in price, certainly in its contrarian bullish setup) it may be time to keep an eye on the Financial sector. I Pulled a few daily charts for the review of anyone who feels that bonds may be played out and the stock market’s bullish mania has further to go.

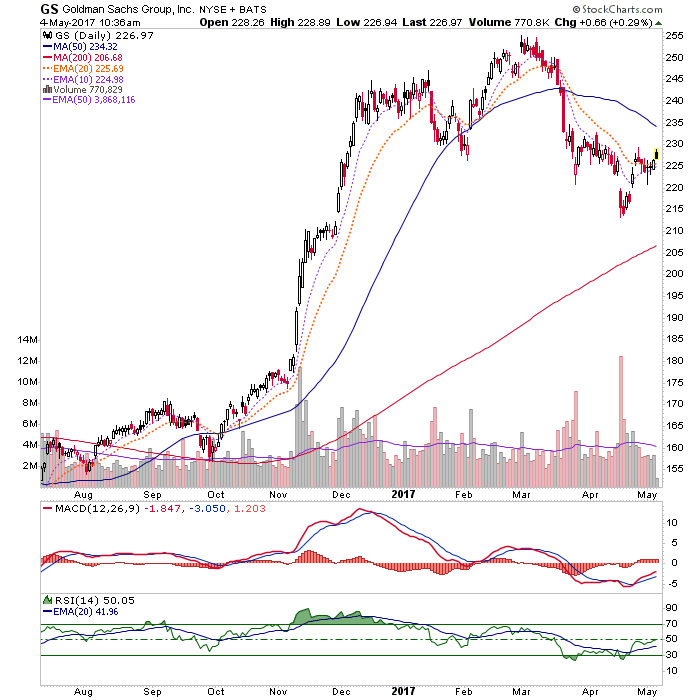

Old friend the Vampire Squid is in a funky little pattern, trying to turn up from the EMAs 10 & 20. Obviously, those EMAs would be important short-term support for a bullish scenario. A failure could bring a later buying opportunity at the rising SMA 200.

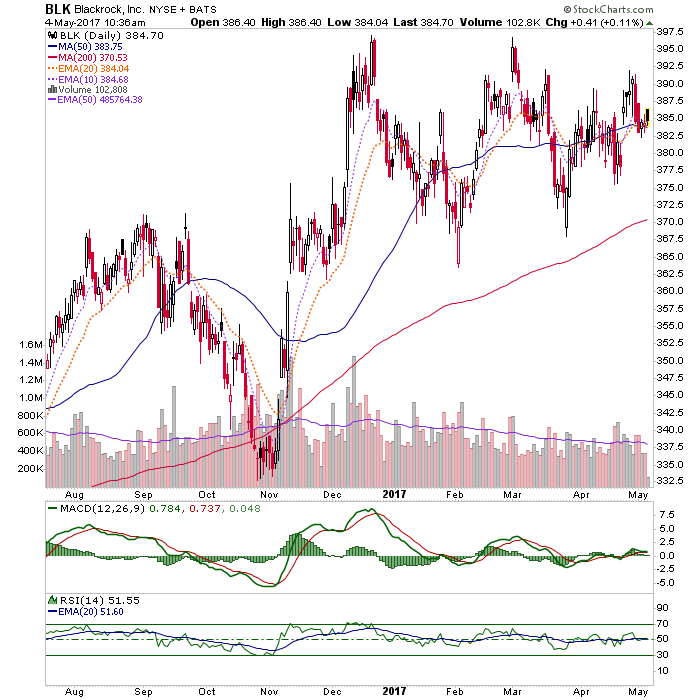

BLK could be in what may eventually form into an Ascending Triangle. I’d like to see the SMA 50 hold to keep it on track. Otherwise the SMA 200 would be open.

The Regional Bank ETF is trying to break above the SMA 50. A rise above 56 would measure a target of around 60.

The Financials ETF is very similar, and would target the March high if this pattern holds up.

No big conclusions here. Just that these items positively correlated to interest rates (negatively correlated with bonds) are hinting short-term bullish. If one develops a bearish bond view – and the stock market remains firm – this would be an area to consider.

A side note here; according to our often viewed yield correlation graph, Banks and Financials are the best for a rising rate environment. But Pharma and Biotech are among the worst. Yet we have a bullish stance on Biotech currently. So, in line with what is a very challenging market lately, this is a consideration as well. It is not likely that both Financials and Biotech are going to thrive together beyond the near-term. One would lose the benefit of yield dynamics, one way or the other.