S&P 500 has dutifully curled down from the red dotted trend line just a hair below the 2040 resistance area. The market is positive pre-US open and may try to bounce from the green shaded short-term support area that it rests at now. Below that, I don’t think that 2000 +/- (‘W’ support) is going to be given up without a fight.

But this week feels a bit heavy and lo and behold, participation is fading the bounce rally (as dumb money follows it). Stockcharts.com: “The Participation Index (PI) measures short-term price trends and tracks the percentage of stocks pushing the upper or lower edge of a short-term price trend envelope.“

SPX weekly shows that Bullish % (shaded area), another way of measuring participation, is rising with the rally in stocks. But this recovery was always going to happen with the bounce. This is the chart we originally used to compare 2015 with 2011. We have since added in-depth weekly views of 2001 and 2008, which are the bearish ‘comps’ per NFTRH 364. 2 out of 3 comps say this is a bearish setup when looking out several weeks to a few months.

Notes

The bounce is maturing and is already in the range for those wanting to be actively bearish (ref. 2020 to 2060 range) to begin scaling in with a 2-3 month horizon. This with consideration of the outside chance SPX bounces as high as 2100, which is the ‘W’ pattern measurement and the fact that 1 out of 3 comps says the resolution could end up bullish. What’s more, as we noted at the depths of the August/September hysteria, that kind of extreme sentiment reset may have precluded any real, trade-able bearish activity for an extended period.

Speaking personally, I am not quite ready to short this market and still hold some longs, including the Boston Scientific (BSX) NFTRH+ highlight. The long stance (with heaps of cash) could change at any moment pending new info, but for now short is not my preference. Indeed, just look at what happened to Biotech yesterday when Citron Research (a short seller) put out a negative piece on one company. The market seemed to channel Hillary Clinton and tanked the sector. That does not seem to reflect a strenuously over bullish sentiment situation.

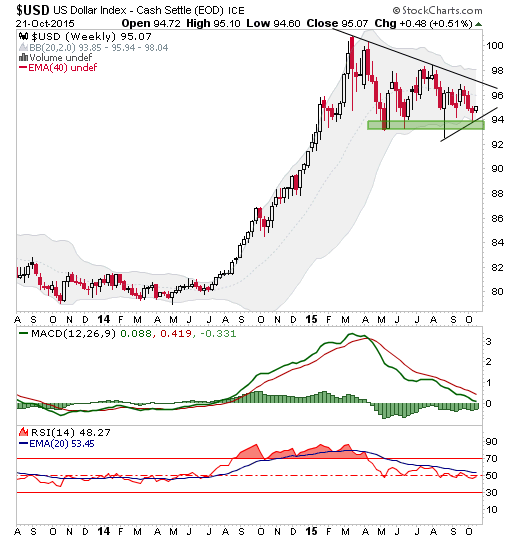

Moving on, the US dollar has refused to break down, which is telling us something. Last week it made a weekly close above support (Sept. low) after a brief break below and there it remains 4 days into the new week. Commodities and Emerging Markets would be vulnerable again if Uncle Buck continues to hold firm.

As we know, the gold sector went up with the USD corrective activity. So now it can continue to go down if USD firms. This negative reaction was logical (for reasons already noted) and the best investment environment in the sector is not going to be when it rises with oil, copper, stock market, etc. We will manage the precious metals somewhat separately because at some point I expect gold to go counter the conventional markets and in the big picture birthing of a new gold sector bull market (pending corrective activity) the USD is not to be feared, while in the smaller pictures it often is. Here again we maintain views on gold-oil, gold-crb, gold-stock market, etc. The latter especially, has been a holdout.

USD’s daily chart still has a bearish look to it but considering the longer-term view is and has been bullish (pending possible drop to high 80’s) another weekly close above the September low of 94.20 would make the hold of support even firmer. Here’s the weekly, having completely worked off the over bought conditions of its first hysterical rise from mid-2014 to early 2015. It is not as yet a bullish looking thing, but it has thus far held support, and that is the first step.

Finally, a look at daily gold and silver. To this point, gold seems to be consolidating in a bullish manner while silver looks short-term toppy from the point we first took caution on it. Silver still looks like it can do the ‘normal’ pullback to the low 15’s, where there is support. We continue to operate on a plan that this is a pullback of an ongoing rally in the sector (ref. yesterday’s update on GDX).