The anticipated cool-down in previously rising inflation signals is in full effect

Preamble

This is a post by human Gary, not market analysis provider Gary. It’s a free website with no ads, no nuthin’ that I ask of you. So you are free to either put up with this type of post once in a while or turn me off. Whatever works for you, really.

The post began as a simple look at the inflationary cool down that we began projecting months ago. But it veered off into some Op/Ed discussion. I don’t sling that mud to be a dick, but instead to try to keep things as real as possible for myself and anyone else who cares. I would not have made any light of this had the influencers in question not blocked me, thus cutting off my ability to share contrary opinions in venues under their control.

I am aware that posts like this lose me allies, contacts and even friends in a realm that my business can benefit by. But the truth is only that, the truth. It is not a commodity or a pitch. Plus, any excuse to present the estimable Larry Fine is more than welcome.

As economies reopen and the initial supply shocks of commodities and materials work through the system, well after the mainstream dinged its inflation-hype topping signal (hat tip to the always reliable Zero Hedge contrary indicator), an article that my Firefox browser and Pocket thought I might like to read popped up:

Seven Reasons to Be Extremely Optimistic About the Economy Right Now

The implication of this article is Goldilocks (not too hot, not too cold… but just right), a dreaded outcome if you’re a pom pom waving gold bug. There are debatable aspects of the article but there are also valid ones, if you care to read it.

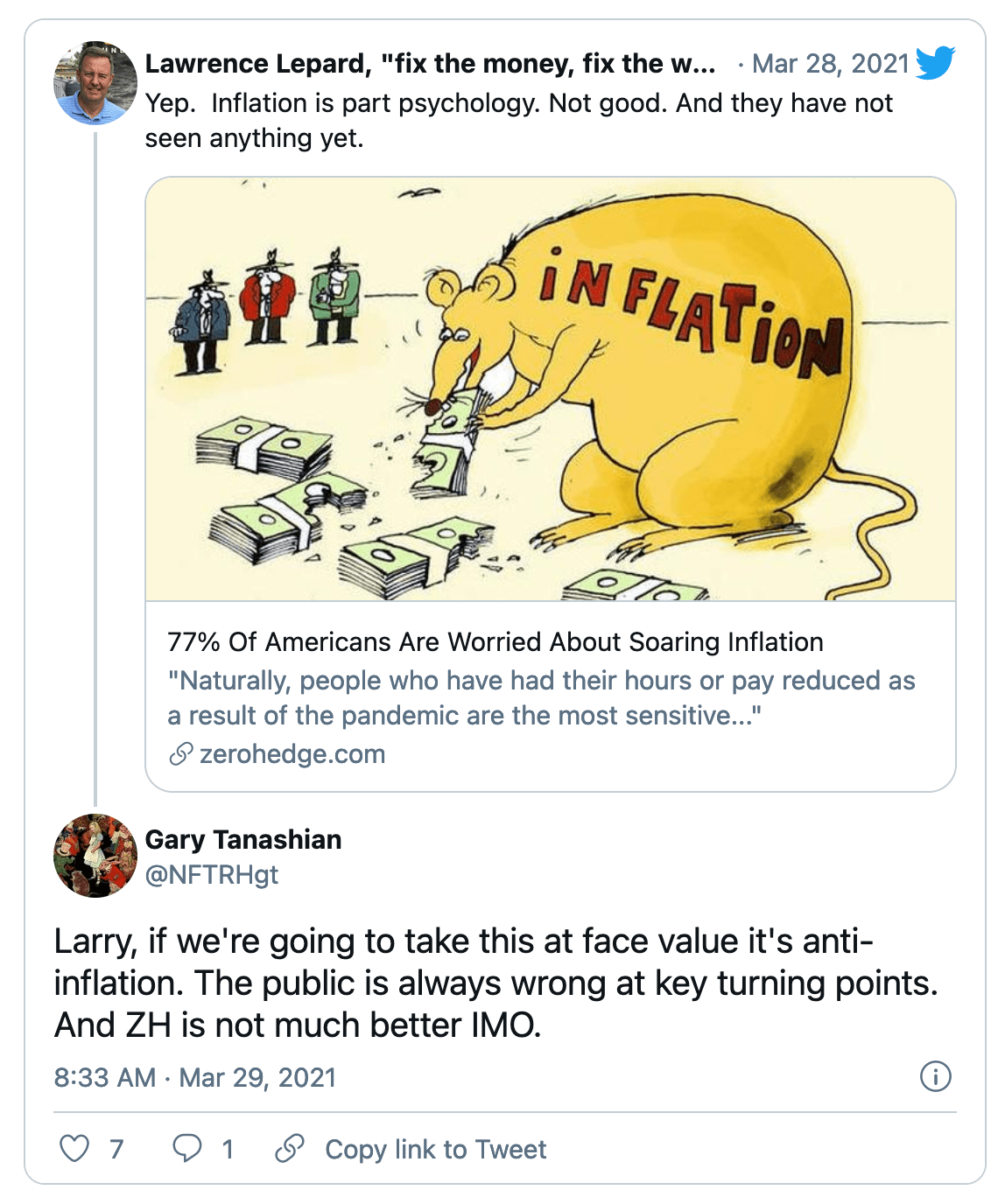

Speaking of pom poms and contrary indicators, in searching for some of my posts back when we were right-mindedly anticipating the inflation noise to hit a barrier, I found this NFTRH subscriber update (now public), and it featured good ole’ Larry, before he ultimately blocked me for tweeting the golden girls to his feed which, as taught in Twitter Influencer 101, must be sanitized of dissenting voices…

With pom poms waving. Larry, you…

…err, Twitter influencer; you called THE TOP in the 2021 inflation hysteria. You and your Ministry of Information, Zero Hedge.

Then rather curiously this commodity guru blocked me for, unlike the cheer leaders uploaded to Larry’s feed, a routine and courteous dissent, or what I actually meant as added color to the discussion about gold’s daily chart technical status.

Since I am blocked (I did not follow him by the way, he popped up in my stream because someone who follows me and/or I follow had interacted with him), a friend sent me a screenshot of this gentleman’s tweet backing off his previous constructive stance on gold of all the way back to 2 days previous. Guiding the herd ever so gently to brace for the worst. Did someone say contrary indicator?

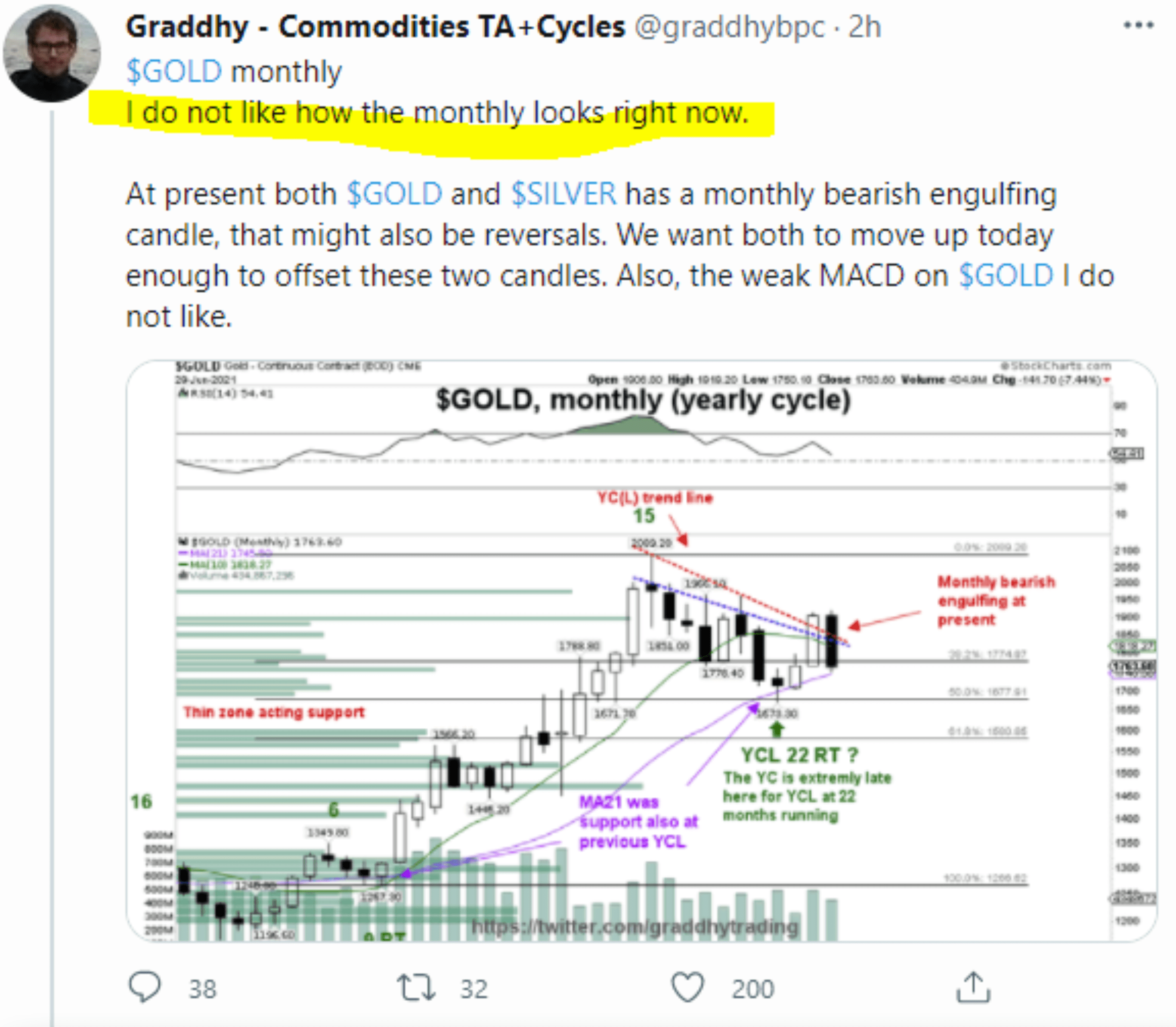

A bounce became more likely as gold got oversold to lateral support on daily charts and commodity/gold influencers tend their herds. As a side note, daily charts guide weekly charts and daily/weekly charts guide the lumbering monthly charts. So if projecting a bounce for example, the daily chart’s oversold status at support is potentially actionable, while the laggard monthly is not.

An oversold bounce is likely, but the monthly chart will not get fixed until well after the daily chart gets fixed, and it is far from that.

Anyway, after that detour through the world of gold, commodity and inflation influencing (AKA propaganda if not outright mind control for the more casual viewer) I want to get back on the track of this post’s original intent.

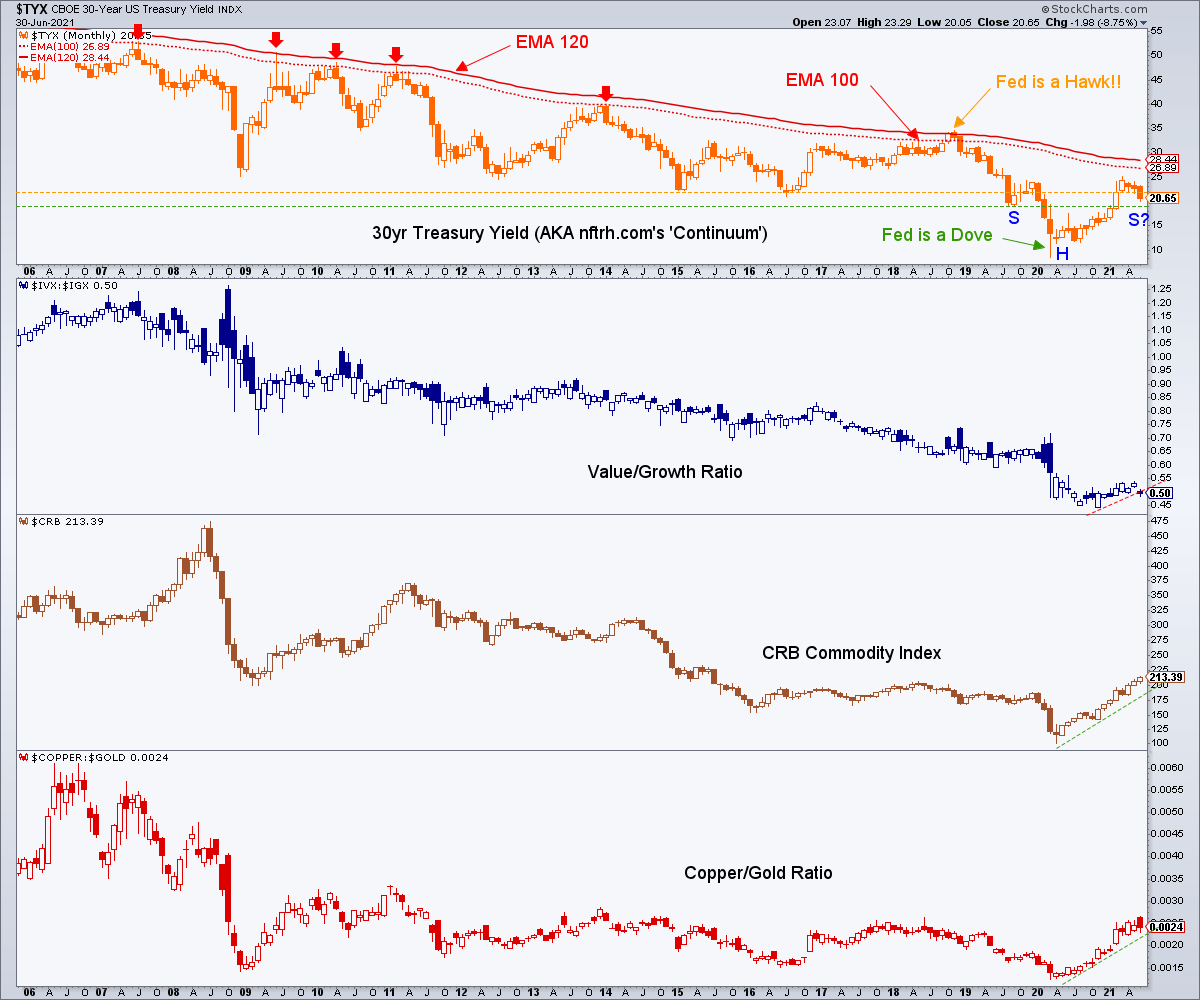

The inflation hysteria is cooling and per the linked article at top the mainstream is now getting that message. If I am right (and folks, unlike influencers I do not sanitize my Twitter feed or hide from my mistakes… wrong is something we all are sometimes and hiding from it only shows mental weakness) that the 30yr yield is making a right side shoulder to an inverted H&S, then Larry’s ‘ain’t seen nuthin’ yet’ sentiment will be proven out. But only after a good bout in the opposite direction.

As yet, of the lower panel amigos only the Value/Growth ratio appears in danger of breaking down.

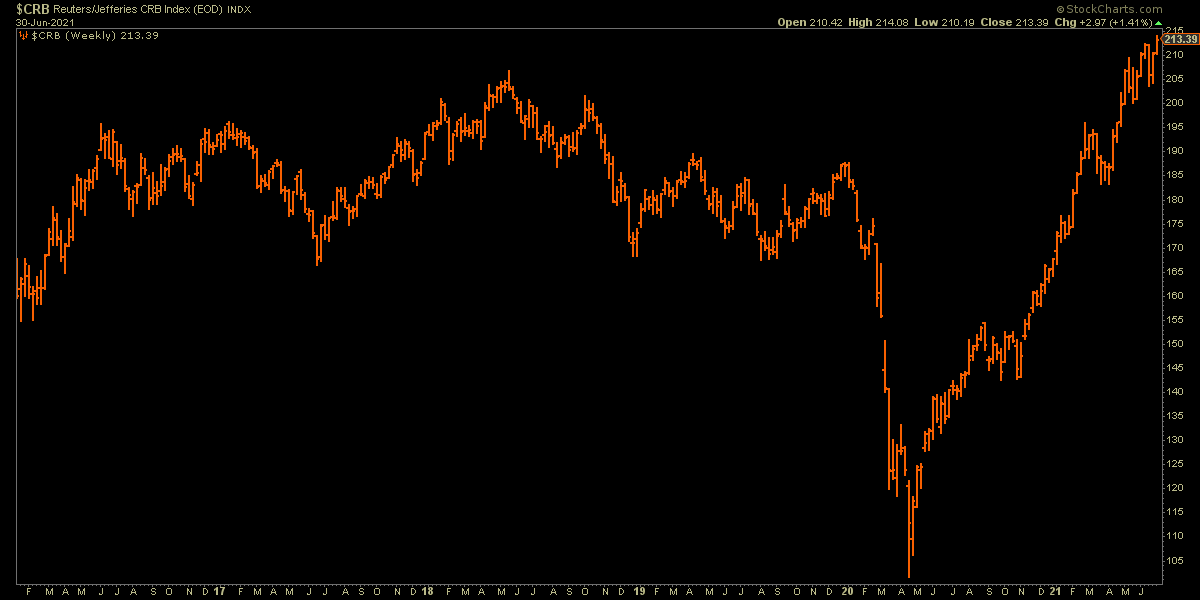

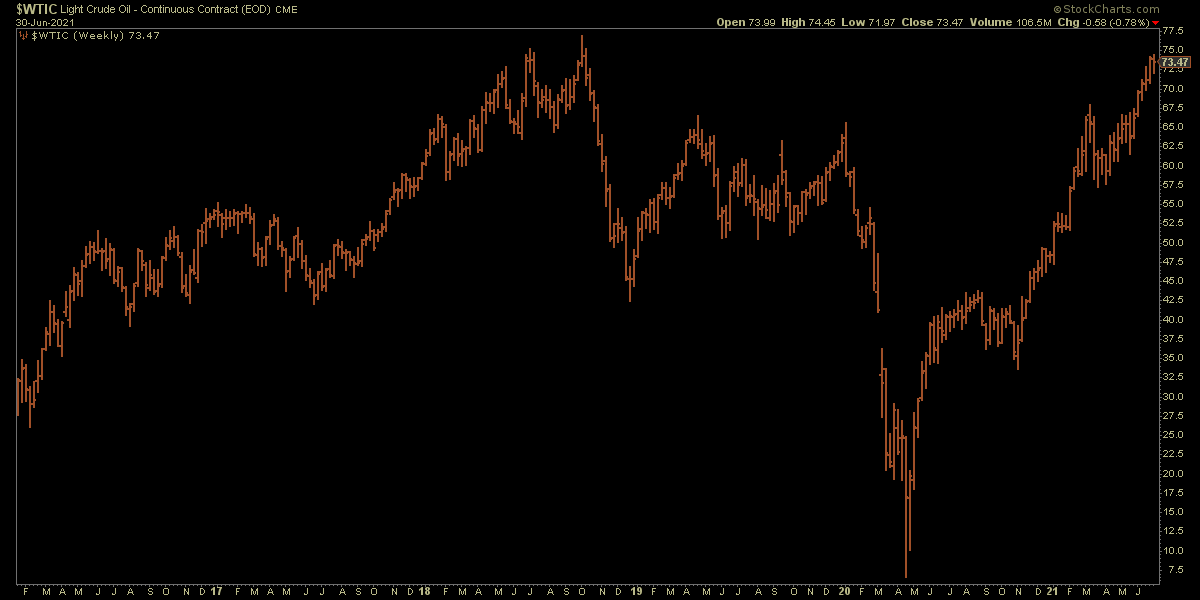

As for commodities, crude oil and its unique supply/demand fundamentals is what is flying the CRB index. Here, see CRB and see oil.

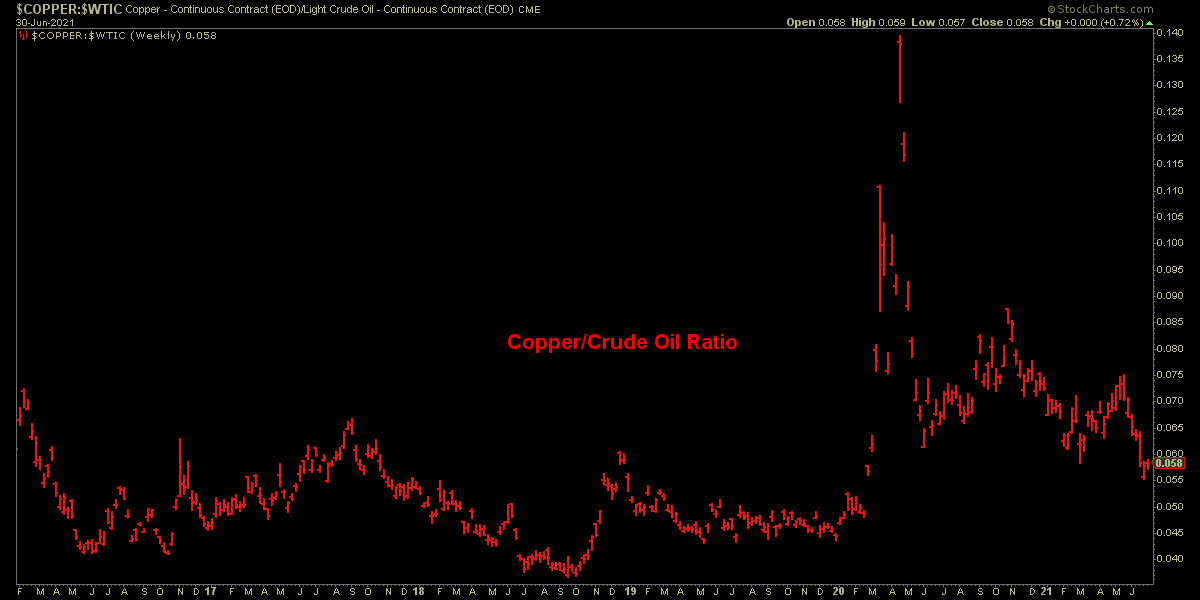

While copper, which led commodities out of the deflationary whirlpool of Q1 2020, has been losing relative strength as Goldilocks tries to assert herself. It’s not just Doctor Copper either. Materials, Financials and other reflation markets are doing the same.

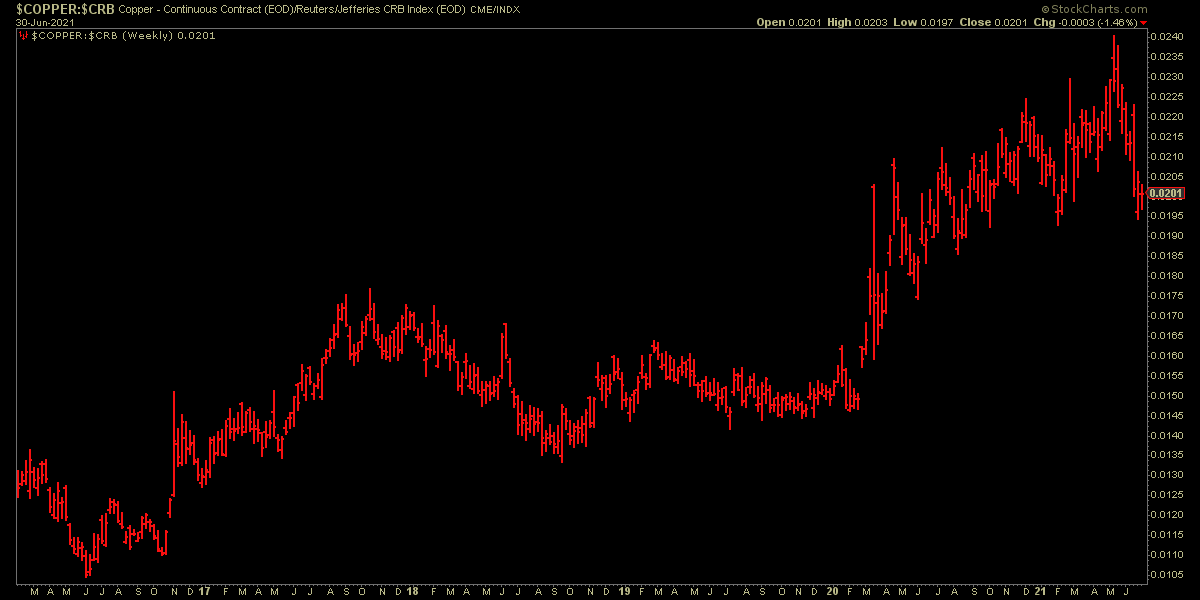

A final chart, the Copper/CRB ratio shows he who led the inflation trades upward has been dropping as would be expected during the inflationary cool down period this spring-summer.

What happens from here, I do not know. But neither do inflation touts, inflationist gold/silver bugs and others sanitizing their presentations for the herds.

You only need to look back to 2011 and Operation Twist, which killed the inflation tout but good by “sanitizing” (Bernanke’s own word) the inflationary macro back then. A more powerful entity than gold/commodity/inflation influencers was able to paint inflation out of the picture and Goldilocks into it (by using the simple mechanism of buying long-term bonds and selling short-term bonds, thereby kicking the yield curve into a years-long flattening trend).

As dastardly as I think Fed policy (esp. MMT TMM, total market manipulation) is, this is the only influencer I respect because their success or failure of agenda means only everything to how we need to manage markets.

For “best of breed” top down analysis of all major markets, subscribe to NFTRH Premium, which includes an in-depth weekly market report, detailed interim market updates and NFTRH+ dynamic updates and chart/trade setup ideas. You can also keep up to date with actionable public content at NFTRH.com by using the email form on the right sidebar. Follow via Twitter @NFTRHgt.