Summary

US Stock Market: Has been at elevated risk for many months now. But no crack yet. On Friday SPX pulled back hard to the uptrending 50 day average. I wanted to short it in the worst way, but held off. When I short this market I’d prefer speculating net short, not hedging. But for that I need at least some kind of a setup. A hard down on Op/Ex Friday was not that. Not yet.

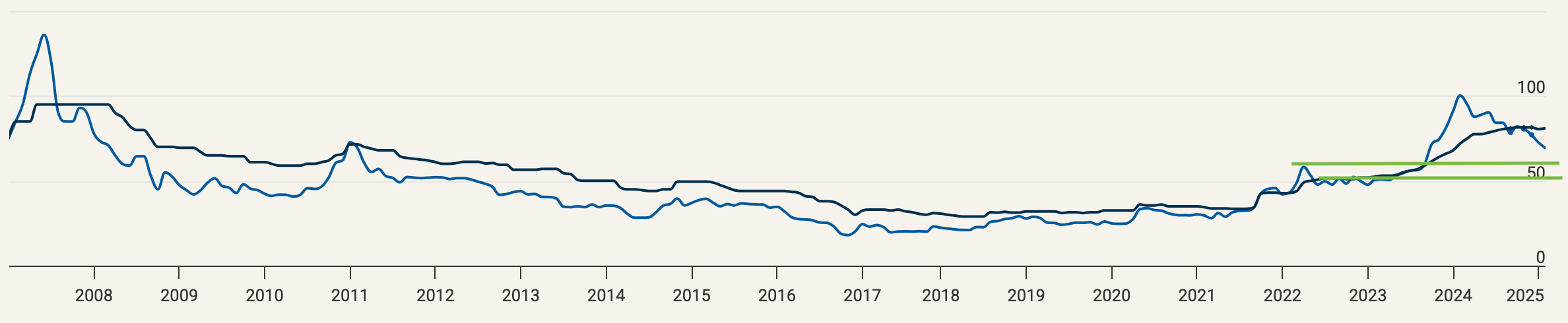

US Stock Market Internals: The SOX > NDX > SPX leadership chain is in trouble. SOX is now trending down vs. both of its fellows since last summer. Meanwhile, the XLV (Healthcare)/SPY (Broad) ratio continues to look like a bottom. If so, such lows and subsequent upturns preceded major bear markets in 2001 and 2007, and the mini-bear correction in 2022. And then there is this. The dangerous looking divergence by the VIX continues.

US Market Sentiment: Structurally over-bullish, subject to short-term bursts of greed and fear. Conditions are and have been ripe for a major correction or bear market. A reminder that sentiment is just that, a condition, not a timer.

Global Stock Markets: Our view of China out-performance for 2025 sure is kicking into gear. This does not mean nominal China/Asia will remain bullish, but thus far they (I own AAXJ & EWH) are. Global (ACWX) has been bouncing vs. the US (SPY) for all of 2025 so far. But that is likely a reflection of the weak USD and would be vulnerable if USD finds a low and catches a bid.

Precious Metals: We have noted week after week that gold’s sentiment profile was “high risk” per Sentimentrader’s data. The sector became overbought as we noted a couple weeks ago in NFTRH 848. But we may finally be shaking the tree to see what falls down and to what support areas. However, this is noise for long-term investors and would appear to be a buying opportunity in the making due to longer-term technicals and macro-fundamentals that continue to evolve nicely. A final fundamental underpinning would be a real crack in US stocks. That could begin a process of turning the macro definitively counter-cyclical.

Meanwhile, the Fort Knox audit, “LMBA Crisis” and Tariff hype in gold should probably ignored. The golden sleuths are at it again, trying to transfix readers about the bullish doings in the gold market. Gold, while below our target of 3000+, is getting overbought and has been a card carrying member (and leader) of the broad rally.

Commodities: It’s been Whack-a-Mole. One pops, another drops. All against a backdrop that is biased adversarial with disinflationary winds blowing. Commodities are not gold and commodity producers are not gold producers. Commodities are cyclical and we are looking for a counter-cyclical macro to engage before the next inflation problem becomes evident.

US Treasury Bond Market: Despite the uproar about Tariffs and inflation and still-sticky prices for consumers, I expect that the macro will continue sliding disinflationary (pro-bonds) and likely devolve into a deflation scare of some kind. The economy is decelerating and cash and short-term Treasury bonds would be the receivers of risk-off liquidity when the stock market tops and turns down for real.

USD (and Gold/Silver Ratio): USD is still testing the support of its base breakout. The GSR is biased positive. The analysis leans toward forward strength in these two, and the coming of a market liquidity problem that would bring down most markets/assets. I am 70/30 for this scenario. If the 30% plays out and USD and GSR drop, Wayne and Garth may prepare to party on, inflation style.

Other Indications

- 10-2yr and 10yr-3mo yield curves continue to steepen even as they’ve consolidated of late. The indication is for an oncoming economic/market bust. Here is the 10-2 big picture. Stock market vulnerability aplenty.

- VIX (shown above) popped on Friday, indicating anxiety (Op/Ex?). But these spikes can be “one and done”. More anxiety will be needed to break the thick speculative confidence of the bubble markets. Fellow indicator of calm vs. anxiety, High Yield Spread, is completely asleep indicating risk still “on”.

- The negative divergence by the 2yr Treasury yield to the Fed proxy T-bill yield eventually saw the Fed weaken its hawkish stance a bit, as the divergence would imply. However, in Q4, 2024 the market drove the 2yr yield up, which has not caused active Fed hawking, but has caused them to eat some microphones talking about inflation that still needs to be dealt with (so damn predictable). If 2007 is a blueprint, it goes like this: Fed softens to support markets as inflation eases and the economy starts to show signs of weakness (as has already happened). Then new inflation signals crop up, the Fed firms or at least pauses its dove cycle and then… SPLAT! The whole edifice tanks as inflation drops uncomfortably (media/economist code for deflation scare) and policy heroes screw savers again by killing interest rates in service to asset owners.

- However, on this cycle so many things are different than they were in previous cycles. That is because we have never had insurgent agents of the White House dogging their way through the government’s books, cutting savagely and completely distorting “business as usual”. In this regard we can have perspective that some things may be different this time.

- But the indications do not lie. They indicate. The implications may get distorted, may be less or more severe, but they are there and they are not at all positive.

- My guess? The downturn is going to be severe. Perhaps one day, if Trump/Musk/DOGE are not utter destroyers with no “build-back” plan, we will catch an important low to a bear market that begins in 2025, and invest long again. But as I see things now, it is way to soon to be thinking that way. It is not too soon for speculators to be preparing to be short for a bear market and investors to be risk-managed into a bear market.

Admin Note

A reminder that NFTRH reports will likely be more abbreviated until mid-March or so, and in-week updating may be limited, as I am having surgery this week. I expect to be up and at ’em after mid-March.

US Stock Market

SPX (daily chart) came close enough to the upside target that it could have made a top. However, Friday’s Op/Ex downside put a spook into markets while all SPX did was tested its 50 day moving average again. Uptrending SMA 50 and SMA 200. No technical damage. Let’s see what this week brings.

NDX has a similar story. Negative RSI divergence, but all important trends up.

In the Summary segment we mentioned that Semi sector leadership is trending down. That is a negative cyclical and market internal indication. If defensive Healthcare (XLV) is indeed making a real and important low vs. broad SPX (SPY), another counter-cyclical indicator.

We won’t include the long-term chart, but suffice it to say the implication of a would-be upturn and trend change (far from reality as yet) in XLV/SPY would be a bear market indication.

US Stock Market Sentiment

Friday put a little blip in Dumb money’s bullishness, but generally sentiment risk is high in stocks. There too is gold’s high risk rating per Sentimentrader’s data. This high risk, much like with stocks, has come during a big bull phase. As we all know, risk can take longer to be realized than our patience can hold out if we are actively positioned against it.

However, in the interest of not getting too transfixed with the bearish view to the exclusion of an open mind, note how Dumb money sentiment has negatively diverged the broad rally that began in Q4, 2023. That is classic “wall of worry” stuff and is a positive contrarian marker for the bulls. Minor, in my opinion, but there it is.

The reading in bonds continues to support a rebound in the bond market (pullbacks in yields). See segment on bonds below.

NAAIM were zooming back to briskly over-bullish on February 19th, pretty much begging for Friday’s smack down. At 91% bullish, they were in fine contrary indicator form.

I have lost access to Investors Intelligence data, as apparently so has Yardeni. We will have to live without the newsletter brigade’s status for the time being.

Ma and Pa (AAII) are still available and they were deeply retrenched as of Feb. 20th at a .72 Bull/Bear ratio, compared to an excitable 2.4 last summer. Their anxiety is a contrary positive for the stock market.

A Closer Look at the US Treasury Bond Market

Here is an interesting situation regarding commercial hedgers, which would theoretically be positioned bullish at/near lows and bearish at/near highs. As we move along the duration curve, from short to long, we see a progression where the longer the duration, the worse the prospects for the bonds in question, on a contrarian basis.

If that plays out logically, it also implies that our steepening yield curve view is right on, as commercial players are also expecting short-term bonds to perform better than long-term bonds (another way of saying long-term yields will decline less than short-term yields, or rise relative to short-term yields, which itself is a way of saying “steepening yield curves”). Let’s view the bonds from short to long-term.

The 2yr Note is at an apparent price low with commercial hedgers briskly net long.

The 5yr Note is a-okay, maybe even asking me to expand my positive bond view from 0 to 3 years up to 5, for a little extra income. All theoretical, folks. But it’s informative.

The 10yr degrades a bit but is still biased contrary bullish.

It is way out on the curve, in the 30yr that things get flat out bad. That is just a terrible alignment, contrary-wise.

The message appears to be that we are and have been right to be long some short-term bonds, favoring them over long-term bonds, and also right in first anticipating and now managing steepening yield curves.

Extrapolating further, I expect steepening curves, which tend to come with counter-cycles and economic busts, to prove out as well. Hence gold stocks, the counter-cyclical sector. See how it all plays together?

I love this stuff. Some people like Super Bowl parties and betting squares. Some people like March Madness. Some people like bowling. I like nerding out on macro indications.

Global Stock Markets

Meanwhile, it is interesting that China large caps continue to forge a trend change to up vs. US large caps (FXI/SPY ratio). Indeed, the ratio is getting somewhat overbought to the upside. But the trend is changing to up and you will recall that back in 2024 we viewed China out-performance as a potential feature of 2025. This, despite Trump’s threatened punishment of China. “Who is punishing who in 2025?” is a valid question.

Asia (ex-Japan) has been held for a while now and is performing as desired, having threatened but ultimately held its major trend marker, the daily SMA 200. I don’t expect Asian holdings to merrily go on their bullish way when the broad markets top, however. But relative trend changes, led by FXI/SPY, could persist.

Per the trade log on Feb. 18th:

It then caught on. The chart view is proving correct so far, but the timing was luck.

The balance of the world (ex-US), ACWX, is still on the bull.

We see by the ACWX/SPY ratio that the situation is much different than China/US, which has changed its trend to up. The balance of the world is only bouncing within a relative downtrend. A deeper decline by the US dollar would aid this ratio. A recovery by Uncle Buck would impair it.

Precious Metals

Reference Friday’s NFTRH+ update, which managed the situation in gold stocks and covered a few positive macro indicators for the sector. We don’t need to belabor the technical situation. Nor do we need to belabor the macro-fundamental situation.

The technicals are short-term vulnerable to correction, long-term bull market.

The funda, the true funda as opposed to those fantasized by many gold boosters, are well in progress with the main holdout being a definitive crack in the US stock market and a weakening economy eventually flashing “recession”, or the bust side of the boom/bust continuum. This is an extended process that is still in progress.

One further note on the correction potential: We have been noting for over a year now that the broad rally has included and often been led by gold and gold stocks. Hence, we also noted that the sector would be vulnerable when the broad markets become vulnerable. In microcosm, it is interesting that US stocks and precious metals got hammered on Friday.

Okay, let’s relax our eyes and reflect on this big picture view of the stock market vs. gold.

Since 2011 monetary policymakers have done all they could to sustain the bull market in stocks. Indeed, the bubble was in policy, in mass greed, in debt-fueled chicanery. Stocks have relatively and massively outperformed gold since then. Ah, but the trend is sideways over the last few years. That is base-making in preparation for a new macro, in my opinion.

Indeed, today we are in a new macro; one that is not going to be as permissive of monetary chicanery as the previous macro, the pre-2022 macro. Says who? Says the Continuum. A decades-long trend (in disinflationary bond market signaling) in long-term yields that had allowed policymakers to inflate at will at any and all points of market/economic danger, is no more. Poof. The bond market had enough in 2022.

That leaves Trump, Musk and his DOGE doggie to do the work fiscally, because the Fed is marginalized in its ability to manipulate (monetize) bonds at this time.

So with the allowance that I for one do not know how things are going to play out, I do know it will be different than the previous business as usual. Now again refer to the Gold/SPX chart above. That 13+ years in the wilderness for gold relative to stocks has been a purification of the case for gold. A long clean out of an asset and sector left for dead (in relation to the boom-boom risk-on trades in stocks).

Again, gazing at that big picture chart of Gold/SPX, if you had to deploy in one asset or the other, which would you choose on a risk/reward basis? Me? Gold, a no-brainer in my opinion, relative to stonks.

Okay, let’s clean up a couple other sector indications and move on. The update linked above discussed gold’s ratios to risk-on assets and gold’s relationship to market inflation signals as relates to gold stocks.

Further, the HUI/Gold ratio’s (HGR) 2025 uptrend got cracked hard on Friday. This was unlike the previous Friday’s sector downer when the ratio held intact.

That is the bad (short-term) news and it adds some validity to the update’s assertion that a correction can go deeper in the short-term.

However, let’s review the big picture of the HGR, which we have not done in a while. Unlike most of the Gold Bug-o-Sphere , this shop does not tout inflation as any reason whatsoever to own gold stocks. As the Continuum’s disinflationary trend (30yr yield chart above) allowed unfettered inflationary policy for decades, that inflation worked against gold stocks relative to gold. That is because the inflation mostly worked to cyclical ends.

Legions of gold bugs bitched about how gold stocks do not leverage the price of gold. Ah, wrong. They did what they are supposed to do. They leveraged gold’s standing in the macro, and with inflation pushing up prices of most items, including and especially the bubble in the stock market, gold mining was much more often than not an “also-ran” segment. So gold stocks leveraged gold, alright. In a negative way. Promotional interests do not want to tell you that (or they are clueless to it, too busy finding reasons to cheer lead).

However, as often noted, there was a glimmer back in 2001-2004 as the miners leveraged gold to the upside amid a deflating macro (green). If I am correct in assuming that today’s disinflationary whiff will become 2025’s deflation scare, gold – whether it rises, sits flat, or falls – will greatly outperform risk assets. In that case, you just watch well the miners’ fabled positive leverage returns.

One complication to the above is that the HGR (along with the Gold/Silver ratio) rose in 2001-2004 while the USD (shaded in the background) tanked off of its previous bull market. If the USD and GSR rise together in 2025, gold stocks would probably get hit hard. But if a deflationary macro (as indicated by a rising GSR) is met with a declining USD again (BRICS? Dedollarizers? At the ready?) gold stocks could tear ass and not come back any time soon.

During the 2001-2004 phase both gold and silver rose, although silver took a good long while to catch on. Silver only started to lift off after USD made its final top and only started to outperform gold in 2003 (to 2006), as the global inflation trades of the time – including China rising relative to the US – began.

Folks, please read the above as much (or as little, if you want to filter my noise) as you need to in order to let the information sink in and hopefully make some sense. That is what I am doing right now. I do find the China component quite interesting, especially since its recent performance seems to fly in the face of all that is Trump.

Jeez, these macro pictures can take you down some rabbit holes.

If the interim deflationary macro analysis is incorrect and whatever Trump, Musk & DOGE are doing under the hood of this jalopy proves inflationary, then the plan illustrated above will probably fail, at least at its core. There have been plenty of times that gold stocks rallied despite an inflationary backdrop. But those were not the long-term phases where we could really make a killing. They were trades.

Commodities

- CRB index has broken upward from a consolidation base and looks bullish. Fellow index GNX has not done so. DBC is an ETF and it is verging on a breakout. All in all, it’s down to the asset mixes of these items. The disparity is in commodity mix and weightings. Overall, the commodity complex continues to be poppers and droppers. No definitive and unified direction against an unfavorable macro backdrop, insofar as it is disinflationary. Certain commodities are subject to geopolitical and supply/demand and/or seasonal status.

- I unloaded remaining Energy positions simply to raise cash. XLE is still functional and it, XOP and several individual names are on watch. In this market, I have little bullish desperation. NatGas has popped with its seasonal (and a cold winter) within a very long-term sideways trend, and WTI oil is gently trending down.

- Copper is still biased bullish and if peace breaks out in Ukraine and rebuilding begins in war torn regions, you’d think that Doctor Copper and his industrial metal bros will play a role. It’s something to watch for. I have my eye on copper miners, but they are not bullish and the whole complex could be vulnerable to deflationary winds, if my macro view is correct.

- Uranium has gotten hammered, adjusting the previously stretched price of u3o8. The question was whether the sector could lead the U price back upward. Thus far, no. Uranium stocks are purely in correction now, diving to find a low. I keep NXE, UEC, UUUU, URNM and SRUUF on watch. But our view has been that u3o8 (blue line) may need to find a low per this chart’s support in the 58 to 50 area.

- REE producer MP Materials has been a standout among other outlier commodities and producers that have been up and down, mostly down. MP, as we’ve been noting for a few years now, is a strategic position and a Trump trade in an adversarial geopolitical world. It would be worth looking for similar traits in other stocks in Trump world.

- Lithium stocks are not doing well, but I am watching LAC (primarily), along with SLI and ALB for future reference.

- Palladium is bombed out and could be making a low. Platinum has been going sideways since 2016.

- Agricultural is a mixed bag of soybeans, sugar, corn, wheat, coffee, cows, hogs and other things humans ingest. I have proven not adept at trading here, and am leaving it alone. On balance the sector is trending up, with some bottom feeders – especially in the grains – bouncing.

USD & Gold/Silver Ratio (GSR)

The story is not yet told, in the short-term. That story will be told either by silver outperforming gold and USD declining…

…or by gold and silver [likely] under pressure but silver dropping relative to gold along with USD rising…

…or possibly even by the scenario noted in the Precious Metals segment, that would see gold outperform silver, USD decline and select markets (e.g. gold mining, China/Asia) continue to bull.

USD continues to hold breakout support and GSR continues to perch constructively. As long as this is the case, let’s keep in mind that our main theme for 2025 is a liquidity event and possible deflation scare before any major inflationary angst resurfaces.

If these two rise, especially rise impulsively, it’s everybody out of the pool because inflation is the last thing to be worrying about. If they fail together, Wayne and Garth have a message for you. As it stands now it’s still a standoff, but to my eye the 2 Horsemen still have the edge. But I will be open minded, either way.

Finally, the 2001-2004 option. The chart shows USD grappling for support while the GSR remains firm. If USD were to break down from its base breakout and GSR rises, the ’01-’04 blueprint comes to the fore.

Portfolio

Gold is long-term risk management & monetary value/stability in a balanced portfolio.

Taxable Account

In order of position size. Cash and short-term Treasury equivalents are the overwhelming holdings.

Trading Account

No positions.

Roth IRA (non-taxable, no contributions)

Again I’ll ask that you not take this chart too seriously. I have full control over it. I could go 100% cash/equiv. and see slight increases due to income. But it does give me some perspective on a weekly basis in a risky market.

What do I see here? Optimist Gary sees a bullish Ascending Triangle. Pessimist Gary sees a double top. Regular Gary is likely to react with more risk management (and possibly more shorting) if the Triangle breaks to the downside. Thus far, no break and February bond/cash income is on the way.

Cash and equivalents are 85%. My preferred method is to hedge gold stocks rather than sell core positions, sell broad stocks, with exceptions (e.g. MP) if needed before shorting, and hold a high percentage of cash/equiv. as usual in a high risk market.

I want to let the market come to me. I don’t want to go to the market, hat in hand hoping or wishing.

Cash & income-paying Equivalents are at levels that are right for me and my real-world situation. Your situation is different. Cash will be adjusted as needed.

Refer to the Trade Log under the NFTRH Premium menu at nftrh.com for trade info, if interested (not that you necessarily should be). Also, you can follow on X @NFTRHgt for notice of updates.

NFTRH is not to be distributed to third parties without prior written consent

Notes From the Rabbit Hole (NFTRH) is a weekly market report in which we provide analysis on financial markets. We make every effort to provide accurate and high quality content, but this analysis ultimately represents our opinions and these opinions are provided without warranty or guarantee of any kind. See full terms & conditions of service under the ‘About’ heading in the main menu.

you might want to add the XLV/SPX chart to your chart section……Dyrl

Good idea! I’ll require some tweaking of the HTML, which I’ll do after I get back up to speed. If it takes to long feel free to remind me.