As long-term yields rise in a reflated market (i.e. a market representing an economy that is gaining traction to a degree at least due to inflationary monetary/fiscal policy) the ‘reflation’ and ‘value’ stuff tends to be favored over the richly valued growth stuff. Today was a day for checking portfolios and balancing/rebalancing accordingly. I did that to a degree.

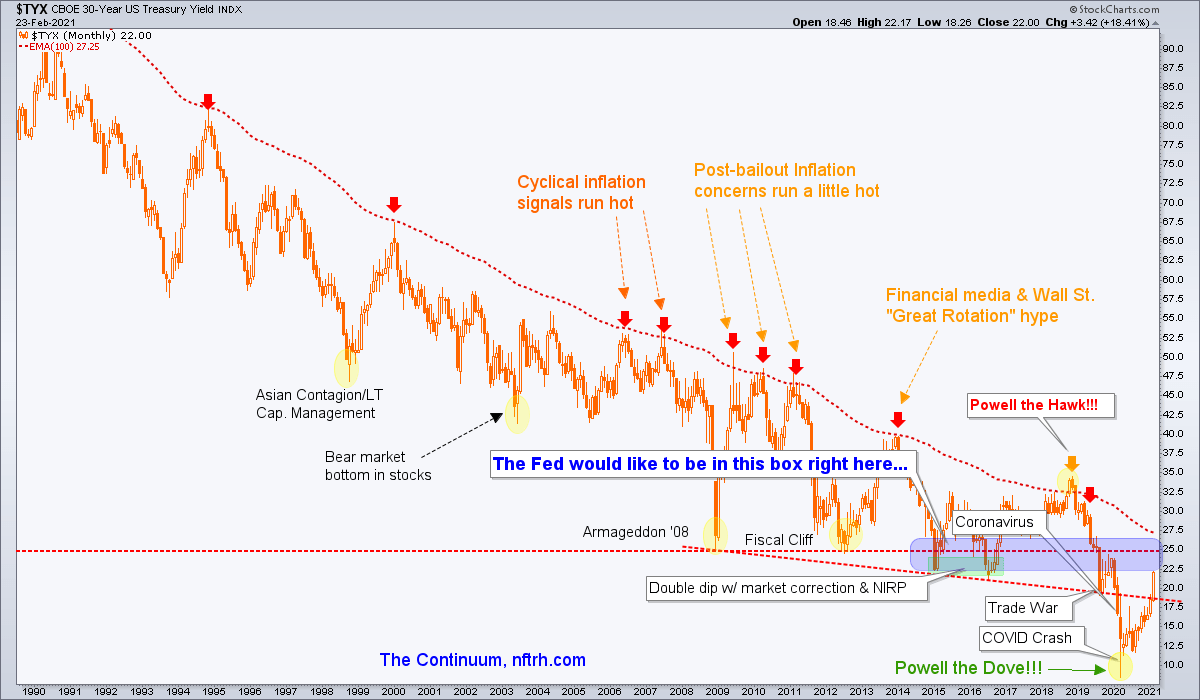

First, the Continuum once again because it wants to keep itself in front of our eyes consistently from here on. The 30yr yield is approaching the ‘Fed zone’ and the Fed Chief apparently did not even mention long-term interest rates in his prepared remarks this morning. That is not by accident. They did not want to freak out the markets and hence, they projected dovish.

But the macro decision point is yet to come with the Continuum’s EMA 100 limiter at 2.7% and oh so slowly (it’s a monthly chart after all) declining. We have been expecting volatility as the Continuum got into the 2% zone and while the reflation is still on and the asset bull is still on, it appears that volatility may be with us to a larger degree going forward.

It will be important to interpret the macro backdrop and apply that to asset allocations. Banks, Materials, Commodities and strategic economic resources (e.g. Lithium, REE, maybe even Uranium) are favored in an ongoing reflation that is boosting the economy. I’d add silver to a degree and gold because the moral hazard risks are increasing as the inflation becomes more intense.

This chart shows the Value/Growth ratio making a small move in a positive direction and the CRB index, which has been very strong yet not yet keeping pace with global stocks. I wonder if there could be some catch-up out ahead in both ‘value’ and commodities if the inflationary speculation keeps up. Anyway, it’s a clear picture about what the anti-USD reflation is doing to global stocks and commodities.