We have belabored yields and yield curves (and TIP-TLT / 10yr Breakevens for that matter) and the signs have been inflationary. Today with the broad futures up once again, we are on the verge of managing the US stock market right through the door (SPX 2160) to a bullish state.

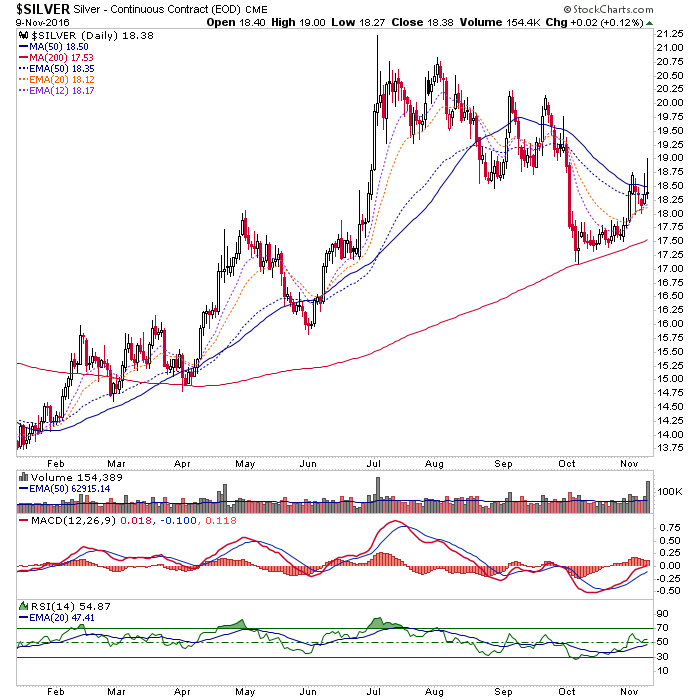

Gold is up in pre-market, but only to 1280 (it needs to clear 1310 to signal a bullish resumption). Its SMA 50 is 17 bucks higher at 1297. Silver is up to 18.77, which puts it above the SMA 50 once again. If it keeps trying like this it could actually make the leap and end the downtrend, at least temporarily.

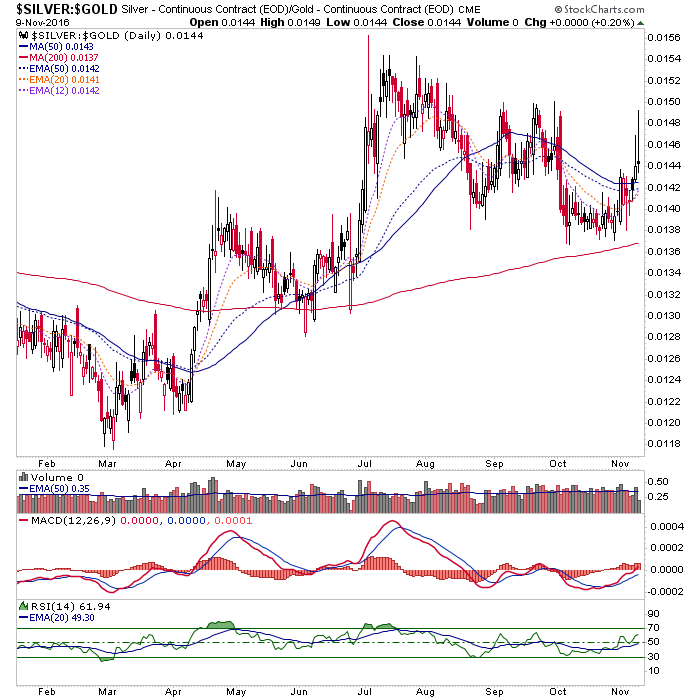

For the purposes of talking ‘inflation trade’, Silver vs. Gold is important. Silver is +2.05% in pre, while gold is +.60%. In other words, the silver-gold ratio is rising and testing the highs of August and September again.

The point here is not to be precious metals exclusive if we are talking ‘inflation trade’. Silver and gold, along with Treasury yield dynamics are indicators to a risk ‘on’ burst that appears to be playing out across most asset markets. Gold obsessives may try to cast gold and silver as something special – and don’t get me wrong, on the big picture I think gold at least, will be because of its unique counter-cyclical qualities – but what is brewing out there now seems to be an equal opportunity momentum play.

It would be important now, if/as endorphins get released (confirming standard gold bug views), not to get sucked in by the ideology of ‘Trump this, inflation that…’ and peer at the precious metals in any kind of a vacuum. The world is hopping up on momentum, and that includes the precious metals this morning.

The reason I write the above is because I know that subscribers do their own research and take in views from around the spectrum. I also know that the gold “community” is a cult-like one that encourages a narrow focus. Well, the asset market burst – assuming it does not roll over today or tomorrow – is not narrow. It includes base metals, global stocks, US stocks… everything it seems, but bonds (amid rising yields).

Bottom Line

My personal orientation right now is to have some miners (as noted yesterday), maybe even add a couple on opportunity, but also be well mixed across the asset market spectrum. This includes Japan, Europe and a good dose of US stocks, including all items held as of last weekend, plus the Transports (recent NFTRH+) and Energy (added back yesterday) and even old friend AMAT, which was down yesterday. Semi Equipment and Energy are among the sectors that according to the historical data, have had a positive correlation to rising 10 year yields (ref. data graphic from last night’s update). As always in this ginned market, cash will remain significant as well because I have not changed my primary directive, which is to keep the majority of 2016’s gains.

Taking it a step further, I am looking at the markets in increments, or chunks. In other words, if this continues to go bullish, the chunk will be perhaps only to the end of the year. This would be because a) it is a market being driven by fear, greed and momentum, and b) we have data that shows a positive end of the year when a Republican takes office, but a brutal year 1 (2017). Depending on sentiment, it could also flame out sooner than year-end.

So, I will consider chunk #2 near year-end and either stay/increase long or happily short the pig when that looks like the best risk vs. reward scenario. That latter condition (projecting bearish markets) would by the way, be the time to take real interest in the gold sector as well. To this point we have managed nothing more than a major support test for US stocks while people got ever more bearish, culminating in the revulsion of early Wednesday morning (the Trump Dump), which set the stage for a ping to the opposite pole. VIX has been hammered back down, but we’ll need to review signs of briskly over bullish sentiment before forming new bearish plans.

It could take a while for all of this to play out… or not. Open minds and perspective are key. I will try to stay on top of the interpretations along the way, but welcome your contrary interpretations as well. This is not about any one individual pretending to see the future. It’s about plans and adjustments along the way. For months we have been on a plan of a major support test and if the Trump Dump was the culmination, a bullish burst would now play out either sooner or later. It is looking more and more like we can bring the Continuum into the picture as well, to see when the caution flag might come out for an inflationary risk ‘on’ burst. The 30 year yield is at 2.9% and the limiter currently resides at 3.4%. So another thing we’ll need to watch for is “DEATH OF BONDS!” or “Great Rotation II” (into stocks from bonds) type headlines. That would likely be a sell signal to be used in conjunction with other data at the time to indicate the end of the party (again, assuming the bullish course follows through this week).